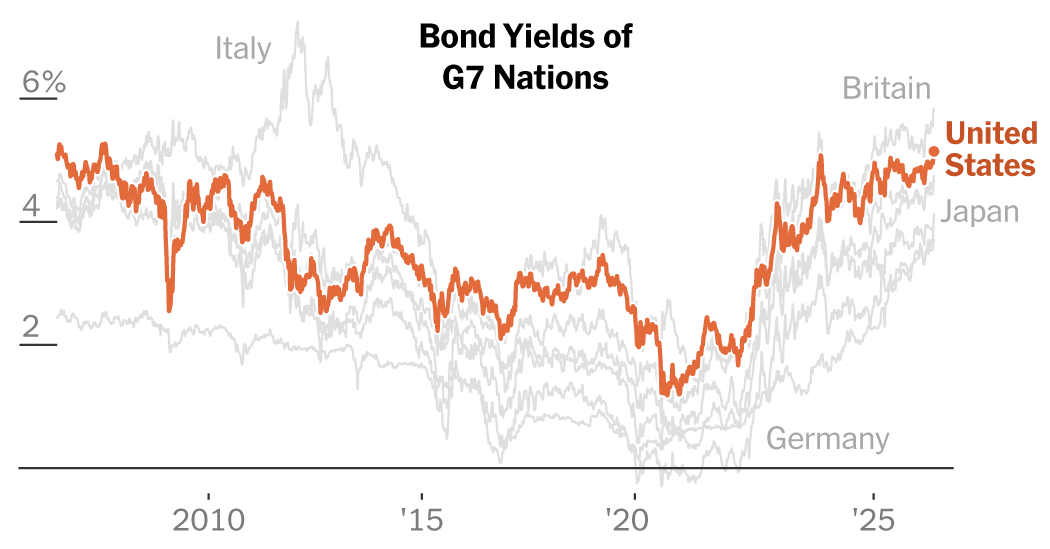

The world remains mired in chaos and uncertainty. This anxiety now reflects starkly in the bond yields. The yield on the 30-year US Treasury bond recently jumped to 5.2%—its highest since 2007. In India, the yield on the benchmark 10-year government bond has jumped from 6.6% to 7.1% in three months. Long-term yields rise when investors demand a higher return for holding bonds. This is compensation for the loss of purchasing power from higher expected inflation.The West Asia conflict and the continued blockade of the Strait of Hormuz have become severely destabilising, stoking global inflation risks.How should bond investors position themselves?From rate cuts to rate hikes When the Reserve Bank of India (RBI) initiated its much-anticipated rate cuts in early 2025, it seemed like bonds were set for a prolonged spell of gains. When interest rates fall, bond prices rise. But after front-loading rate cuts by June 2025, the RBI quickly pivoted to a neutral stance, signalling limited room for further cuts. After a final 25-basis points (bps) rate cut in December, the central bank ended the year with a cumulative easing of 125 bps (one basis point is one-hundredth of a percentage point). It has since kept rates unchanged, keeping a wary eye on significant developments globally.Domestically, while inflation has so far remained contained, continued disruptions to critical supply chains threaten to send prices soaring. The rising crude oil bill is likely to widen India’s current account deficit (CAD), contributing to a steadily weakening rupee. Forecasts of uneven or sporadic monsoon pose additional risk to inflation. This build-up of a ‘perfect storm’ has effectively shut the door on any rate cuts in the near future.Kunal Valia, Founder and Compliance Officer of StatLane, a Sebi-registered research analyst, says, “At this stage, the rate easing cycle appears largely complete. Going forward, a combination of domestic and global factors is likely to keep bond yields elevated and limit the scope for any meaningful decline.”With markets adjusting to higher inflation expectations, Valia reckons bond yields will remain broadly range-bound, albeit with a mild upward bias. The 10-year government bond yield is likely to trade in the 6.9– 7.3% range over the coming quarters.Experts suggest rate hikes could happen sooner than expected.“The RBI is likely to hike rates as well imminently,” believes Vishal Goenka, Co- Founder, Indiabonds.com. If the current situation persists, the path of least resistance would be for the regulator to hike rates sooner than expected, insists Suyash Choudhary, Head–Fixed Income, Bandhan Mutual Fund. “With average Consumer Price Inflation (CPI) for the current financial year likely to be in the 5–6% band, it almost automatically follows that the RBI will have to undertake some rate hikes.”As a base case, one should expect hikes of 50-75 bps over the course of the rest of this fiscal year, according to Choudhary.

Debt funds: Is it time to exit long-duration bond funds as rate hike risks rise? - The Economic Times

The RBI’s rate-cut cycle is behind us. Experts foresee 50–75 bps of hikes. Your bond portfolio needs to reflect that.

949 words~4 min read