As far as President Donald Trump is concerned, the summer fun is already over. He outraged traditionalists by staging a U.F.C. fight night at the White House for his eightieth birthday, celebrated the two-hundred-and-fiftieth anniversary of the country’s founding by branding the Democrats as “communists,” and flew to a NATO summit in Turkey, where his fellow-strongman Recep Tayyip Erdoğan rolled out a turquoise carpet for him. Now it’s back to the hard stuff: the lingering conflict in the Middle East, the economy, and the midterm elections, which are less than four months away.These three phenomena are interlinked, and not in a good way for Trump. At the start of this year, the White House and Republican leaders were hopeful that, come summer and the midterm-campaign season, they would have some positive economic developments to point to. “Growth is exploding,” Trump told the Detroit Economic Club, in January. “Productivity is soaring. Investment is booming. Incomes are rising. Inflation is defeated.” Trump is an inveterate bullshitter, of course, but his Administration does employ some economists who have at least one foot in reality, and they, too, were feeling hopeful.Although the U.S. economy certainly wasn’t exploding with vigor, it had defied fears that his blanket tariffs would plunge it into a recession. In 2025, G.D.P. grew by 2.1 per cent—below the growth rates from the Biden years, but respectable enough. The inflation picture also seemed benign. In January, prices were rising at an annualized rate of 2.4 per cent—not far off the Federal Reserve’s two-per-cent target. This convergence raised hopes among Trump’s advisers that the central bank could soon resume cutting interest rates. Meanwhile, buoyed by enthusiasm for A.I., the stock market was hitting records on a regular basis, and Big Tech companies were making huge investments in chips, servers, and software. In the first three months of the year, these expenditures boosted G.D.P. by roughly 1.3 per cent on an annualized basis. “We’re getting very strong disinflationary growth,” Joseph Lavorgna, a seasoned Wall Street economist and then a counsellor to the Treasury Department, told CNBC, in February.Unfortunately for G.O.P. politicians who are on the ballot this fall, this optimism turned out to be largely wishful thinking. To be sure, the mania for A.I. investments continues unabated. Taken as a whole, though, the economy seems to be plodding along much as it did last year. In May, inflation rose to the highest level in more than three years—4.2 per cent—and last month job growth slowed sharply. Not surprisingly, many Americans are still in a funk over the cost of living, and Trump’s outlandish claims, which he still insists on repeating at every opportunity, ring hollower than ever. In a recent Harris poll, just sixteen per cent of respondents said the economy is getting better; fifty-seven per cent said it’s getting worse. (Even among self-identified Republicans, approximately one in four said things are improving.) Given these sentiments, it’s hardly surprising that Trump’s job-approval rating on the economy is in the cellar: thirty-two per cent, according to an Economist/YouGov survey released last week. In the same poll, his approval rating on inflation was even lower: twenty-seven per cent.Surely, the Trumpian economic scenario was wildly overoptimistic to begin with. (In January, Howard Lutnick, the Secretary of Commerce, predicted that G.D.P. growth would hit more than five per cent in the first quarter.) But the A.I.-investment boom is genuine enough; how long it can last is another matter. Conceivably, 2026 could have been a year of decent G.D.P. growth, falling interest rates, modest inflation, and rising real wages. But then Trump, in concert with Israel, decided to bomb Iran. As the war expanded, the price of a barrel of crude oil rose from about seventy dollars to more than a hundred and ten dollars. The cost of a gallon of gasoline, which had been under three dollars, on average nationwide, jumped to $4.50. And the prices of other oil products that play a crucial role in the economy, including fertilizers and plastics, also spiked.These developments amounted to a “self-induced supply shock” for the American economy, Lavorgna, who left the Trump Administration in March, told CNBC, last month. He went on: “The problem is this war . . . from a forecasting perspective, it changed things, and changed things monumentally.” The pickup in inflation didn’t go unnoticed at the Fed, which has a legal mandate to insure price stability. At a policy meeting last month, nine of the eighteen officials on the Fed’s policymaking committee indicated that they expected at least one rate hike by the end of the year. Even Kevin Warsh, the Republican financier whom Trump handpicked as the new chair of the Fed, made noises about the need to contain inflation.It was in this context that the Trump Administration reached a provisional agreement with the Iranian government, formalized in a memorandum of understanding, to end the war and reopen the Strait of Hormuz. After the deal was announced, the price of crude, which had already fallen significantly in anticipation of an agreement, dropped further: by the start of last week, it was close to its prewar level of some seventy dollars. Later in the week, however, after hostilities resumed and Trump declared the ceasefire “OVER,” transit in the strait came to a virtual stop. The price of Brent crude briefly jumped back above eighty dollars, before closing at about seventy-five dollars on Friday. The price of gasoline, after dropping below four dollars in June, has started to creep up again.Even before this uptick, Trump had been complaining that the cost of gasoline hadn’t fallen as far as the price of crude had, and he accused Big Oil companies of price gouging. They will certainly pad their profits if they can. But it was Trump’s reckless decision to start a war with Iran that threw the industry into turmoil and upended global supply chains. Energy experts have said all along that repairing this damage would take some time, even if a sustainable peace deal was reached. The sudden emergence last week in the Philadelphia area of a couple of dozen “Freedom Fuel” stations that are selling gas at discount prices doesn’t alter this larger reality or make Trump less culpable. (It’s still not entirely clear who is behind the “Freedom Fuel” initiative. A spokesperson for the White House told CNN that the Trump Administration isn’t involved.)On Tuesday, the Bureau of Labor Statistics will release the June Consumer Price Index. Reflecting the drop in gas prices last month, it will likely show the headline rate of inflation falling below four per cent. (An “inflation nowcast” maintained by the Federal Reserve Bank of Cleveland predicts a year-on-year figure of 3.71 per cent.) This may well give Trump something to trumpet for a day or two, but it’s unlikely to change the mood of ordinary Americans, who want to see the prices of groceries and other essential items falling—not merely going up at a slower rate. The crisis of affordability was, arguably, the biggest factor in Trump’s victory in 2024. But, since reëntering the White House, he has only accentuated the problem: by imposing hefty tariffs on countless imported goods, and by starting a needless war. Adopting the Red Scare tactics of the last century seems unlikely to save Republicans from the political consequences of this folly. ♦

