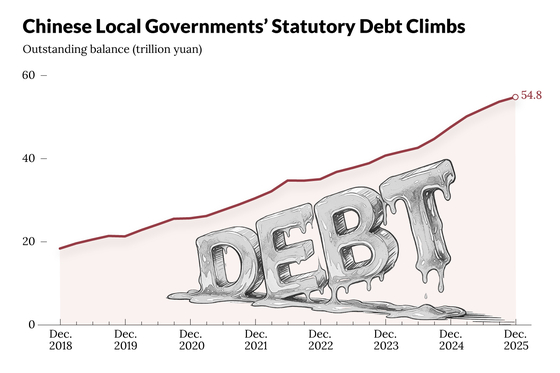

China has a debt problem disguised as a debt solution. The country’s massive effort to clean up hidden local government borrowing is succeeding on paper, with provinces burning through their refinancing allowances at an impressive clip. The catch: the cleanup is strangling the very economic growth Beijing desperately needs.

The $1.39 trillion cleanup

In November 2024, Beijing launched a CNY10 trillion (roughly $1.39 trillion) debt-resolution program targeting local government financing vehicles, or LGFVs. These are essentially shell entities that local governments used for years to borrow money off the books, funding everything from highways to housing developments without technically adding to official debt tallies.

The program was designed to run through 2028, with CNY6 trillion earmarked specifically for refinancing LGFV debt through special bond issuances. By mid-2026, provinces had already utilized approximately 94% of that CNY6 trillion refinancing allowance, issuing over 1.62 trillion yuan in the first half of the year alone.

Provinces like Jiangsu, Shandong, and Zhejiang have led the charge in bond issuances. On one metric, the program is a clear success: LGFV debt growth slowed to approximately 3.3% in 2024, a dramatic cooldown from the double-digit growth rates these vehicles had been posting for years.