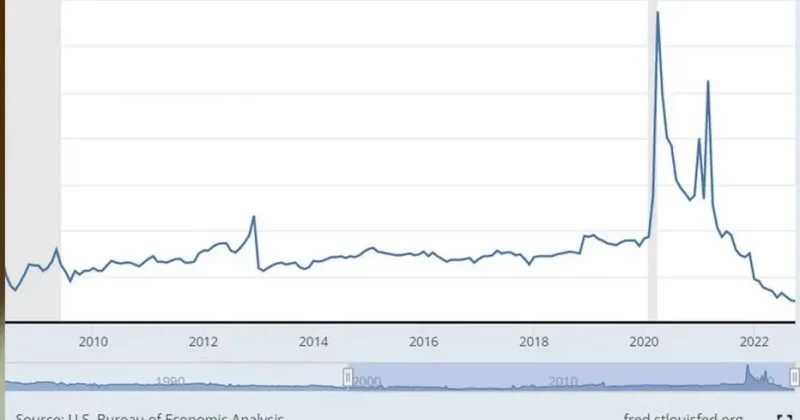

Americans are saving less of their income. The personal savings rate was just 2.6% in April, as reported by the Bureau of Economic Analysis on Thursday morning. That’s down more than half a percentage point from March and down 1.7 percentage points from the start of this year, and marks the lowest rate since June 2022.The reason why, experts said, included inflation remaining strong with gas and grocery prices continuing to rise.“This is really reflective of continued impacts of inflation,” said Ted Rossman, principal analyst at Bankrate. “People are just not saving much at the end of the month.”Ryan Sweet, chief global economist at Oxford Economics, said the low savings rate makes it harder for households to weather a job loss or a costly car repair.“The consumer is essentially running out of that buffer,” he said. “That safety net is starting to get depleted.”In many cases, Sweet said that safety net is gone altogether. That means more household debt.“We start to get concerned that consumers will turn to using credit cards, which we've already seen,” he said.And that could cause people to fall behind on payments, Sweet said. But even as savings dwindle, consumers — especially with higher incomes — have kept on spending. Rossman said that hasn’t always been the case.“Normally, when people are stressed about the economy, they pull back on things,” he said. “They stop traveling, they stop going out to eat.”Rossman said that the fact there hasn’t been a pullback on a wide scale could mean consumers think the current spike in oil prices won’t last.“We keep hearing, from the president and others, that war’s going to be over soon, gas prices are going to come back down,” he said. “I do wonder if some people are pulling more of the short-term lever about, ‘OK, I’ll dip into my savings for now,’ but it’s a short-term adjustment they’re willing to make.”Still, the savings rate is less than half of what it was two years ago. Matt Schulz, chief consumer finance analyst at LendingTree, said that means the trend has been going on for a while now.“I think that struggle is driving more of this right now than confidence is,” he said.Schulz said the best thing consumers can do is to make the most of whatever savings they’re able to pull together.“By using something like an online, high-yield savings account that is getting around 4%,” he said.Compare that to a traditional savings account from a megabank, which Schulz said offers an interest rate closer to zero.

With prices rising, Americans are saving less

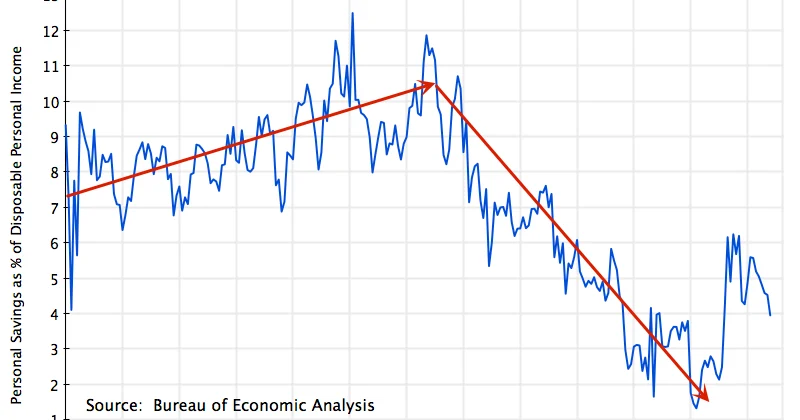

The latest release from the Bureau of Economic Analysis shows the personal saving rate has dropped to its lowest point since June 2022.

TL;DRAI

The US personal savings rate dropped to 2.6% in April — lowest since June 2022 and down 1.7 points since January — as inflation keeps eroding household buffers. Consumers are increasingly turning to credit cards to sustain spending, signaling demand fragility that tech companies with B2C or SMB exposure should factor into H2 forecasts.

419 words~2 min read