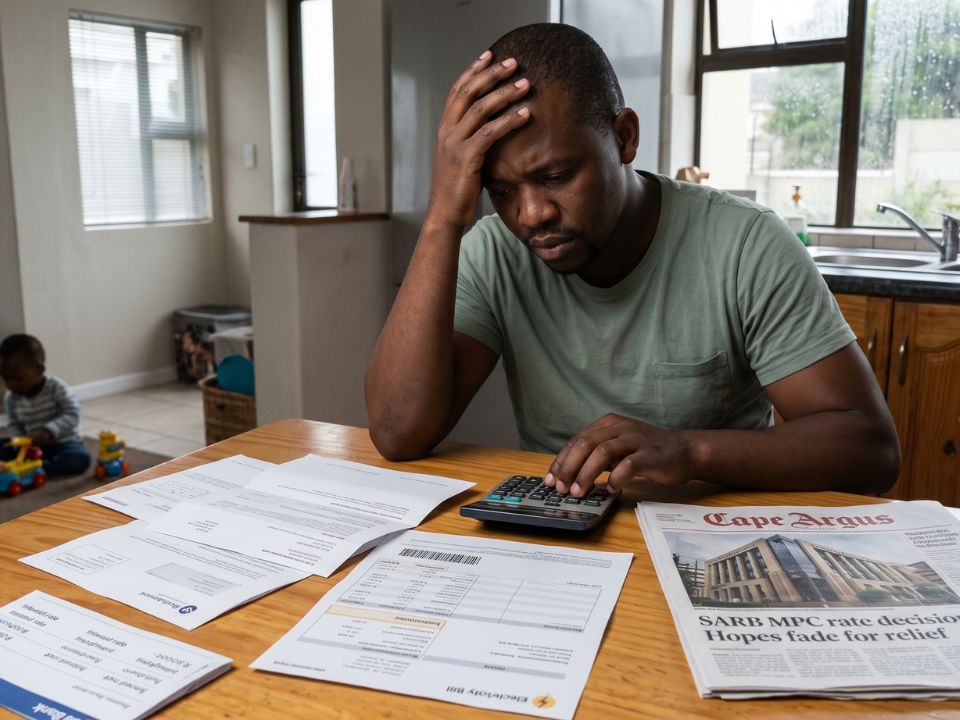

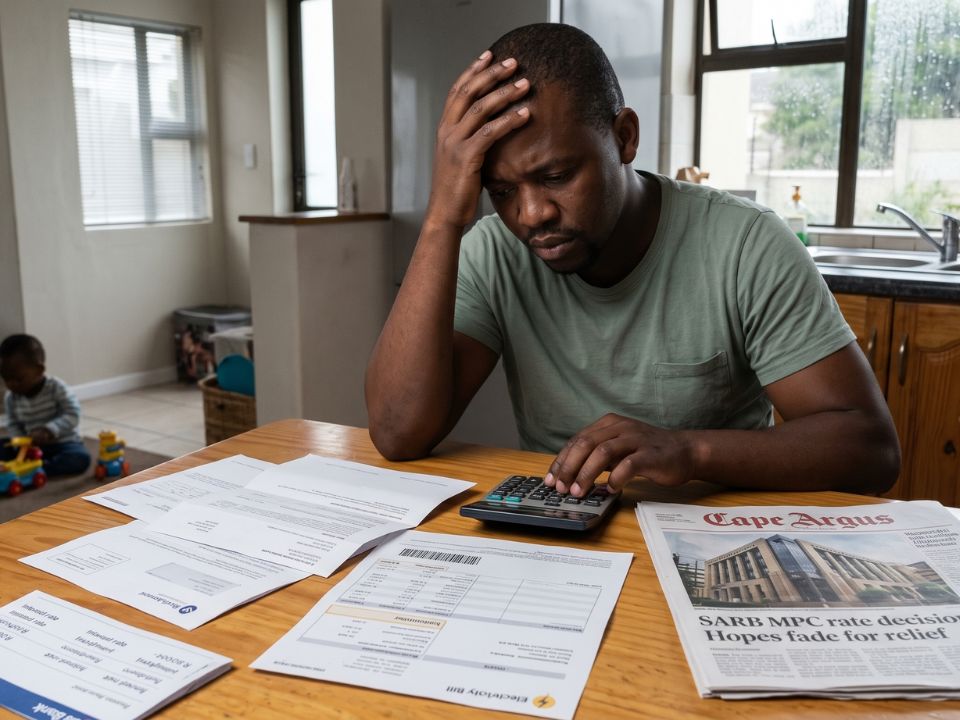

On May 28 Reserve Bank governor Lesetja Kganyago will read a statement much of the country is hoping not to hear. The fear is that the Bank’s monetary policy committee (MPC), rattled by an oil shock it did not cause, will lift the repo rate above its current 6.75% and make an indebted nation pay more to stay indebted.The instinct is to resist. I want to argue the harder thing: not that a hike would be pleasant — it would not — but that the alternative is quietly worse, and the discomfort is the point. Grant the obvious first. A higher rate raises the cost of bonds, vehicle finance and overdrafts. It taxes households that are already stretched. It leans on an economy that grew barely above 1% last year. These are real costs no honest analyst should wave away. But cost is not the same as harm, and the most expensive thing a country can do is misprice its own present. Consider four reasons the hardest rate decision may also be the kindest one. The subsidy nobody voted for Cheap money is never neutral. When rates sit low relative to inflation and the world, capital does not sit still. A rate held low — or merely left unchanged while others move — underwrites the machinery of financial engineering: companies borrow cheaply to buy back their own shares rather than build anything, and as cash and bonds stop outrunning inflation, investors crowd into equities, bidding valuations higher.The JSE inflates. Those who own assets of consequence — fund managers and the already-wealthy — capture the gains directly, while the ordinary saver benefits only second-hand, after the intermediary takes its cut. The savers are thanked for a meal they cooked but did not eat. And the loop tightens on itself. Concentrated gains widen inequality, and the wealthy spend a smaller share of each extra rand than the poor, their marginal propensity to consume being low, so the new paper wealth does not return to the tills as demand. Weak demand gives firms scant reason to invest, so the same capital circles back into assets, lifting valuations again. A higher rate is not a punishment of the poor; it is the withdrawal of a subsidy to the rich. The discipline of dearer debt Yes, a hike raises what the state pays on its debt, and the bill is not small: servicing it already swallows some R356bn a year, more than the country spends on health. But discipline arrives only when comfort leaves, and a rising cost of borrowing forces the question the Treasury has dodged for a decade: where does the money go? The auditor-general puts irregular expenditure at R42.5bn in the past year alone, most of it lodged in procurement, with the five-year pile of irregular, fruitless and wasteful spending now past R123bn. Yet that is only what an audit can see. The quieter haemorrhage is legal: the middleman who buys a box of tissues at one price and