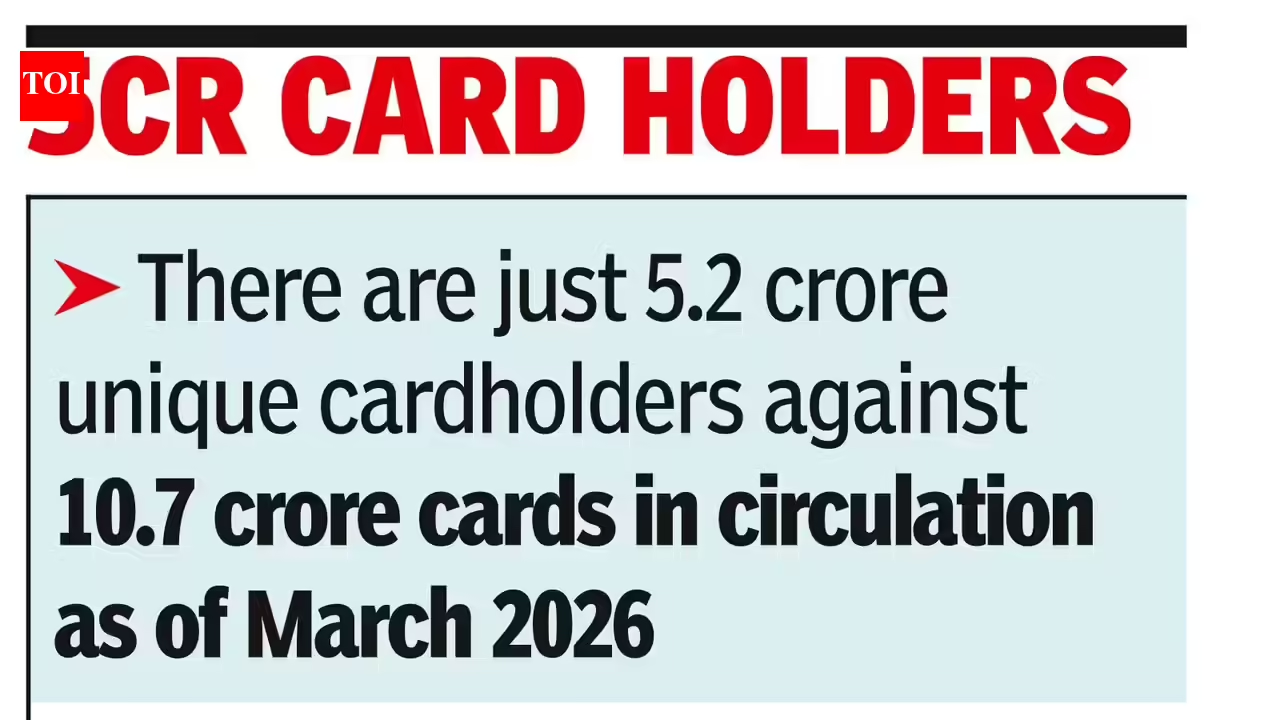

Mumbai: Credit cards are steadily losing their position as the default unsecured borrowing product, ceding ground to small-ticket personal loans and other consumption-linked credit, according to a TransUnion CIBIL report. The share of open credit cards in India's overall unsecured credit products has fallen to 38% in 2026 from 56% in 2016, it said. Small personal loans of up to ₹50,000 have steadily gained share during this period. Card balances as a proportion of total consumption-credit balances in the industry, meanwhile, have stayed flat at about 15-16%."Cards are now increasingly competing within the same consumption-driven small credit space, rather than operating as a default option," the report said. Even as card balances increased eightfold in a decade to more than ₹3 lakh crore at the end of March this year, risk spilled across products, delinquency data showed.Credit information company TransUnion CIBIL segmented cardholders into four behavioural personas - occasional card users, card-centric users, diversified credit users and high exposure users - and tracked how missed payments on any credit product correlated with card delinquency specifically.Among occasional card users, who use cards mainly for payments and rewards, just 4% missed at least two payments across products in a 12-month period, and their card delinquency rate (90-plus days past due) was only 0.6%.

Credit cards lose ground as small-ticket personal loans gain traction: CIBIL

Credit cards now hold 38% of unsecured credit, down from 56% in 2016. Small personal loans under fifty thousand rupees have gained significant market share. Card balances remain stable at fifteen to sixteen percent of total consumption credit. Delinquency data shows risk spilling across various credit products. Occasional card users exhibit low delinquency rates across their credit portfolios.

211 words~1 min read