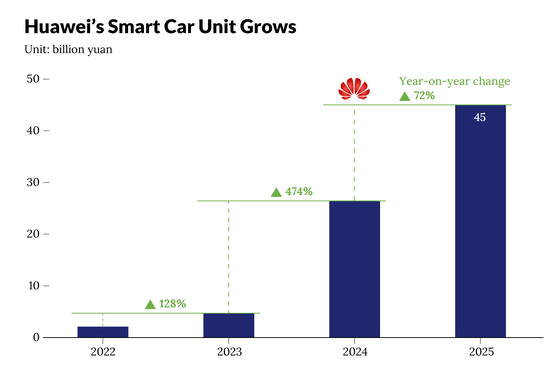

China’s state-owned automakers are significantly strengthening their partnerships with technology leader Huawei Technologies, with a focus on leveraging Huawei’s advanced in-car software solutions. This move signals a crucial shift as these automakers, long cautious about outsourcing core vehicle functions, now face mounting financial pressures and tough competition from nimble private-sector outfits like BYD, Geely, and foreign player Tesla [para. 1][para. 2].Major state-owned players, such as Dongfeng Motor, Guangzhou Automobile Group (GAC), and SAIC Motor, have reported disappointing financial outcomes in 2025. For example, GAC posted a net loss of 2.5 billion yuan ($350.5 million) in the first half of 2025, a remarkable reversal from a 1.5 billion yuan profit a year earlier. Dongfeng’s net profit plummeted 92% year-on-year to just 55 million yuan, while SAIC experienced a 9.2% decline in first-half net profit to 6 billion yuan. Notably, SAIC, once China’s top car seller for almost two decades, lost its crown to BYD in 2024 [para. 3][para. 4][para. 5][para. 6].These poor financial performances are attributed to state automakers’ struggles in the booming new-energy vehicle (NEV) market, now defined by sophisticated, software-driven models. In the first eight months of 2025, NEVs captured 48% of new car sales in China, soaring from only 5.4% in 2020. This surge means NEVs are on track to outsell fossil-fuel vehicles by year-end and easily surpass the government’s 2025 target of a 20% market share for NEVs. The market is also consolidating, with BYD holding a 29.8% share, followed by Geely at 12.8% and SAIC at 8.7% [para. 7][para. 8][para. 9].In response, state-owned companies are aggressively embracing Huawei’s intelligent driving solutions. Recent collaborations include SAIC’s launch of the H5 SUV under the Shangjie brand developed with Huawei’s Harmony Intelligent Mobility Alliance (HIMA), Dongfeng’s integration of Huawei’s systems into its Voyah and M-Hero models, and GAC unveiling a new brand co-developed with Huawei [para. 10][para. 11][para. 12][para. 13][para. 14].Huawei’s technology compensates for state-owned automakers’ lack of in-house expertise in advanced smart vehicle systems, prompting a strategic reliance on the tech firm’s R&D investments. Huawei partners through two main models: HIMA, which gives Huawei influence over design, development, and marketing, and “Huawei Inside,” where automakers deploy entire suites of Huawei’s driving systems without ceding control over vehicle development. Notable brands under these alliances include Seres Group’s Aito, Chery’s Luxeed, SAIC’s Shangjie, and others. However, concerns remain that widespread adoption may lead to less product differentiation for traditional automakers [para. 15][para. 16][para. 17][para. 18][para. 19][para. 20].Mitigating this risk, some companies are diversifying their alliances. For instance, FAW plans to acquire a 35.8% stake in ZYT, an assisted-driving developer recently spun off from DJI, to hedge against over-dependence on Huawei [para. 21][para. 22].Despite increased cooperation with Huawei, privately owned firms continue to outpace state players in developing cutting-edge autonomous driving technologies. Geely’s Zeekr subsidiary recently unveiled a plug-in hybrid SUV with Level 3 autonomous capability—a significant technological milestone. Tesla has expanded its Full Self-Driving system’s rollout in China, and BYD has aggressively promoted its in-house “God’s Eye” driving system across multiple models. Meanwhile, XPeng aims to achieve Level 4 autonomy by late 2025, even as regulatory scrutiny on “autonomous” marketing intensifies following a recent fatal crash [para. 23][para. 24][para. 25][para. 26][para. 27][para. 28][para. 29][para. 30].AI generated, for reference only

In Depth: Desperate for Smart Driving Tech, State Carmakers Turn to Huawei

China’s state-owned auto majors such as Dongfeng and SAIC are overcoming their reluctance to cede control over core vehicle functions as they fall further behind privately owned rivals

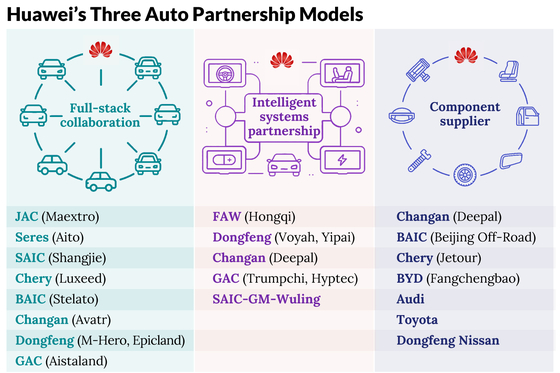

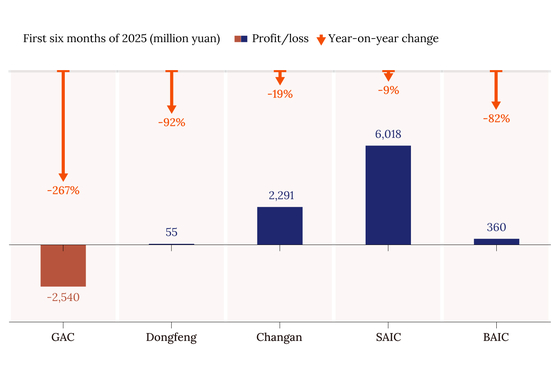

539 words~2 min read