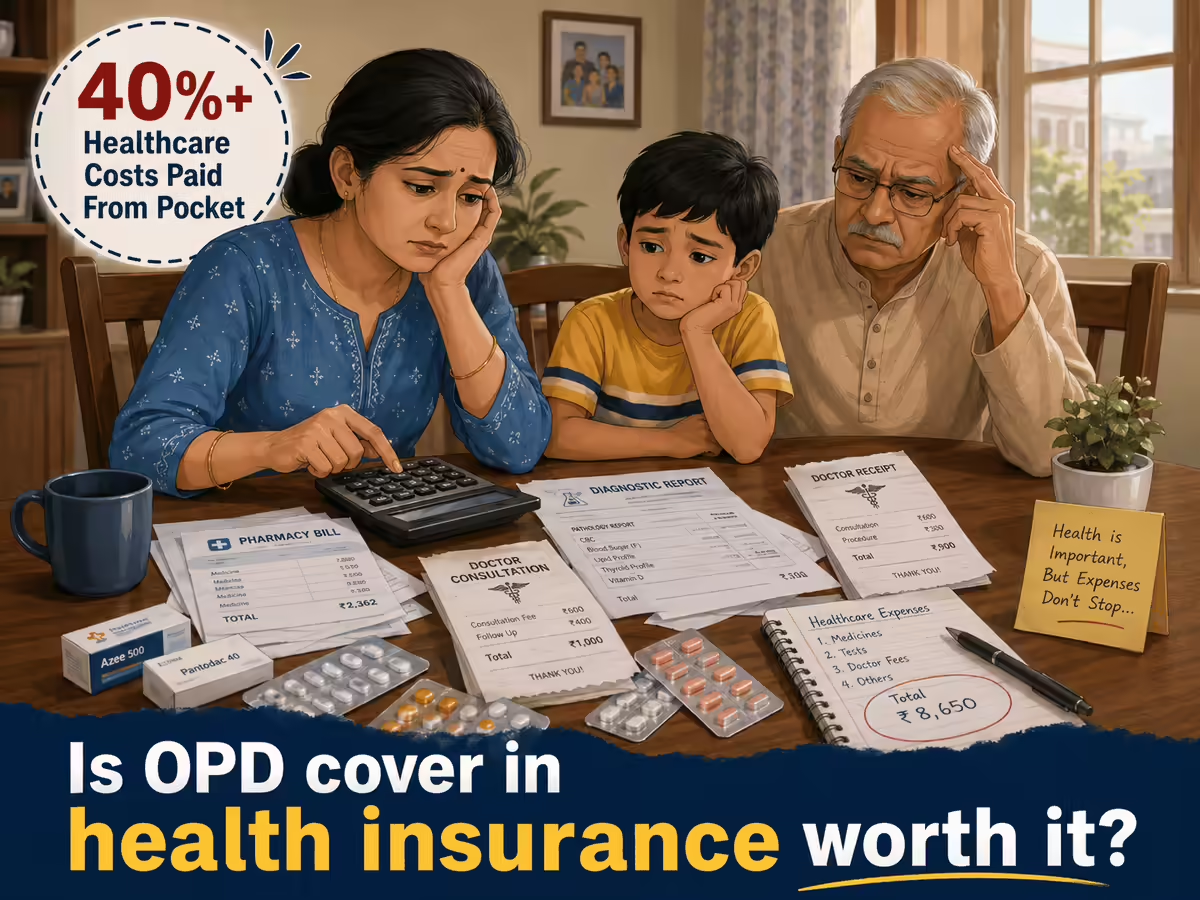

Do you often find yourself spending on doctor visits, medications, or diagnostic tests? If yes, OPD (Outpatient Department) cover could help reduce these out-of-pocket expenses.While regular health insurance mainly takes care of hospitalisation costs, OPD cover offers benefits for certain medical expenses that don’t require you to be admitted to hospital. But since it comes at an additional cost, is it actually worth paying for?Keep reading to discover what OPD coverage includes, how it differs from day care treatment, and when it may or may not make financial sense.What is OPD coverage in health insurance?OPD coverage generally includes medical expenses incurred without any hospital admission. These expenses may include doctor consultations, diagnostic tests, prescribed medicines, physiotherapy sessions and other routine treatments.Also read: Insurer denies Rs 20 lakh life insurance claim over diabetes non-disclosure; woman fights back and wins; here’s whyIt can be particularly useful for individuals who need regular consultations, monitoring, or ongoing treatment.“OPD is what happens when you just walk into a clinic with a bad fever, see a physician, get a prescription, and head straight home. It simply covers your routine out-of-hospital expenses like consultations, lab reports, and pharmacy bills,” says Sarita Joshi, Head of Health and Life Insurance, Probus. What is the difference between OPD and day care treatments?Many policyholders confuse OPD coverage with day care treatment, but the two serve very different purposes. Here is the difference between the OPD and day care treatments:AspectOPDDay CareHospitalizationNo hospitalization requiredRequires hospitalization for less than 24 hoursNature of treatmentConsultations, diagnostics, pharmacy, routine check-ups, minor proceduresProcedures such as cataract surgery, dialysis, chemotherapy, tonsillectomy, etc.CoverageOPD is usually not covered in standard policies unless specifically includedMost health insurance policies cover day care treatments (subject to policy terms and listed procedures)Sum InsuredOPD treatment may have sub-limits depending on the policyGenerally covered up to the sum insured limitIn a country where more than 40% of the healthcare costs are treated as out-of-pocket expenses and hence not covered under health insurance, day care treatments are usually covered under the standard hospitalisation benefit, whereas OPD needs to be opted for by paying an additional premium, says Milind Tayde, Head - Employee Benefits, Anand Rathi Insurance Brokers.Who should buy OPD cover in health insurance?The usefulness of OPD cover largely depends on an individual's healthcare needs and expected usage. OPD cover can be particularly beneficial for families with predictable and recurring medical expenses.Also read: Less than 24 hours in Hospital? Know about health insurance coverage for day care treatments, surgeries, and emergency procedures“Take a household where senior parents need regular endocrinologist visits and constant chronic care management for diabetes. Those Rs 2,000 pharmacy bills and regular lab tests add up fast over twelve months. For these families, an OPD feature is highly practical because it turns a stream of certain out-of-pocket clinic expenses into a structured, predictable annual insurance budget,” says Joshi.Similarly, OPD coverage can be beneficial for individuals suffering from chronic illnesses such as diabetes, hypertension, etc., which require regular doctor consultations and follow-ups. It may also be useful for certain dental treatments that are generally not covered under standard health insurance policies, explains Sandeep Aggarwal (EVP & Head-Corporate Health Claims), IFFCO TOKIO General Insurance Company Limited.OPD cover exclusions and hidden conditions you should check before buyingLike most insurance products, OPD cover comes with conditions, limits and exclusions that should be thoroughly checked before buying.