Gita Gopinath, the IMF’s First Deputy Managing Director, just told global bond investors something they probably already feel in their portfolios: the ground beneath them is shifting. In a Bloomberg Surveillance interview, Gopinath described bond markets as being “in a fragile place,” driven by high and increasing debt levels that markets are no longer willing to shrug off.

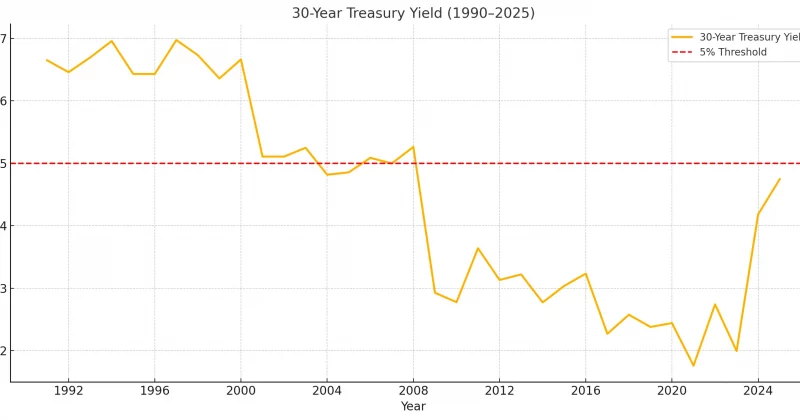

The timing matters. US 30-year yields are trading well above their recent averages, and Gopinath flagged visible stress in both French and UK bond markets.

The debt tolerance problem

Gopinath’s core argument is straightforward. Advanced economies have accumulated public debt ratios that became significantly more pronounced in the wake of post-pandemic fiscal spending. The problem isn’t just the size of the debt. It’s that investors are now demanding higher compensation for holding it.

The stress in French and UK bond markets is particularly telling. France has been grappling with political uncertainty and fiscal credibility questions for months. The UK’s bond market, still nursing scars from its 2022 gilt crisis, remains sensitive to anything that smells like fiscal indiscipline.