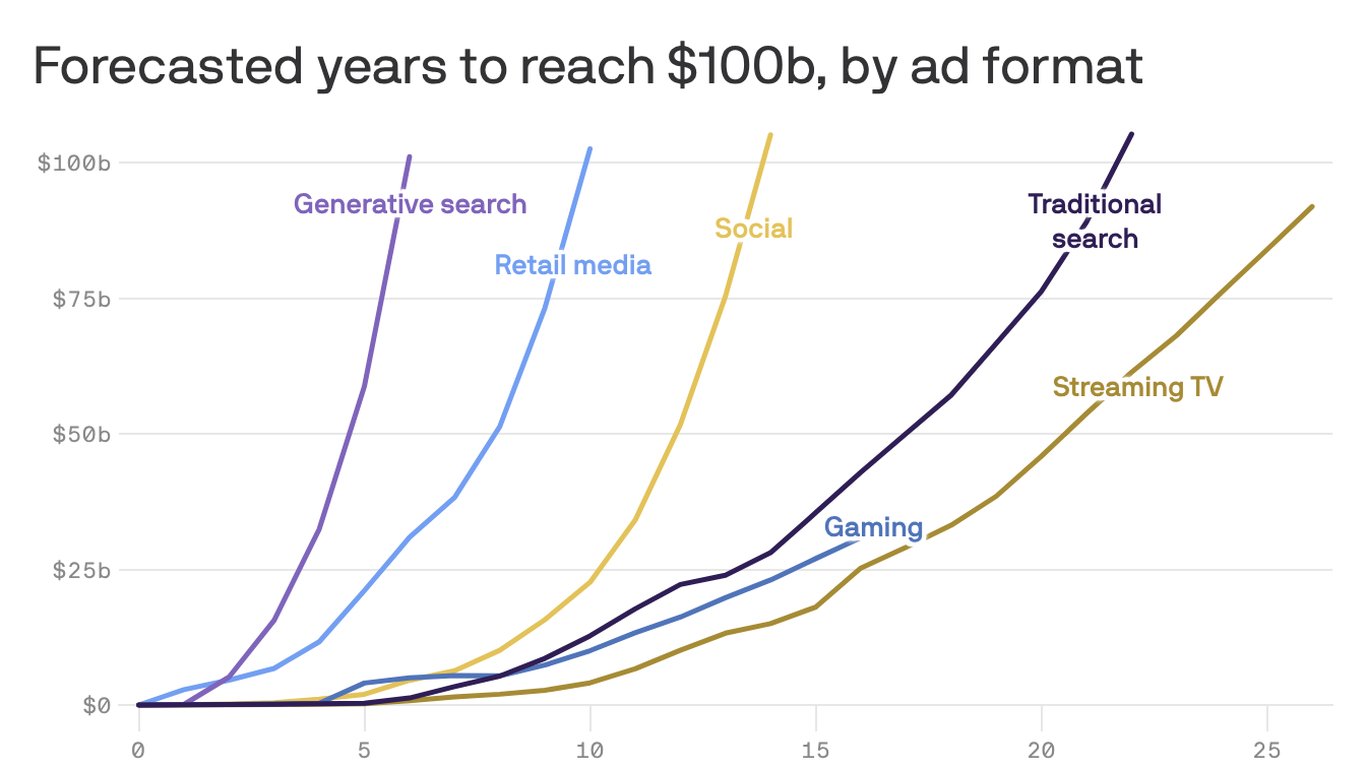

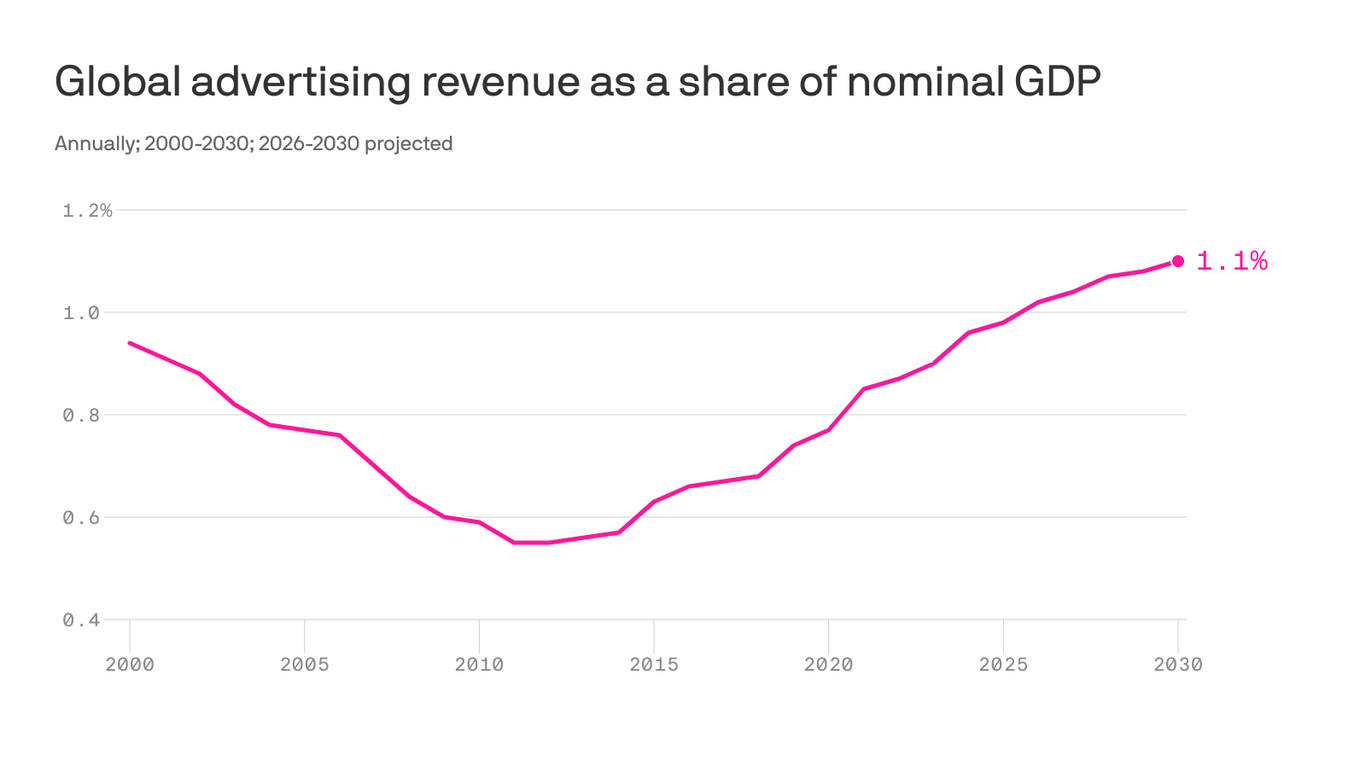

The global economy is navigating a highly complex dual reality: an energy and supply-chain shock operating side-by-side with a technology investment cycle of historic proportions. Yet, instead of triggering a market slowdown, the high-stakes race toward artificial general intelligence (AGI) has turned into an unprecedented economic engine.WPP Media’s This Year Next Year 2026 Global Midyear Forecast, authored by Kate Scott-Dawkins, global president of business intelligence, details how the ad industry is actively bankrolling the current AI transition. Highlighting upgrades to the U.S. forecast, the report reveals exactly where the dollars are moving as tech stacks and consumer behaviors shift.Here are the can’t-miss takeaways from this year’s midyear report.1. The AI ‘gold rush’ and explosive rise of generative searchThe defining narrative of the 2026 forecast is the concentrated AI investment boom. The U.S. remains the undisputed center of this surge and the primary engine of global advertising growth, with total ad revenue now projected to reach $483.4 billion. This reflects an 11.9% growth rate (excluding political spend) — a massive upward revision driven by the concentrated surge of AI platform investments.(Photo credit: WPP Media, used with permission)To explain this market behavior, the report draws a direct historical parallel to the 19th-century American West: “AI investment — and the advertising it generates, both from AI-native companies and from traditional advertisers deploying AI to improve efficiency across their businesses — is providing a powerful countervailing force, much as the Gold Rush did nearly two centuries ago.”During a recent press briefing, Scott-Dawkins explained, “The best [analogy] that I could come up with as I was starting to write the report this year was the Gold Rush and the concept of manifest destiny. If you listen to a lot of the rhetoric from AI labs and people in tech, there is an inevitability about artificial general intelligence that is creating this rush — this ‘succeed at all costs’ before the other person, company or market — and that has driven a ton of investment that would seem to defy logic in terms of the pace of growth.”This aggressive spending has physically spilled out onto the streets of the tech boom’s epicenter, completely saturating the local landscape: “When you live in San Francisco, you can really feel the locus of that. Every bus stop, every billboard, every out-of-home contains the word AI in it,” Scott-Dawkins said. “It is really astounding.”The record-breaking pace of generative searchReflecting the rise of paid advertising in AI environments, the midyear report officially introduces generative search as a standalone forecasting category for the first time. The new sub-channel isolates paid placements and ad impressions served within environments including Google’s AI Overviews and AI Mode or standalone conversational AI products such as OpenAI’s ChatGPT.Globally, generative search is forecast to bring in $5.1 billion in 2026, with the U.S. dominating the market by capturing roughly 60% of total revenue at $3 billion. WPP’s baseline model suggests that if current momentum holds, generative search could cross the $100 billion threshold within six years, making it the fastest media channel in history to do so.