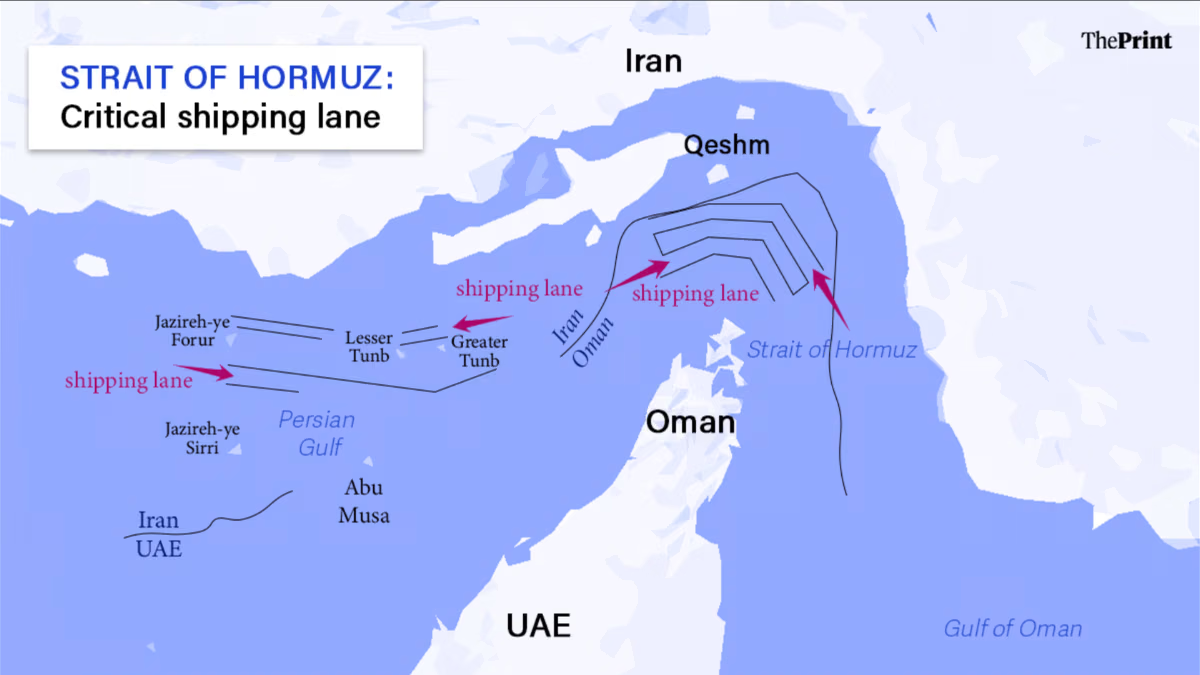

The global oil market is witnessing significant developments as countries are constructing new infrastructure to bypass the Strait of Hormuz, a critical chokepoint currently affected by the ongoing 2026 Iran war. This conflict has effectively closed the strait, which previously handled 17-20 million barrels of oil per day. To mitigate this disruption, nations like Saudi Arabia and the UAE are expediting pipeline projects, such as the UAE’s West-East pipeline, which aims to significantly increase export capacity by 2027. These efforts suggest a strategic shift to reduce reliance on the strait, potentially affecting global oil pricing.

In the context of WTI crude oil futures, market participants appear to be factoring in these infrastructure developments. The pricing for WTI hitting $130 in July remains low, with a current probability of only 1% for such a high price level. However, pricing for a more moderate $90 per barrel has seen increased activity, with a current 33.2% probability, reflecting expectations of moderated price pressures due to these infrastructure expansions.

The situation remains dynamic, with market participants closely monitoring developments around the strait and pipeline projects. The increased probability of achieving $90 WTI in July suggests expectations of a moderate decrease in oil prices, consistent with the broader strategy of bypassing the Strait of Hormuz.