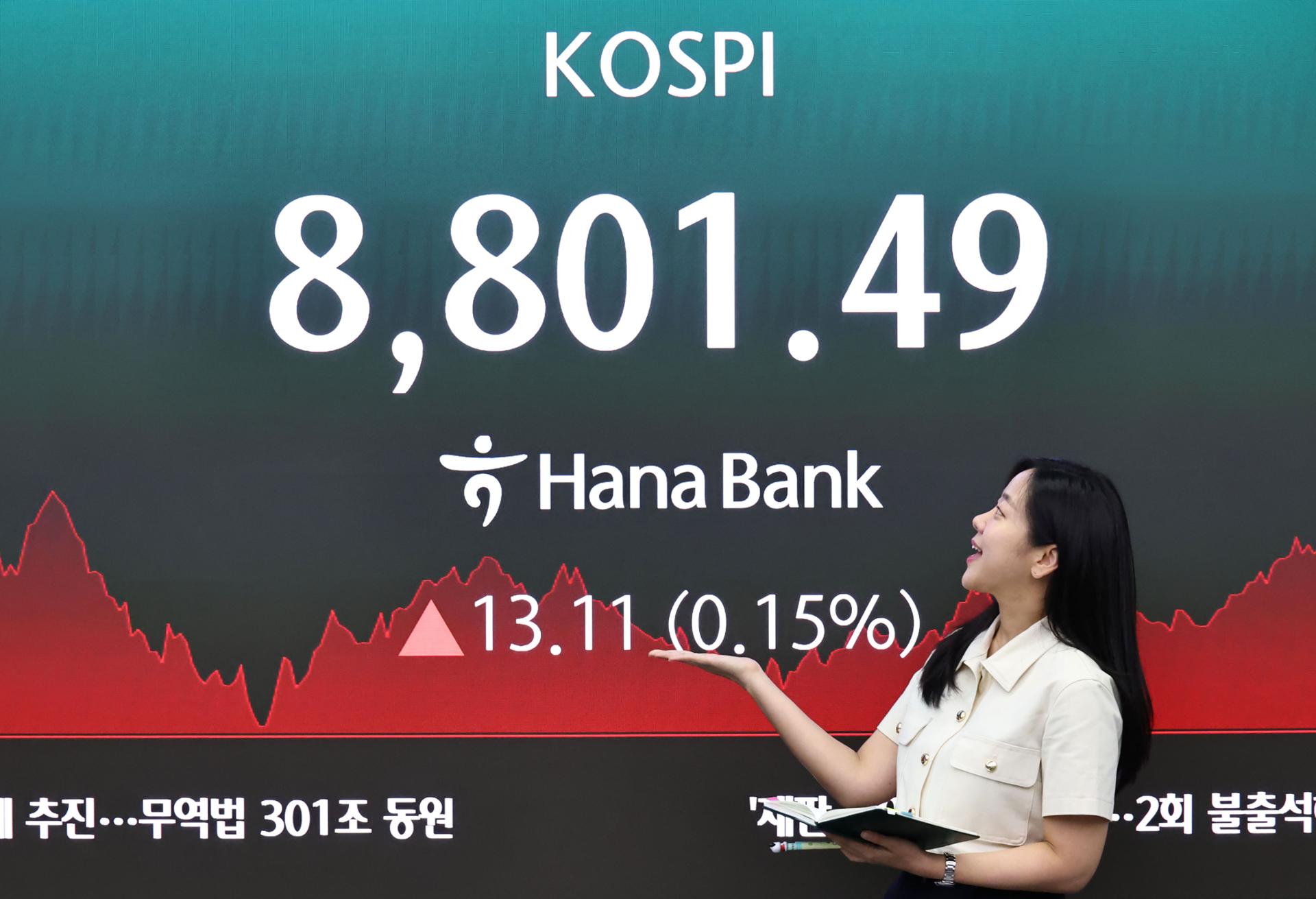

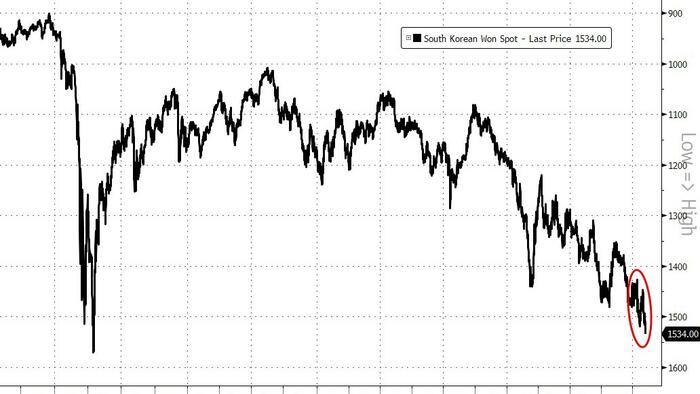

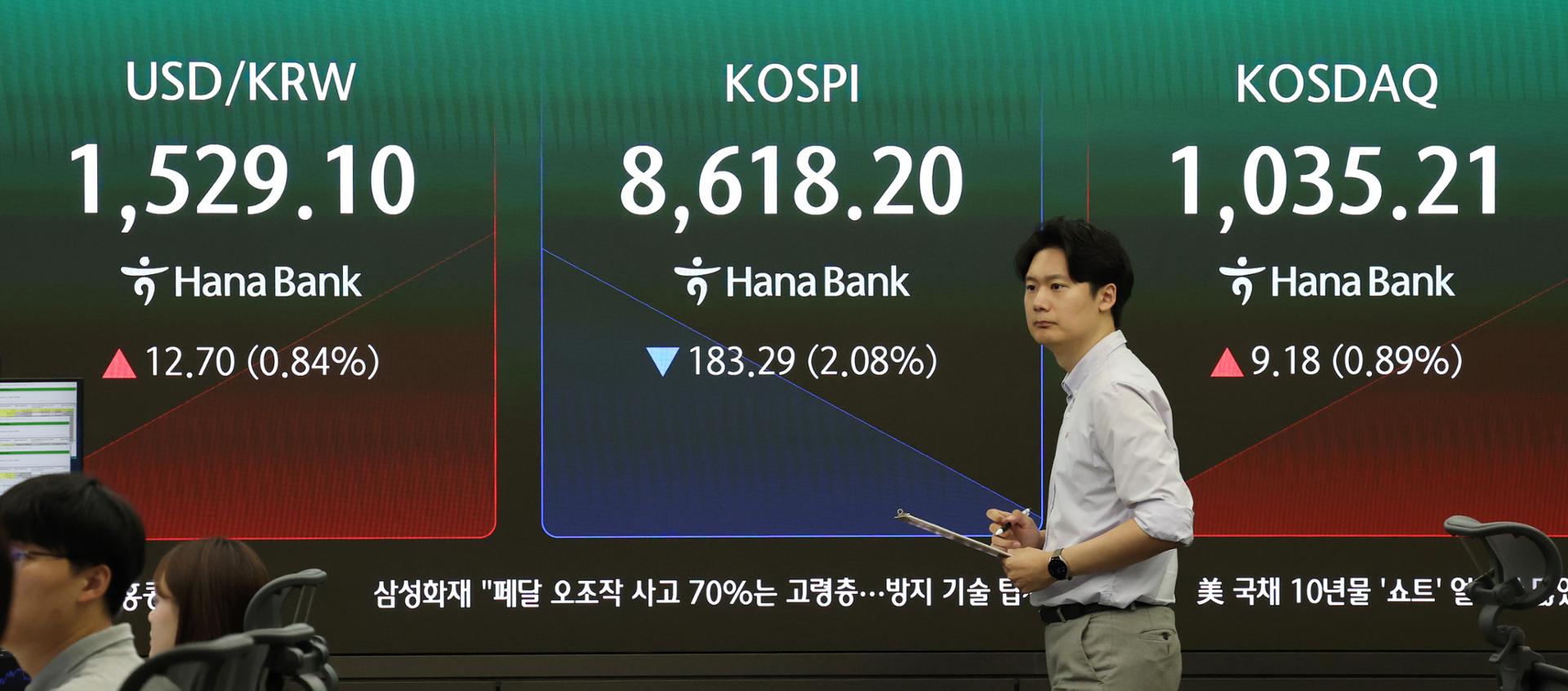

Foreign investors remain net sellers, but domestic liquidity is increasingly driving Korea's market higher, veteran analyst says Kim Hak-kyun, head of research at Shinyoung Securities, poses for photos during an interview with The Korea Herald at the firm's headquarters in Yeouido, Seoul, on Monday. (Im Se-jun/ The Korea Herald) The Kospi's historic rally may have changed the way investors talk about the Korea Discount, but it has not erased the deeper valuation gap that still weighs on Korean equities, according to Kim Hak-kyun, head of research at Shinyoung Securities."(The) Korea Discount has been fully resolved if you are talking about whether stock prices failed to rise," Kim said in an interview with The Korea Herald in Yeouido, Seoul, on Monday."But if the term refers more precisely to how undervalued Korean companies are relative to their assets and earnings, Korea is still discounted."Kim, a market strategist with nearly three decades of experience, has led the research center of Shinyoung Securities, a Korean brokerage best known for its long-term, value-oriented investment approach, since 2018.His argument draws a line between a price rally and a structural rerating. The Kospi has more than doubled from around 2,290 in April last year to above 8,500, powered largely by Samsung Electronics and SK hynix as the AI memory-chip cycle amplified a broader global equity boom and turned Korea into one of the world's best-performing major markets.That makes the rally both real and incomplete. Korean stocks have risen enough to challenge the view that the market has simply lagged global peers, but Korea remains among the world's cheapest markets on earnings and only slightly above China on price-to-book terms, he said.The rally's narrowness is the clearest reason. Excluding Samsung