“Generative search is a very difficult thing to forecast with zero historical data,” Scott-Dawkins said. “Traditional search was there in [22 years], social in about 14, retail media cut that down to about 10. It feels somewhat reasonable that we would get there in six with generative search, especially as Google, the incumbent, is going to be able to make that transition within its own walls quite efficiently. And then you have the added element of companies like OpenAI adding to that, as well.”2. Television’s tipping point: Streaming surpasses linearIn a monumental structural shift for home entertainment, 2026 marks the official tipping point where streaming ad revenue surpasses linear ad revenue in national, non-local U.S. television.While total U.S. TV ad revenue is forecast at $68.5 billion — holding nearly flat at 1.5% growth but insulated by premium live sports such as the NFL, NBA and the FIFA World Cup — the internal mechanics have permanently fragmented. Linear TV is poised to slide down 8.6% to $41 billion, while streaming TV ad revenue will expand by 21.5% to reach $27.6 billion.“In the U.S., streaming ad revenue will surpass linear in national (non-local) TV in 2026 — a milestone Disney foreshadowed in its fiscal Q2 earnings, where the company reported it now generates more entertainment subscription, affiliate and advertising revenue from [subscription video on demand] than linear,” the report notes.3. Global power shift: Legacy media erased from the top 10From a macro perspective, the report highlights a staggering re-rating of who controls global advertising inventory. For the first time in history, traditional media owners have been completely pushed out of the world’s top 10 largest advertising sellers. Walled gardens, data scale and AI optimization have allowed digital-native or digital-dominant tech and commerce giants to absorb the vast majority of international ad spend.Furthermore, the global ranking reveals a widening geographical tech divide. Chinese digital platforms have scaled aggressively to offset soft domestic consumer demand, and they now officially outnumber U.S.-based platforms in the global top 10 by a ratio of six to four. U.S.-based legacy media and entertainment companies that used to occupy the leaderboard 10 years ago, such as Paramount, Disney and Comcast, have been replaced by platforms including Kuaishou and JD.com, China’s largest retailer. “It’s interesting how the composition now includes a lot of commerce players,” Scott-Dawkins said during the press briefing. “The ability to tie media to purchase has become very, very important in this world.”4. The $12.4 billion midterm political tsunamiCompounding the U.S. market’s explosive growth is the predictable, yet unprecedentedly massive influx of political advertising cash.In this midterm election year, U.S. political ad revenue is forecast to reach $12.4 billion. This represents a 7.6% increase over the previous midterm cycle. When this political windfall is added back into the broader equation, the total U.S. advertising market growth rate