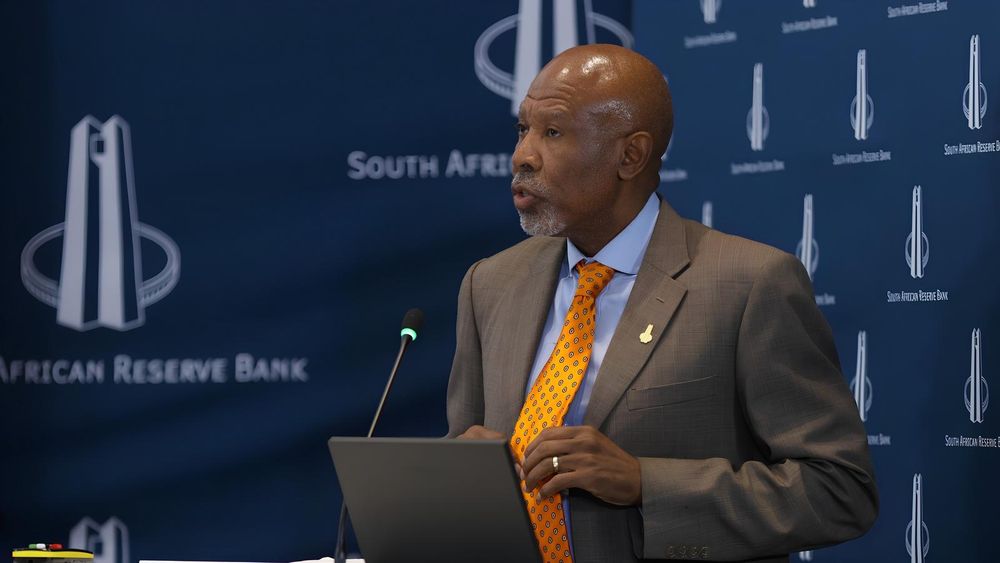

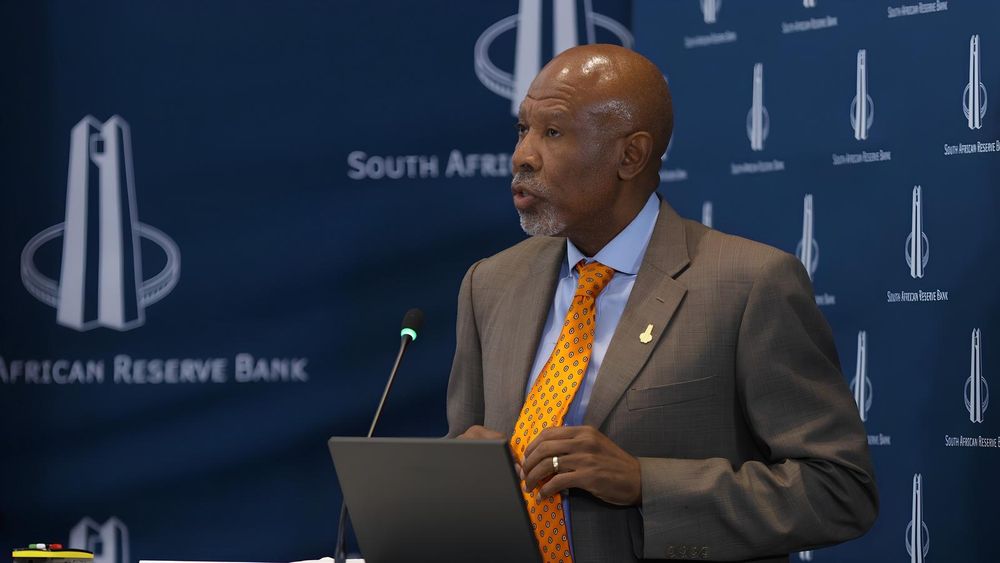

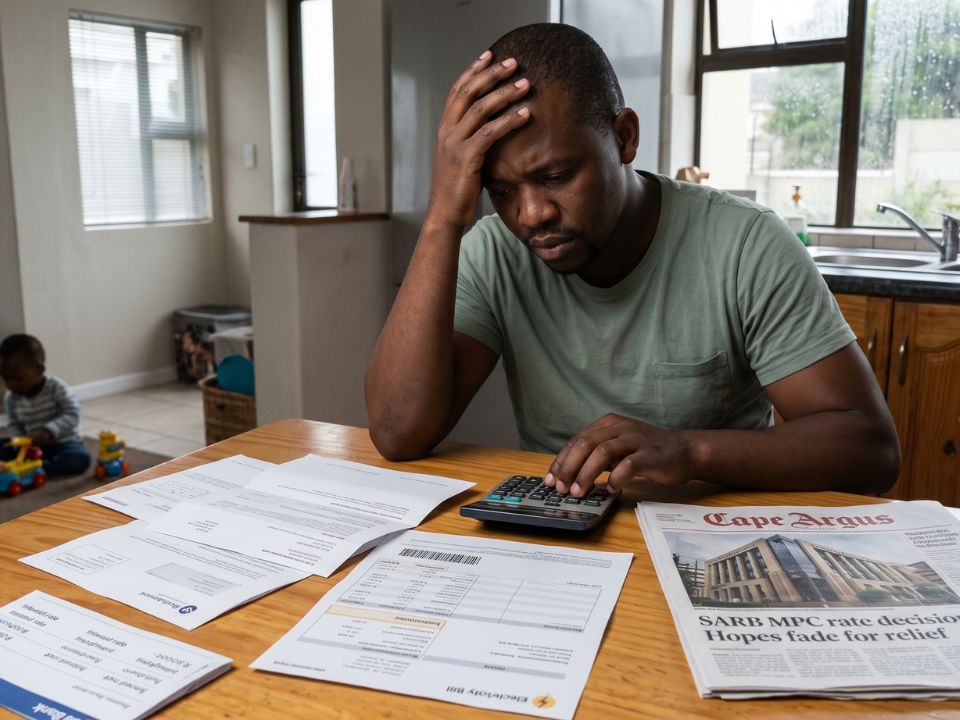

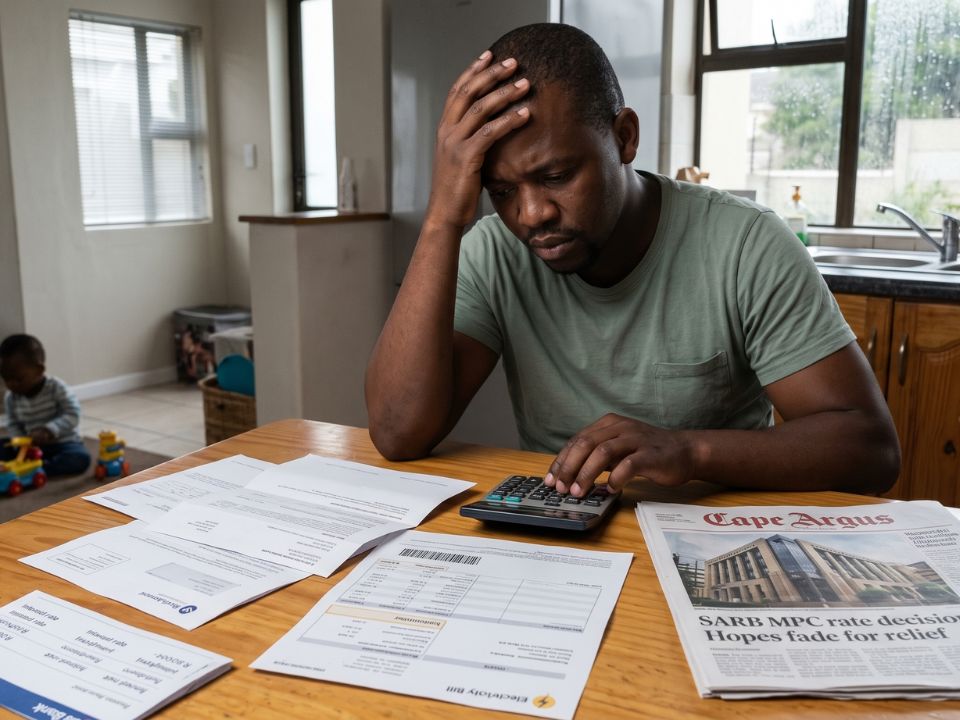

We could debate until the cows come home whether the Reserve Bank’s decision last week to raise interest rates when economic growth is so feeble was the correct call or the right timing.What is not debatable is that the outcry that the 25 basis point hike will stifle household spending and undermine GDP expansion drives home the warning made by numerous economists and policymakers over the years that relying so heavily on consumption to drive the economy is unsustainable.Bank governor Lesetja Kganyago made it clear that though the Bank lacks the tools to prevent the initial effects of supply shocks linked to the Middle East conflict, monetary policy is also responsible for longer-run inflation.“We take this duty seriously and reiterate our commitment to bringing inflation back to 3% over time,” he said. And that is the point that is often overlooked in the often emotive debate over taming inflation versus growing the economy.The Bank’s main job is to keep inflation under control and it was rightly alarmed, as we all should be, when it spiked to 4% in April from 3.1% in March. The last thing any economy needs is for inflation to run out of control. Ask our neighbours in Zimbabwe how that worked out for them.The constitution compels the Reserve Bank to protect the value of the currency “in the interest of balanced and sustainable economic growth”. Sustainable growth cannot be achieved by the finance sector and partly credit-driven household demand as has been the case for so many years now.The sectors that propelled the economy at the start of democracy have all declined sharply both in terms of output and their contribution to GDP. We must get them performing optimally again for any real hope of getting growth above 1.1%.Sustainable growth cannot be achieved by