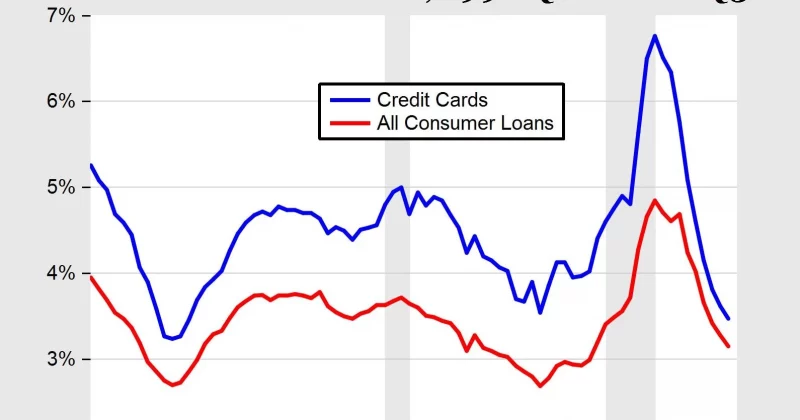

American consumers are falling behind on their credit card payments at levels not seen since the period after the 2008 financial crisis, according to a report from the Federal Reserve Bank of New York. About 13% of all U.S. credit card balances were at least 90 days overdue in the first quarter of 2026. This is the highest delinquency level since 2011, when the country was still recovering from the Great Recession.U.S. credit card debt hit $1.25 trillion, with 13% of balances overdue by 90 days, levels last seen post-2008 crisis.The report also notes that America's total credit card debt has reached $1.25 trillion, which is close to the highest level ever recorded. Experts say a growing number of consumers have fallen into serious credit card debt and are finding it difficult to recover. Grace Zwemmer, a U.S. economist at Oxford Economics, said the data shows increasing financial vulnerability among a section of consumers. Zwemmer said the problem is not that many new people are missing payments, but that people who were already behind are falling even deeper into debt, as quoted by USA Today report.Credit card debt was falling during the pandemicCredit card debt fell during the pandemic as stimulus payments and lower spending helped consumers pay down balances. Debt began rising again as inflation and borrowing costs increased.U.S. credit card balances crossed $1 trillion for the first time in early 2023. The delinquency rate continued to rise in the following years, reaching 13% in the first quarter of 2026. That is close to the Great Recession peak of 13.7% recorded in early 2010.Also read: IRS warning: Some credit card rewards may be taxedOdysseas Papadimitriou, founder and CEO of WalletHub, said to USA Today, the country is moving in a worrying direction. The average American household currently carries $11,169 in credit card debt, he added.Inflation and high interest rates are making things worseFinancial experts say many cardholders continue to struggle because prices remain high and credit card interest rates are still elevated. The average credit card interest rate rose from 14.6% in February 2022 to a peak of 21.8% in August 2024.Interest rates have remained very high, averaging about 21% in February 2026. Experts say the growing amount of overdue debt suggests some consumers are trapped in debt and may not have a realistic path to catch up. Papadimitriou said many consumers who get into financial trouble no longer have easy options to escape it, as cited by USA Today.Many Americans are still managing their cards wellDespite rising debt concerns, millions of Americans are handling their credit cards responsibly. Around half of all U.S. credit card holders carry debt from month to month. The other half pay their full balance every month and avoid paying high interest charges. A report from the Federal Reserve Bank of Philadelphia found that while overdue debt amounts are increasing, the number of delinquent accounts has remained fairly stable.Experts say this is not another 2008 crisisMortgage delinquency rates remain far below the levels seen during the Great Recession. The 2008 financial crisis was largely caused by problems in the housing market, unlike today's situation. Experts do not believe the current credit card problems are comparable to the crisis that led to the Great Recession.Experts note that credit card delinquencies are still rising, but the pace of increase has slowed compared with two or three years ago. The number of newly delinquent credit card accounts remains elevated but has generally stabilized, as cited by USA Today.

US credit card debt hits $1.25 trillion as more borrowers fall behind: Are Americans heading back 18 years?

U.S. credit card debt hit $1.25 trillion as delinquencies reached a 15-year high. Inflation and high interest rates are leaving more Americans behind.

581 words~3 min read