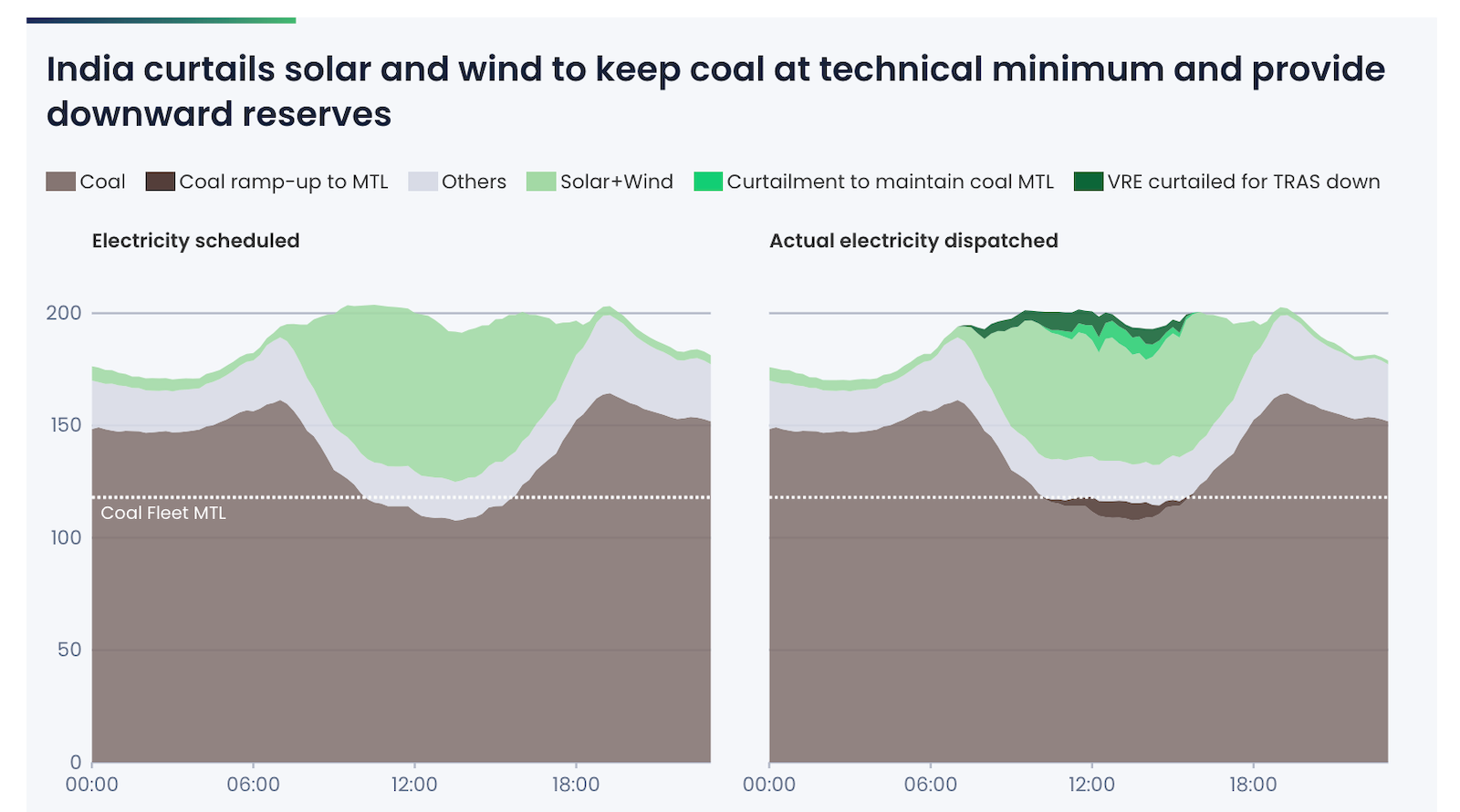

Green energy curtailment due to transmission constraint was mainly in northern and western regions whereas there was idle capacity in substations in other regions

| Photo Credit:

