Japan is trying to put out two fires with one hose. The yen recently slid to 160.3 against the US dollar, prompting finance ministers to warn of “decisive action.” Meanwhile, 10-year Japanese government bond yields have surged to multi-decade highs around 2.6% to 2.74%. The problem: fixing one of these almost certainly makes the other worse.

The numbers tell the story

Japan has already thrown serious money at this problem. The government has intervened to the tune of 11.7 trillion yen, roughly $73 billion, to support the currency, with most of that spending concentrated between late April and early May.

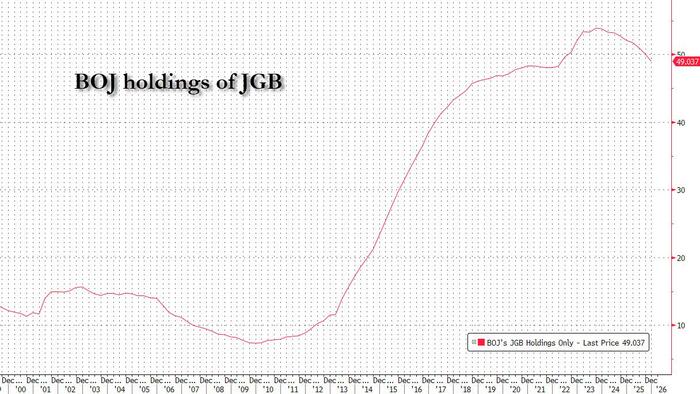

On June 16, the Bank of Japan raised its policy rate to 1%, marking the highest level since 1995. That’s a milestone for a central bank that spent decades in ultra-loose territory, including years of negative interest rates and yield curve control. The rate hike represents the BOJ’s continued march toward monetary normalization, driven by rising inflation that Japan ironically spent years trying to create.

Here’s the thing. That rate hike is supposed to help the yen by making Japanese assets more attractive to hold. But it also raises borrowing costs across the economy, and Japan’s public debt exceeds 250% of GDP. Every basis point of higher rates translates into significantly larger debt-servicing costs on a balance sheet that was already eye-watering.