Donald Trump’s Needless War with Iran Is His Biggest Economic Blunder

As the midterm elections approach, gas prices have started to rise again, and Trump’s poll ratings are in the cellar.

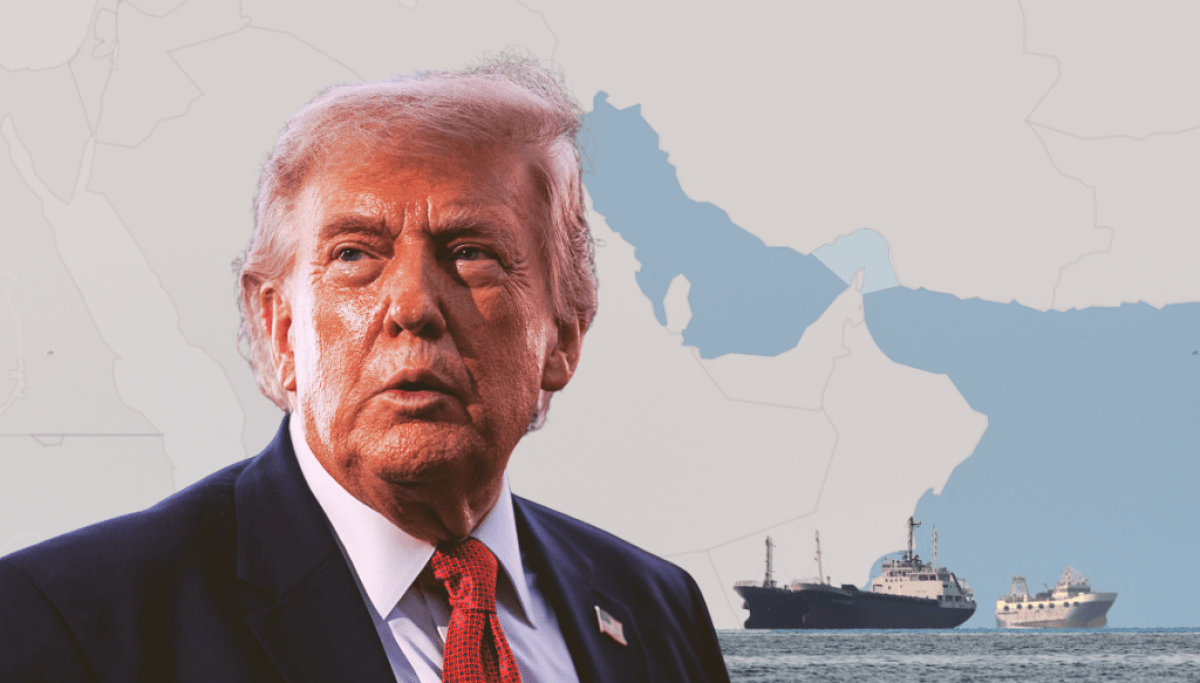

1,219 words~6 min read