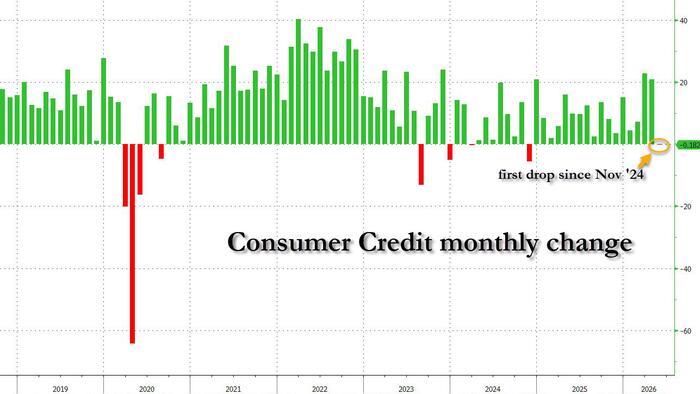

Americans quietly stopped reaching for their credit cards in May. The Federal Reserve’s G.19 Consumer Credit report, released July 8, 2026, showed total consumer credit posting a flow of negative $2.2 billion on an annual basis, the first flat or declining reading since 2024.

Credit cards are where the action is

Revolving credit, which is mostly credit card balances, fell at an annual rate of 4.7% in May. In dollar terms, that translated to a month-over-month drop of $5.3 billion, pulling the total outstanding revolving credit balance from $1,349.5 billion in April down to $1,344.2 billion.

Credit card APRs have been running between 20.9% and 22.2%, a range that turns an average balance into a serious recurring expense.

The nonrevolving side of the ledger, which covers auto loans and student debt, held up better. That category grew at a 1.6% annual rate in May, providing enough of an offset to keep the overall consumer credit number from collapsing outright. But a modest gain in auto and student lending could not compensate for what happened in revolving credit.