rises from 11.9% to 13.9%.This wave of political cash often crowds out non-political local TV ad spend, creating localized pricing pressures across broadcast and digital channels alike.5. The shifting legal battlefield: Product liability over contentAs tech platforms have grown to operate similarly to municipal “semi-governments” — a parallel Scott-Dawkins draws to Neal Stephenson’s 1992 dystopian novel Snow Crash, where civic services are supplanted by corporate franchises — they are facing a wave of landmark legal and regulatory scrutiny centered squarely in the U.S.Crucially, the legal strategy behind these new cases has shifted in a way that directly impacts digital media monetization. Rather than suing platforms over the specific third-party content they host — which has historically been protected by the broad legal shield of Section 230 of the Communications Decency Act — plaintiffs are now successfully targeting the underlying platform architecture.Recent, high-profile verdicts in New Mexico and California have found platforms such as Meta and Google liable for harms to minors based on their reward-reinforcing, engagement-maximizing product design features. As the report authors note, this development strikes directly at the core mechanism used to drive user attention and digital ad consumption.“By arguing that algorithmic recommendation, infinite scroll, variable-ratio reinforcement (the same unpredictable reward mechanism behind slot machines — you scroll, sometimes you find something compelling, sometimes you don’t, and the uncertainty is precisely what keeps you scrolling) and other engagement-maximizing design features constitute a product rather than an editorial function, plaintiffs are routing around the immunity that has defined the economics of the internet for three decades,” the report notes.6. Looking forward: The ‘agentic’ future of advertisingWPP points out that looking beyond immediate regulatory or platform shifts, the long-term evolution of the industry involves navigating a world where advertising bypasses humans altogether. As consumers look for a “personal defender” to filter through an increasingly adversarial web filled with AI-generated spam and sophisticated deepfakes, they will delegate everyday commercial decisions to personal AI agents.When software automates these daily choices, traditional ads designed to catch a person’s attention are no longer enough on their own, the report says. Marketers will have to adapt by figuring out how to make their brands appeal directly to algorithms and AI assistants rather than human shoppers.“The historical definition of advertising — messages directed at humans to influence human behavior — may not be sufficient for an era in which a meaningful share of commercially relevant decisions are made by non-human systems. Whether those systems are participants in the brand-consumer relationship, silent facilitators or something else entirely is a question the industry will need to resolve — likely sooner than it expects.”

WPP Media: AI search ad revenue set to hit $100B at record speed

From the AI gold rush to streaming’s takeover of linear TV, the forecast reveals the forces driving advertising’s next era.

1,413 words~6 min read