Electronics and SK hynix, the Kospi would be closer to 5,200, Kim said, meaning the two chip giants have accounted for a large share of the index's rise."When Samsung Electronics rises, it tends to absorb liquidity like a black hole because it has been Korea's dominant stock since after the Asian financial crisis," he said.But Kim said that narrowness should not be read only as a weakness. Even without the two chipmakers, the index has roughly doubled from last year's level, and many companies outside the AI trade now look inexpensive relative to their fundamentals."There are many companies still trading below book value while generating returns on equity of more than 10 percent and dividend yields above 3 percent," Kim said. "For investors who can wait, I think this rally may offer opportunities in stocks across industries that have been left behind by the semiconductor rally."That potential rerating is tied to governance reform as much as valuation. The government has pushed Commercial Act revisions aimed at strengthening shareholder rights, while regulators are expected to keep pressure on companies trading far below book value.Kim said many undervalued companies are cheap for a reason, often because their assets have not been used in ways that benefit shareholders. That is why governance reform, rather than price support alone, matters for any lasting rerating."The revision of the Commercial Act is a change in Korea's capital market culture," Kim said. "Governance will not improve in a single day just because the law has changed. What matters now is that the spirit of the law takes root in reality."The rally has also been powered by domestic liquidity strong enough to offset foreign selling. Foreign investors have sold more than 100 trillion won ($66 billion) in Korean shares since November, including 44 trillion won in May, according to Korea Exchange data. Kim Hak-kyun, head of research at Shinyoung