invoices the state at double that, a mark-up that trips no compliance flag. On a procurement bill past R1-trillion a year, trimming even a tenth of that intermediation — by insourcing capability and automating the routine — would recover near R100bn annually, roughly a third of the entire debt service bill. The department of home affairs has shown the shape of it: Smart ID turnaround cut by two-thirds, built in-house where queues and contractors once stood. A government of national unity is the rare configuration with the cover to do this, because no single party owns the waste. The currency in the room Here the doves underprice the risk. Rates are not set in isolation; they are set against the world. If South Africa holds while industrialised economies move, the rand weakens — not on sentiment, but on the arithmetic of relative return. A currency already swinging with every headline from the Iran-US war — near R17 to the dollar — slides further. And a weaker rand is no abstraction. It is the fuel price, and treating it as one line item is the economic equivalent of treating gravity as optional. Once it rises, transport rises, then food, then the cost of moving goods at all. The oil shock’s full force has not yet landed — spot prices stay partly suppressed by futures-market manipulation — but the bill is in the post. A rand weakened for domestic reasons would strike harder, sooner and wider than any rate increase. The cure for imported inflation is not to import more of it. The cost of borrowed time The fourth reason is the subtlest. Hold rates artificially low, and you distort every decision made against them. Households and firms commit to a price of money history says will not hold; when the oil shock filters through and rates rise, the defaults follow. Cheap money today is expensive money deferred, with interest. But the deepest reason is credibility. The Reserve Bank has only just won a tougher 3% inflation target, and the latest reading sits close to it. Defending that anchor while it is fragile costs far less than rebuilding it after it breaks — and a credible anchor lowers the risk premium on every rand the country borrows, the government’s included. Kganyago has called the current stance “moderately restrictive”. Restraint, held when it is uncomfortable, is precisely what makes it believed. But none of this makes a hike costless. It makes it honest. The question being asked on Thursday is not whether higher rates hurt — they do — but who is protected by keeping them low and who quietly pays for it. Sometimes the responsible thing and the popular thing part ways. This is one of those times. • Mafinyani is a senior partner in financial engineering & AI at the specialised finance, risk and applied technology firm Intellica Analytics.

RUFARO MAFINYANI | The case for the rate hike no-one wants

Cheap money's hidden cost widens the gap between rich and poor

975 words~4 min read