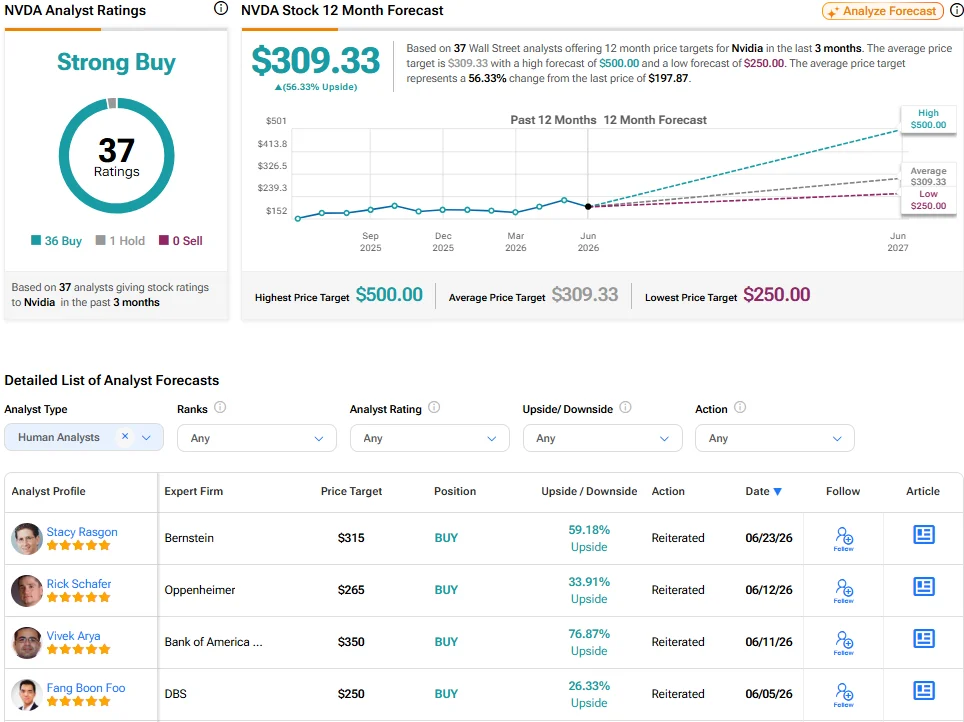

Nvidia’s stock is trading at its cheapest valuation in seven years, and Bank of America thinks that’s a gift. The firm reiterated its Buy rating on NVDA on July 8 with a $350 price target, arguing that the market’s hand-wringing over margins and competition has created a textbook entry point for investors willing to look past short-term noise.

At roughly 18 times forward earnings, Nvidia’s price-to-earnings ratio sits at levels not seen since 2019. For a company that has essentially become the picks-and-shovels supplier to the entire AI gold rush, that kind of discount gets Wall Street’s attention.

The bull case in numbers

BofA analyst Vivek Arya laid out a straightforward thesis. Nvidia’s current stock price reflects what he considers overly negative assumptions about both the company’s earnings trajectory and the competitive threat posed by custom ASICs, the specialized chips that some hyperscalers are developing in-house.

The valuation math is hard to argue with on paper. Nvidia trades at approximately 0.5 times its PEG ratio, with projected average sales growth of 42%. In English: the stock is priced as if the company’s growth engine is sputtering, when the actual revenue trajectory suggests it’s still accelerating.