Rio Times Markets · The Week Ahead

Week Overview

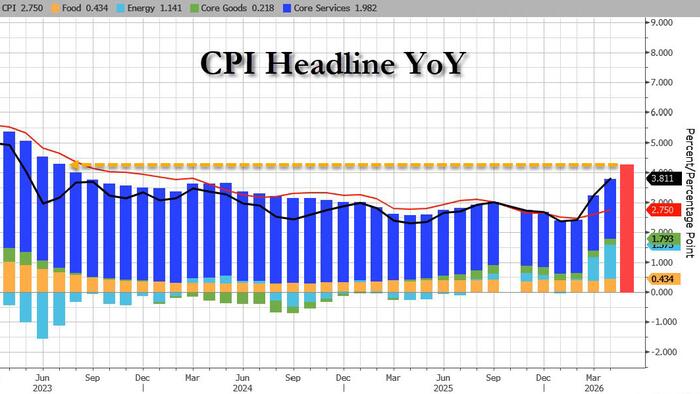

This is the Warsh Fed’s first inflation test. June CPI (Tuesday, 8:30 AM ET, cons. −0.1% MoM / ~3.9% YoY per BMO and Kiplinger) could deliver the first negative monthly headline in over a year — gasoline fell about 10% in June after the Iran peace talks eased Hormuz shipping risk. But as Kiplinger warns, do not let a negative headline fool you: core CPI (cons. 0.3% MoM) stays sticky at 2.9% year-over-year, and the Fed’s newly hawkish dot plot — a median of 3.8% with nine of 18 members projecting hikes by year-end — means Chairman Kevin Warsh is watching core, not the headline.

PPI (Wednesday, cons. 0.0% MoM vs. 1.1% prior) confirms the energy-driven producer deflation, and the Bank of Canada decides the same day (cons. hold 2.25%). The Beige Book (Wednesday, 2:00 PM ET) maps regional conditions in the oil shock’s aftermath, while retail sales (Thursday, cons. +0.3%) and the Philly Fed (cons. 12.1) measure demand.

Abroad, China’s Q2 GDP (Tuesday overnight, cons. +0.9% QoQ) tests the world’s second economy; UK monthly GDP (Thursday, cons. +0.1%) and euro-zone CPI final (Friday, cons. 2.8% YoY) round out the G7. Michigan sentiment (Friday, cons. 51.4 vs. 49.5) could mark the first improvement in five months. Brazil delivers services (Wednesday), retail sales (Thursday) and IBC-Br (Friday); OPEC meets Monday and the Bank of Korea decides overnight Wednesday. There are no major market holidays — normal trading worldwide.