A student in one of my courses recently elected to switch from a standard letter grade to a pass-fail option, under a Bowdoin College policy that allows students to take up to four of their courses on a “credit/D/fail” basis. She wasn’t struggling in the class—far from it. She made the change because she had been earning an A-minus.

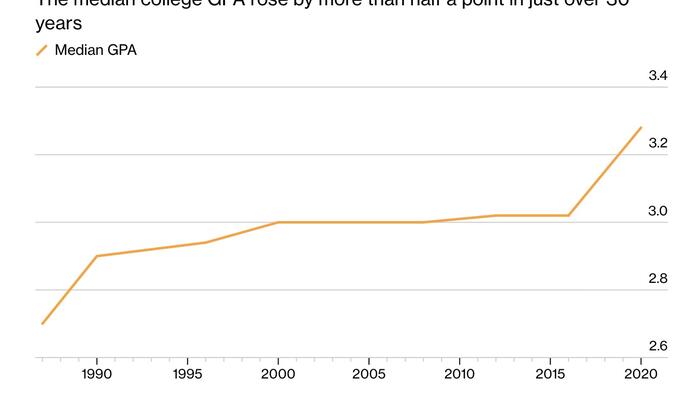

The recent decision by Harvard University to cap the percentage of A’s awarded has renewed conversations about grade inflation in higher ed. As an economist, I can observe that grade inflation shares some characteristics with price inflation.

Effective grading and pricing mechanisms both signal relative values, and the signal degrades when persistent increases alter those relative valuations. If every single agent in every economy raised prices by 10 percent, relative prices would remain unchanged and the negative impact of this monetary rescaling would be minimal. Similarly, if (starting from a moderate base) every single professor in every educational institution in every country simultaneously increased the proportion of A’s by 10 percent, the result would not be so concerning. However, if I do not follow the inflated distribution of my colleagues, my students would suffer from the variation in relative prices.