Renewable energy (RE) growth in India has been robust and is getting global recognition. We have achieved one of our NDC commitments of more than half the generation capacity coming from non-fossil sources by 2030 well in advance by five years. India has added a record 52 GW of renewable capacity in the last fiscal year and has a pipeline of about 232 GW RE capacity under execution and tendering.The target of 500 GW non-fossil capacity looks achievable. Solar capacity of more than 150 GW stands out in total RE capacity and is in line with the pathway of our power sector to net zero by 2070. As per NITI scenarios, solar capacity is projected to grow to around 1500 GW by 2050 in Current Policy Scenario and to about 2400 GW in net zero scenario.We plan to add 50 GW of solar capacity per year and have a strong pipeline. However, concerns have started emerging in terms of more than 40 GW unsigned PPAs (power purchase agreements) for awarded capacities, and recurrent curtailment of solar generation. This article attempts to analyse the reasons for these headwinds and suggest a plan of action for addressing the same.Causes for curtailmentAccording to a recent report, total green energy curtailment during January-March 2026 was 470 million units, of which, 300 million units was due to transmission constraints. Curtailment due to transmission constraint was mainly in northern and western regions whereas there was idle capacity in substations in other regions. This was largely due to a rush to set up capacities in RE rich areas driven by waiver of transmission charges.The cause of remaining curtailment was lack of demand in the system in peak solar generation hours. This problem is going to aggravate in future as the solar additions are likely to surpass the demand growth in future years. Peak demand in solar hours increased at the rate of about 11 GW per year between 2024 and 2056, and that too only for a few days in a year. If we intend to add 50 GW annually of solar capacity in the next few years, the system is bound to see much higher solar time surpluses on most of the days resulting in increasing levels of curtailments. Avoiding this will need expensive large scale storage addition unless we take other urgent interventions to increase the day time demand.Reluctance to sign PPAs can be traced to increasing pressure on consumer tariffs. It has been the experience of several countries including Germany and Australia that affordability gets larger attention as system costs start rising with increasing share of RE in overall supply mix. India has also started seeing the same. Average power purchase cost of the Discoms was ₹4.72 per unit in FY21 which increased to ₹5.38 in FY25. A recent tender in Uttar Pradesh for supply of RE through BESS in evening four peak hours discovered a tariff of ₹6.45 per unit even after incorporating VGF (viability gap funding) by the Central government. If we exclude the support of VGF, the cost of peak RE power through BESS will be close to ₹8 per unit as against the rate of power in power exchange being around ₹6.5 in evening peak hours in FY26.The cost of integrating daytime extra solar generation in the power system becomes even higher in a State like UP where annual average demand in solar hours has been generally significantly lower than non-solar peak. Backing down pithead coal based stations with energy charges much lower than cost of solar energy for accommodating solar surpluses is leading to higher system costs. Also, the flexibility costs to accommodate high solar surpluses are comparatively much higher in our system which is low on wind and gas peakers. Wind provides peak time green energy and gas peakers have capital cost lower than coal based plants.In addition, the successive mandates to use domestically manufactured solar cells and wafer/polysilicon are also temporarily raising prices of solar generated electricity. The indirect concessions like net metering, must run status, and socialisation of waived transmission charges are further pushing up the average cost to serve for Discoms which is ultimately borne by the common consumers.Overall, if we try to integrate additional solar capacities at a rate higher than what a power system of a State can absorb by way of incremental demand in solar hours, it is bound to show in higher system costs. Consequently, to keep the tariff hike under control, States will come under increasing pressure to give additional tariff subsidies which has already become a financial strain on their fiscal health.Holistic approach neededTherefore, going forward, we need to adopt a holistic and calibrated approach while accelerating the expansion of RE capacity in our generation mix. Immediate priority should be to set the national targets of RE capacity addition based on the aggregate picture emerging from the studies of the States’ power systems so as to ensure the affordability.While undertaking resource adequacy planning exercise, aspiring for zero solar curtailment is not good economic policy. It will raise the system costs and also kill the markets for flexibility products. Most of the countries with higher share of solar have curtailment at the proportion of total solar generation much higher than what we are seeing in India. What we need is a predictable curtailment framework which leads to least cost solution at system level and also fairly compensates the affected generators through market based instruments, not through must-run. The calls of the solar industry to mindlessly add high cost inter-State transmission lines to evacuate solar energy without properly evaluating the other options of DRE (decentralised renewable energy) and distributed storage assets are also not aligned to the objective of least cost supply to the consumers.Higher RE capacity addition can be achieved in a cost-effective manner only if we take steps in advance to accelerate the electrification of energy services for increasing the demand for electricity particularly in solar hours. India has less than 20 per cent share of electricity in final energy consumption as compared to 29 per cent in China and 27 per cent in South Africa. 500 GW non-fossil capacity targets by 2030 must have been accompanied by mission approach progress on electric mobility, electrification of industrial processes and well-planned growth of electric cooking.Demand flexibility and demand response for increasing solar hour demand can be adopted only through Time of Use tariffs implemented via universal smart metering. We need to accelerate its progress and make it a pre-condition for aggressive target setting for solar additions.Flexibility costs in the power system of India can be kept under control also through a much more diversified growth of RE sources with higher share of wind and hydro. This will reduce the need for new coal based capacities for meeting peak demand in the evening. Taking an easier route of very high solar additions than paying attention to addressing the barriers in expansion of wind and hydro is not likely to work. We should also work harder to integrate hydro projects in neighbouring countries with our system.Lastly, if India, for strategic reasons, wants to take more aggressive solar additions targets, resultant increase in State level system costs should be set off by government capital subsidy or VGF.The writer is former Union Power SecretaryPublished on June 16, 2026