Why did the Japanese yen hit its weakest level since 1986, and what does this mean for global financial markets? Explore the implications of Japan's new monetary policy strategy.

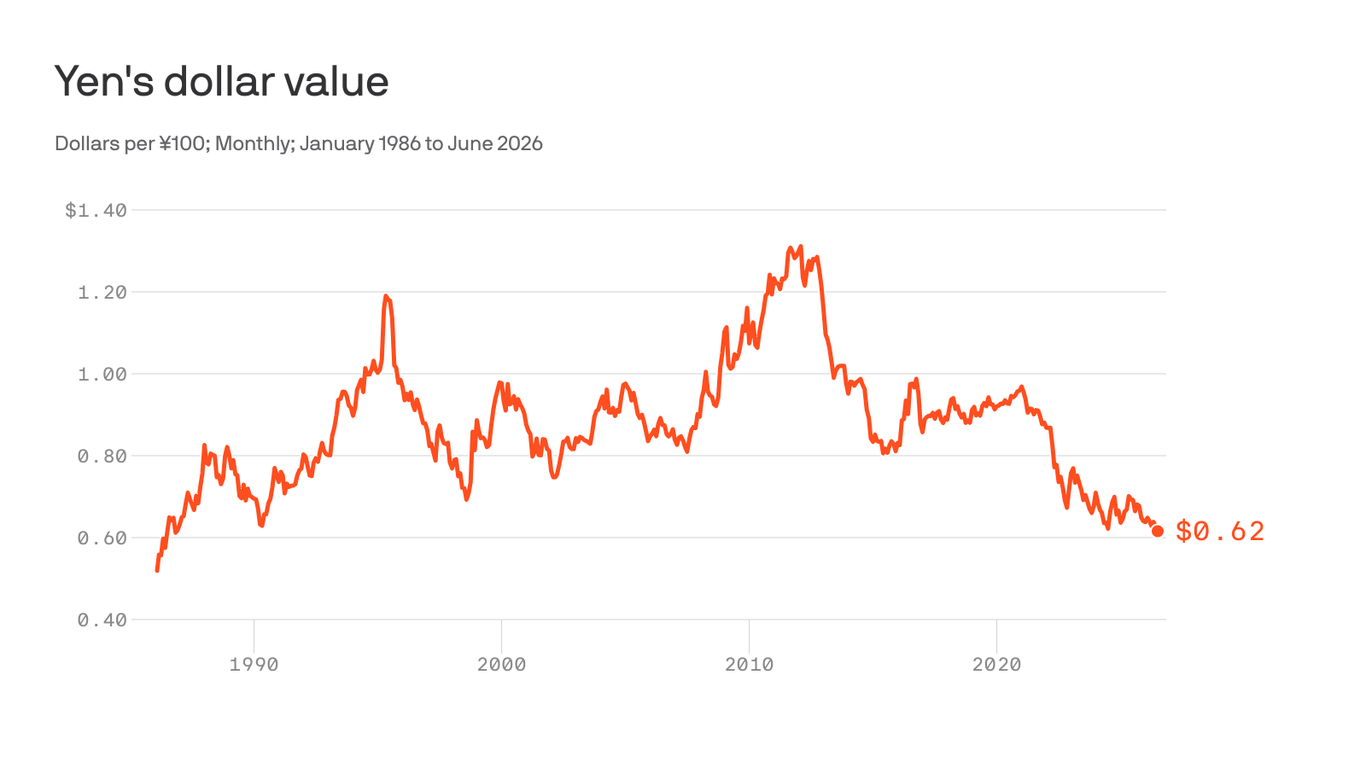

Last week, the Japanese yen hit ¥162.66/$, its weakest level since 1986.

The last time the rate was at this level, Japan was deep inside the asset bubble that would erase a generation of wealth. That context matters, because it is the insight which is informing the Japan’s Ministry of Finance’s (MoF’s) decisions and it explains why Japan’s monetary policy playbook has changed.

Japan has abandoned its practice of telegraphing (communicating) intervention. The old approach was transparent enough that the market had learned to trade around it. Officials would issue warnings, traders would gauge proximity to a threshold and position accordingly, the MoF would step in, the yen would recover briefly and the carry trade (where investors borrow currencies with low interest rates and use those funds to invest in currencies with higher interest rates) would rebuild once the pressure eased.

Japan spent a record ¥11.7 trillion, roughly $72 billion, in a single April to May 2026 intervention window. The yen bounced and fell straight back through the level they had defended.