the finance sector and partly credit-driven household demand as has been the case for so many years now.Manufacturing and mining are of particular concern: as the economy has steadily deindustrialised, the former’s contribution to GDP has slumped to 13%-14% from 22%-23% in 1994, while the latter now sits at 6%-8% from 15%-16%. There is evidence of the buoyancy that can take root when you invest in the sectors of the economy that can create jobs. As one economist recently reminded us, there was visible evidence of it ahead of the 2010 World Cup, with the bustle of construction that lifted not just the economy but also the collective national morale.We can recreate that by investing in the infrastructure maintenance, repair and development the economy is desperately crying out for. The private sector stands ready and willing to help finance this and just needs to see evidence of the political will in the government to facilitate and protect those investments.To reiterate, it is the job of the government, not the central bank, to put the measures in place that will encourage the private sector to participate in the sectors that can grow the economy meaningfully and sustainably.The role of monetary policymakers is to protect the rand value of those investments.Another pertinent point that is often overlooked is that the obsession with keeping interest rates low to protect indebted South Africans punishes those who are saving, whose money loses value when inflation surges out of control.Yes, there are millions of South African households whose income is so low they have nothing left to set aside after paying for each month’s bare essentials. But that is all the more reason to protect the value of that income, meagre as it is, by keeping inflation contained.

EDITORIAL | SA economy should not rely so heavily on consumption

Concerns over rate hike and its potential to stifle household spending highlights issue

590 words~3 min read