Nvidia, the company that essentially became the pickaxe seller during the AI gold rush, is now trading at a discount to the broader semiconductor sector. That’s according to Tony Zhang, Chief Strategist at OptionsPlay, who laid out his case on CNBC.

Nvidia’s stock has pulled back toward the $200 level, which technical analysts have flagged as a key support zone.

The valuation case

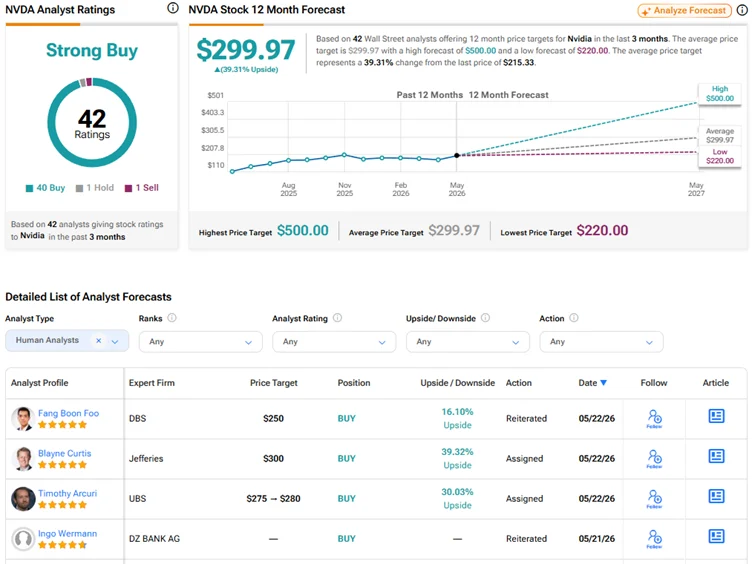

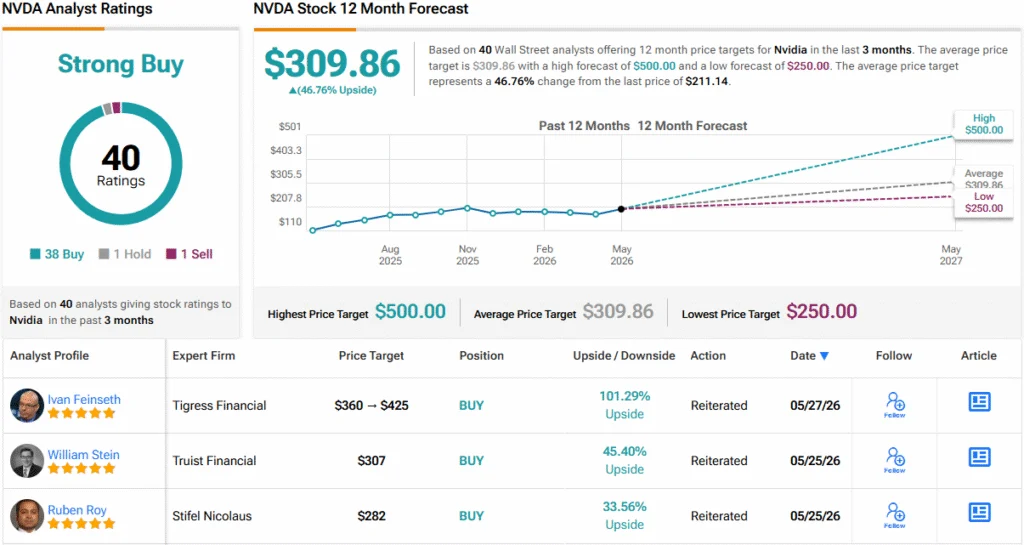

Zhang pointed to Nvidia’s forward price-to-earnings multiples, which currently sit in the range of 22-25 times earnings. In English: for every dollar of future profit Nvidia is expected to generate, investors are paying roughly $22-$25 for the stock. That’s considered favorable when stacked against both industry peers and Nvidia’s own historical averages.

Zhang has historically favored defined-risk options strategies for trading Nvidia. His approach leans toward structures like call spreads and credit spreads, particularly around earnings announcements when implied volatility tends to spike. The logic is straightforward: capture upside exposure while capping potential losses.