“The main thing to watch is how the benefit is structured. A plan might give you a ₹10,000 total OPD limit, but cap individual doctor consultations at ₹500 per visit. If your trusted specialist charges ₹1,200, you pay the balance,” says Joshi.Buyers should also verify the utilization rules, such as whether the plan covers teleconsultations or requires you to purchase medicines exclusively through their digital partner networks, she adds.Policyholders should carefully review the fine print. According to Narendra Bharindwal, President, Insurance Brokers Association of India (IBAI), common restrictions include :Annual reimbursement capsLimits on consultation feesRestrictions on pharmacy expensesNetwork hospital or clinic requirementsCo-payment clausesWaiting periods for certain treatmentsSome plans also require digital consultations through designated platforms or prior authorization for certain benefits. Overall, OPD coverage should be viewed as a lifestyle and healthcare convenience benefit rather than a substitute for core hospitalization coverage. The decision to opt for it should be driven by individual healthcare needs, expected utilization, and a careful assessment of the benefit-to-premium ratio, he adds.When OPD cover may not be worth the additional health insurance premiumWhile OPD coverage can be valuable for some policyholders, it may not offer good value for everyone, as the value of OPD coverage depends largely on utilization.Also read: Latest claim settlement ratio of health and general insurers released by IRDAI in 2026: Niva, Acko, Aditya Birla, Galaxy lead; Shriram, IFFCO Tokio fall below 90%“If you are a healthy 28-year-old whose only medical event is an occasional seasonal flu, a heavy OPD premium doesn't add much value. Insurance math is straightforward here: because OPD claims are a near certainty, the premium is often closely pegged to the actual wallet balance provided. If a feature adds ₹6,000 to your premium just to give you a ₹6,000 consultation limit, it's often more practical to simply self-fund those rare clinic visits,” says Joshi.“For healthy individuals who rarely visit doctors or undergo diagnostic tests, the additional premium may exceed the actual OPD benefits availed during the policy period,” says Bharindwal.Should you buy OPD cover in health insurance?Experts suggest that OPD cover should be viewed as a convenience and healthcare budgeting tool rather than a replacement for core medical treatment.For families with recurring medical expenses, chronic illnesses or frequent consultations, the additional premium may be justified. However, for healthy individuals with limited healthcare needs, self-funding routine medical expenses may prove more economical.

Should you buy OPD cover in health insurance? Over 40% of healthcare costs are paid out-of-pocket in India - The Economic Times

OPD cover in health insurance addresses out-of-pocket expenses for doctor visits, diagnostics, and medicines without hospitalization. While beneficial for those with chronic conditions or frequent consultations, it may not be cost-effective for healthy individuals. Carefully review sub-limits and exclusions before purchasing.

949 words~4 min read