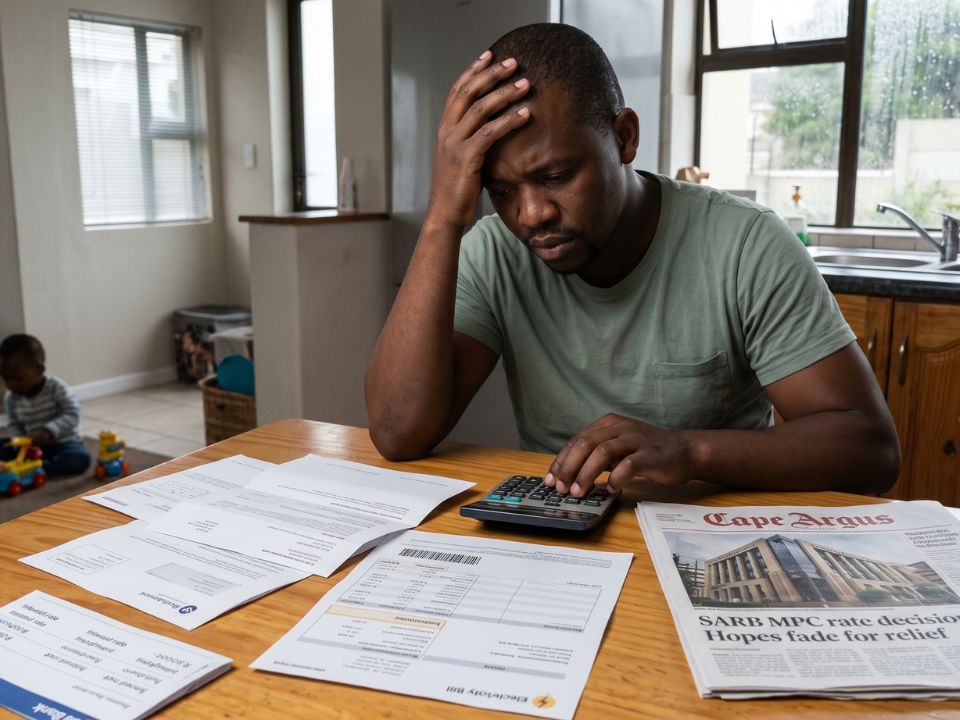

The Reserve Bank’s monetary policy committee (MPC) has sent signals that it expects a high-inflation, low-growth environment after raising the repo rate by 25 basis points to 7%.Governor Lesetja Kganyago said, given the current elevated levels of uncertainty, the MPC continued to find value in scenarios, with the current set exploring three risks — geopolitical shocks, severe weather events, and food and fuel prices.“One is a prolonged Middle East crisis, leading to higher food and oil prices, plus a weaker rand. The second included El Niño, a weather pattern that seems to be forming currently and which typically brings drought to parts of South Africa.“The third scenario added nonlinear effects — basically the risk that big shocks have proportionally larger effects on inflation, with more costs passed on to consumers. All these scenarios imply higher inflation and lower growth.” Four MPC members preferred a hike while two preferred no change, after the consumer price index (CPI) print for April surged to 4%. Kganyago said for the quarterly projection model, policy must achieve a balance, supporting economic activity while guiding inflation back to target over time. “The various scenarios all show some additional monetary-policy tightening. “The scenario with a longer Strait [of Hormuz] closure has inflation at about 5%, with two more hikes than the baseline. With El Niño added, rates stay high for longer. The most adverse scenario puts all the risks together, causing inflation to peak above 6%, requiring three extra hikes.”Dumisani Jantjies, a developmental macroeconomic analyst, said the rate announcement highlighted South Africa’s 32.9% unemployment reality check. “For a second-round wage-price spiral to happen, workers must have the power to successfully demand higher wages. But with South Africa’s official unemployment rate sitting at a staggering 32.9%, labour has virtually zero bargaining power. Most workers are terrified of losing their jobs and will simply absorb the pain of higher costs rather than demand raises.” North-West University Business School economist Prof Raymond Parsons said the MPC judged its majority decision to be a precautionary measure, although conceding there’s as yet no clear data that second-round effects are already strongly evident as a result of the global energy crisis and higher fuel prices.“The MPC majority view, therefore, seems to have already conflated the visible first-round inflation effects with possible ‘second-round’ ones later... to justify its immediate decision. Borrowing costs for business and consumers will nonetheless rise in what is already a weak growth environment, with South Africa’s GDP growth projections being generally cut, including by the MPC.”However, he said, the minority MPC view, believing that the timing was not yet right for a rise in rates, is convincing and that credible reasons exist for such a stance.“South Africa has economic buffers and some policy space to allow time for monetary policy to still navigate what remains a highly uncertain economic outlook. It would still have been possible for the MPC statement to convey a hawkish message to businesses and consumers about likely ‘higher-for-longer’ interest rate prospects, but combined with another pause in rates for now. “This would have made the MPC majority view appear less of an outlier compared to most other central banks, which, like the Reserve Bank, enjoy high credibility and have overwhelmingly decided to wait and see.”Parsons said the MPC statement itself referred to the extent to which the bulk of central banks around the world have so far kept rates on hold, given the dilemmas they faced in highly uncertain economic circumstances.Tertia Jacobs, treasury economist at Investec, said timing debates are unfolding at global central banks amid elevated uncertainty surrounding inflation persistence, geopolitical risks and the growth outlook, even as financial markets continue to price in a more restrictive monetary policy environment.“The governor indicated that a 50 basis point rate hike was also discussed by the MPC, although the committee ultimately concluded that there was insufficient information at this stage to justify a more aggressive tightening response.“The decision to proceed with a gradual adjustment, therefore, reflects both the unusually high level of uncertainty surrounding the inflation outlook and the MPC’s preference to remain data dependent as the oil shock evolves.”The central bank’s decision to revise inflation forecasts incorporated some degree of second-round pass-through from the recent energy shock, but the MPC acknowledged that upside risks remain, particularly should elevated fuel and utility costs become more broadly embedded in wage-setting behaviour and services inflation over time.“The governor also acknowledged that the current shock finds South Africa in a better space relative to previous external shock episodes. This aligns with the arguments we highlighted in support of maintaining rates unchanged at this meeting.”Toni Anderson, head of home services at Standard Bank, said the increase comes at a difficult time for consumers, with rising fuel prices already putting strain on household finances, but the repo rate remains at a multiyear low of 7%.“While this hike will disappoint many homeowners and people looking to buy property, earlier rate cuts have already made homes more affordable for many consumers. Understandably, consumers face a persistent strain from the rising fuel prices, which requires them to balance their budgets. But prioritising their home loan repayments remains critical.”Although unwelcome, the rate increase was not unexpected, Anderson said, as consumer inflation rose to 4% year on year in April, above the Treasury’s 3% target, placing inflation at the upper end of the target range, which allows for a one percentage point margin on either side.Business Times

Reserve Bank’s growth, inflation scenarios are tough across the board

Higher inflation and lower growth implied by all three eventualities MPC looked at

900 words~4 min read