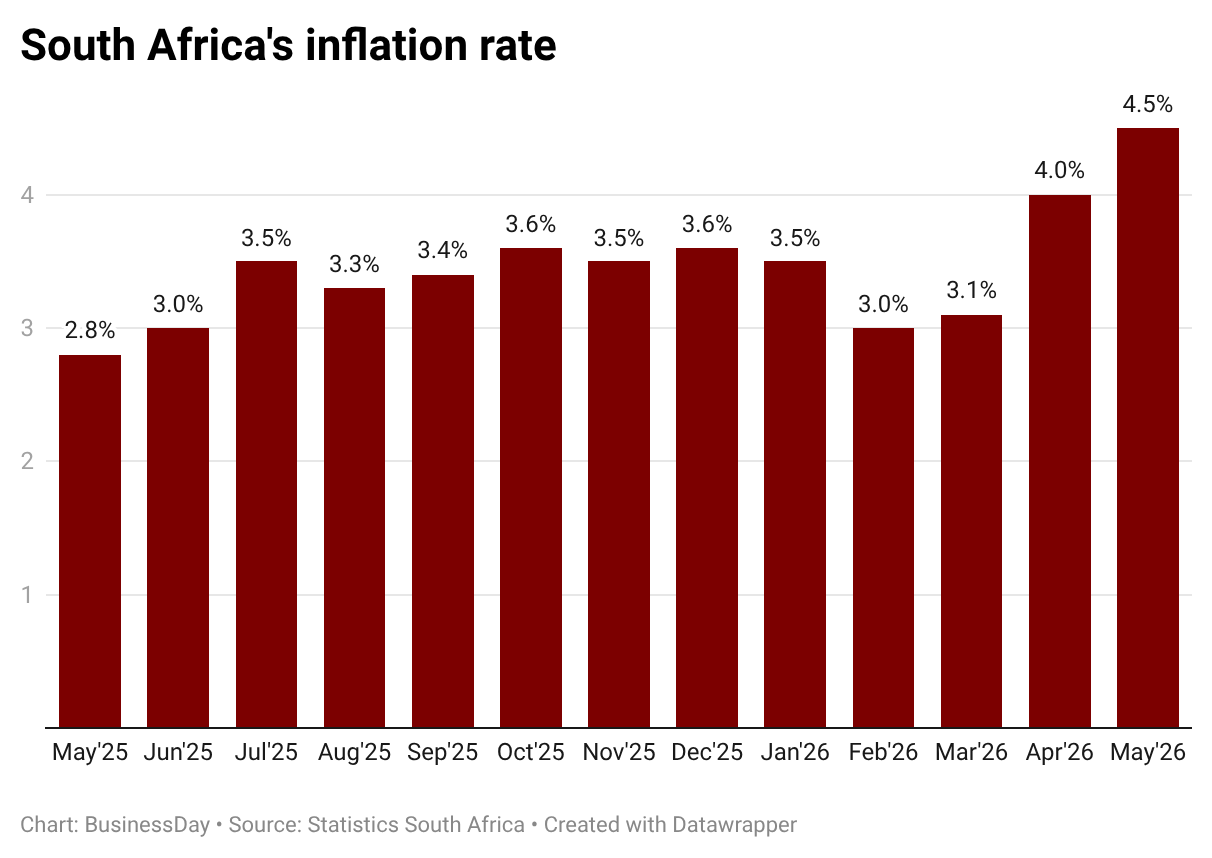

The April 2026 inflation data released by Stats SA on May 20 confirmed our most pressing anxieties. As the economic fallout from the Middle East conflict washes onto our shores, domestic inflation is climbing. This is not an abstract macroeconomic phenomenon; it is a direct assault on the cost of living for millions of South Africans. Households are paying significantly more at the fuel pumps and for basic goods, yet the fundamental value of what they are purchasing remains entirely stagnant. With April’s electricity tariff hikes compounding the pressure and the delayed shock of $80-plus oil yet to fully manifest on our supermarket shelves, the South African consumer is being suffocated. The state is currently caught in a contradictory trap: while temporary fuel relief attempts to give with one hand, the reality of paying VAT on drastically inflated prices takes away with the other. The tragedy of our current policy predicament is that it is largely self-inflicted. During the 2025 medium-term budget policy statement (MTBPS) discussion the government aggressively championed a lower inflation target (from 6%) to 3% with a tolerance band of plus or minus one percentage point. (Karen Moolman) This move was executed despite fierce pushback from developmental economists, civil society, labour, the parliamentary budget office and other stakeholders through a formal parliament submission, all warning about the lack of empirical evidence supporting such a restrictive stance for a developing economy. The core message of this unified pushback was unequivocal: elevating strict price stability above all other macroeconomic objectives (such as growth, employment and inequality) in a fragile, developing economy carries a devastating “sacrifice ratio”. The parliamentary budget office correctly warned attempting to bludgeon structural or imported inflation into an artificially low target using aggressive interest rate hikes would systematically choke off domestic demand, deter fixed investment and drastically worsen the unemployment crisis. As the Reserve Bank monetary policy committee comes to a decision later today, predictable voices are clamouring for an interest rate hike to artificially drag inflation back into this new target. This argument is not only premature, it is fundamentally flawed. The inflation we are experiencing today is entirely imported, and now we know how it operates. It is a supply-side shock driven by geopolitical disruptions and global oil market panic.You do not need to be an economic analyst to understand a basic truth: domestic interest rates cannot dictate global fuel prices, and nor can they end a war. Fighting this imported inflation with domestic monetary tools is worse than a “wait-and-see” approach, it is active self-sabotage. These global prices will naturally recede once hostilities cease. Punishing South Africans in the interim achieves nothing but economic destruction. Consider the reality of a 25-basis point interest rate increase right now. For households it means a punitive increase in the cost of servicing debt, from home loans to credit cards, stripping away whatever disposable income remains. For the broader economy it stifles investment and expansion, directly contradicting the need for job creation. The Quarterly Labour Force Survey released on May 12 paints a grim picture of worsening unemployment, which showed a 1.3% decline in employment in the first quarter. For public finances, higher