Securities, speaks during an interview with The Korea Herald at the firm's headquarters in Yeouido, Seoul, on Monday. (Im Se-jun/ The Korea Herald) Local money has absorbed much of that pressure, with about 110 trillion won flowing into the market this year through late May and investor deposits at brokerages hitting a record 137 trillion won in mid-May. Kim called the pace "almost unprecedented," already surpassing the 75 trillion won that flowed in during the full year of 2021, the market's previous historic rally.That has changed the meaning of foreign selling. Before the pandemic, the Kospi typically rose when foreigners bought and weakened when they sold. But during the COVID-19-era rally, foreigners sold from the bottom while domestic investors drove the index from around 1,400 to 3,300. A similar structure is visible now, Kim said."Foreign investors' moves still need to be watched, but it no longer seems to be the case that the market falls simply because foreigners are selling," Kim said. "What matters more now is the speed and strength of Korean investors' money moving into the stock market."For now, Kim said domestic money could continue to support the market into early next year, especially as Korean equities have outperformed US stocks over the past year. But the more durable test is whether the rally can turn equities into a long-term asset for Korean households, giving shareholders reasons to stay even after the cycle turns."Stocks cannot keep rising forever because markets move in cycles, and bear markets will come," Kim said."That is when governance matters. I hope companies can give shareholders dividends and other reasons to stay invested."

Kospi rally is real, but Korea's rerating has only begun: Shinyoung strategist

The Kospi's historic rally may have changed the way investors talk about the Korea Discount, but it has not erased the deeper valuation gap that still weighs on

863 words~4 min read