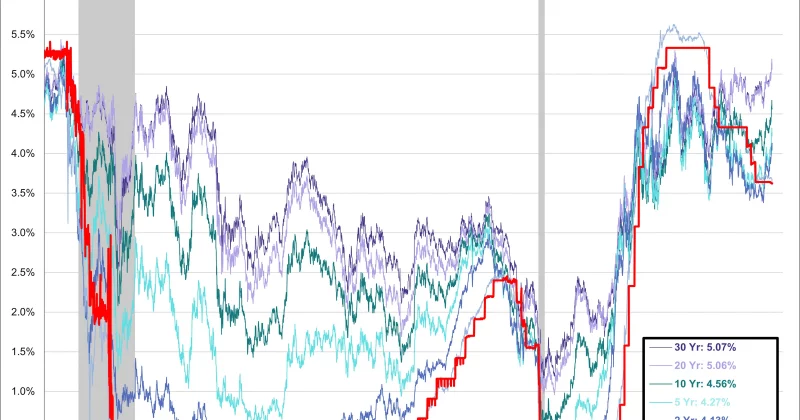

The bond market has a new north star, and it sits right in the middle of the yield curve. Fixed-income managers are gravitating toward five-year Treasury securities as Kevin Warsh’s tenure atop the Federal Reserve introduces a policy regime that’s already rattling longer-duration debt.

Warsh, who took office as Fed Chair on May 22, 2026, has wasted no time signaling that the Powell era’s communication style is over. The result: a scramble among portfolio managers to reposition around intermediate maturities, where the risk-reward math looks most favorable under a hawkish, less predictable central bank.

The Warsh doctrine takes shape

Warsh held the federal funds rate steady at 3.5%-3.75% during the June 17 FOMC meeting, while making an explicit move toward minimizing forward guidance. For bond traders who spent years parsing every syllable of Powell’s press conferences for clues about future rate moves, this is like having the answer key taken away mid-exam.

Warsh also announced an ambitious plan to restructure the Fed’s balance sheet, currently hovering around $6.7 trillion. His goal is to strip out all mortgage-backed securities and hold only Treasuries.