rates dramatically inflate the state’s debt servicing costs, crowding out the social wage. It would be remiss not to acknowledge the genuine strides made by the state on the structural front. The government’s supply-side interventions, spearheaded by Operation Vulindlela, are taking hold. We are seeing tangible, reported progress in stabilising energy security and initiating much-needed reforms in our freight and logistics networks. Yet herein lies the paradox; despite these structural victories, our broader macroeconomic performances continue to deteriorate or underperform. Why? Because fixing the supply side of the economy is meaningless if there is no demand to meet it. The economy desperately requires robust demand-side interventions to stimulate growth and job creation.Yes, maybe this is largely a fiscal policy prerogative. However, in our current fragile context, deploying a blunt monetary instrument such as an interest rate hike would be devastating. It would certainly not be complementing fiscal policy, as it is often argued to be an important formula to get the economy moving. It would systematically dampen the exact domestic demand we need to capitalise on our supply-side reforms, in effect starving our recovering productive sectors of their consumers. When we look beyond our borders it is clear South Africa is somewhat an outlier in our overly passive macroeconomic approach. When faced with similar imported supply shocks the Bank of Japan explicitly refused to hike interest rates, recognising punishing domestic consumers cannot cure global oil prices. In Europe, states such as France and Spain deployed aggressive tariff shields and price caps, while the UK levied windfall taxes on energy giants to fund direct relief for households. Even our developing peers in Latin America, such as Mexico and Brazil, aggressively slashed fuel and transit taxes to insulate their citizens. These jurisdictions acted as protective shields for their economies. By allowing an interest rate hike our state would be choosing to outsource macroeconomic crisis management to the monetary authority interest rate lever, a tool that destroys domestic demand while completely failing to lower the price of a barrel of oil in the Middle East. South Africa’s macroeconomic policy has remained paralysingly passive for too long. We have stubbornly elevated a single objective — price stability — above all others, sacrificing growth, employment and structural equality in the process. When an economy faces stagnant growth alongside an aggressive, externally driven spike in the cost of living, orthodox tightening fails. We urgently require a shift toward a more active and developmental macroeconomic strategy. Policy must prioritise shielding poor and working-class households from external shocks rather than protecting profit margins. Attempting to win an impossible battle against global inflation will only worsen our domestic macroeconomic crises. It is time for the state to abandon its passive stance, absorb the lessons of the past few months, and actively construct a resilient economy that works for its people. • Jantjies, a former director of of the parliamentary budget office, is a senior macroeconomic and fiscal analyst, professor of practice at the University of Johannesburg, and chair of the African Network of Parliamentary Budget Offices.

DUMISANI JANTJIES | State must be proactive in inflation battle

Why fighting imported price increases could break SA households

1,033 words~5 min read