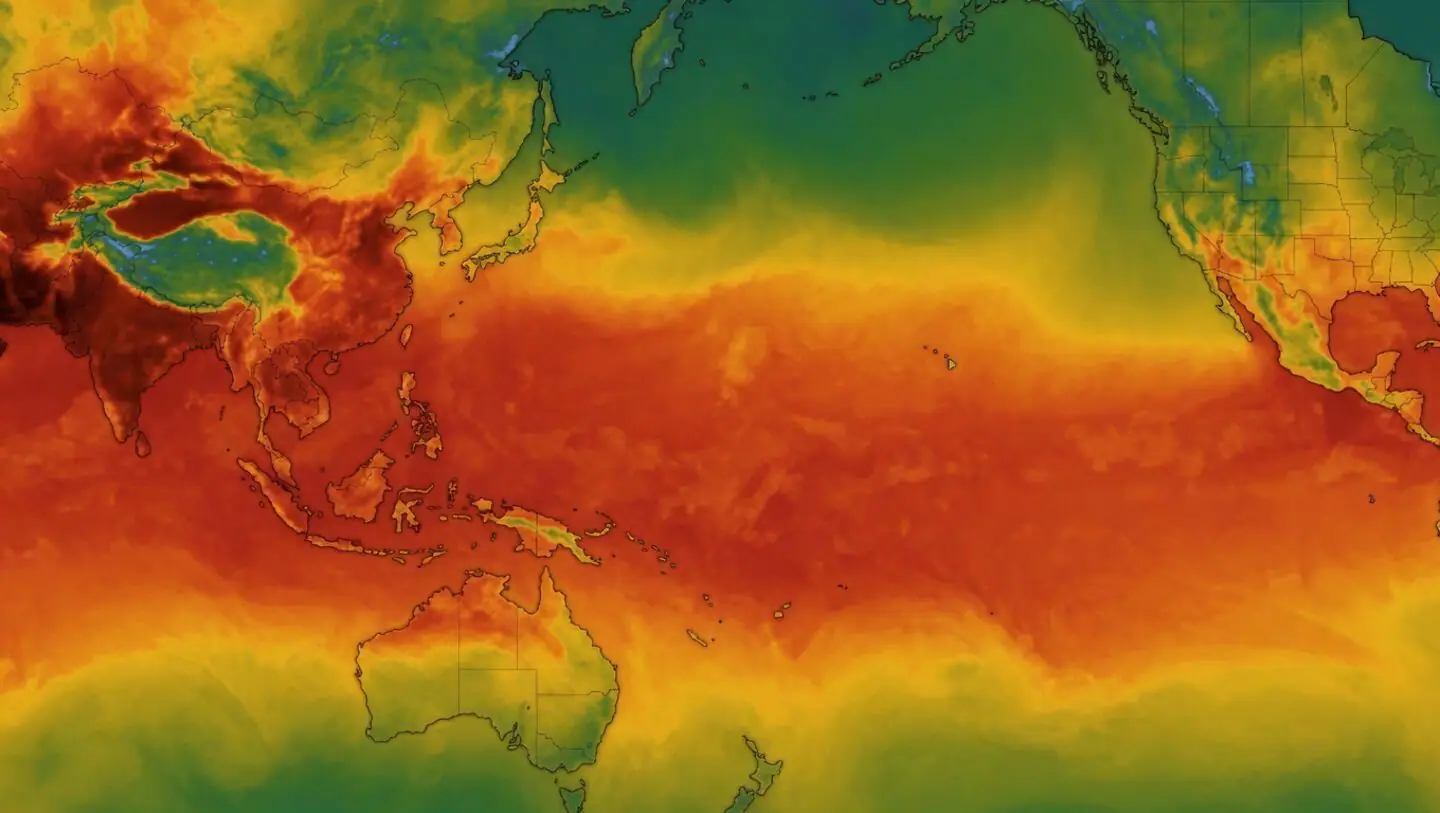

Come May, one event that is most-awaited and tracked by India Inc and investors is the onset of the South-West monsoon and its progression.The 2026 South-West monsoon season has opened on a weak note, with the country recording a 40 per cent deficient rainfall in June. However, the IMD expects monsoon to progress, beginning this week.One word that is frequently making the headlines is El Nino. And with several global weather agencies having confirmed the event, the fear seems real now. But is El Nino something investors should really worry about?For those who are unfamiliar with the Spanish word, it basically denotes the adverse changes (rapid increase) in the sea-surface temperature (SST) over central and eastern Pacific region. This affects the trade wind formation and movement, eventually resulting in below-normal rainfall in Australia and South-East Asian regions such as Indonesia and also has an impact on India’s monsoon rainfall.But an El Nino event does not necessarily spell doom. Much depends on its timing. If conditions intensify only after September, the impact on India is likely to be limited, as the South-West monsoon accounts for nearly two-thirds of the country’s annual rainfall.The intensity of the El Nino event is very crucial. The Nino 3.4 Index, in addition to trade winds, atmospheric response and sub-surface ocean temperatures, is the basis for ascertaining the event. If the SST value is above 0.5 for five consecutive three-month overlapping seasons, then it’s a weak El Nino. An SST value between 0.5 and 1.5 implies a moderate El Nino; while any value above 1.5 indicates a stronger event.We have had two El Nino episodes in the last three decades — 2015 and 2023. But in 2015, which is considered moderate El Nino, the overall rainfall deficit was 12.7 of the Long period Average (LPA). Interestingly, in 2009, which was a drought year, the SST values during the season were under 0.5, indicating a no El Nino year. Likewise, 2014, too, was not an El Nino year.It is clear that El Nino is not the only reason for a poor monsoon. Indian Ocean Dipole (IOD) is a climate phenomenon caused by variations in sea temperatures in the Indian Ocean. Its positive, negative and neutral phases can influence the Indian monsoon. A positive IOD brings good rainfall to India, while a negative IOD results in lower seasonal rainfall.Other factors include Madden Julien Oscillation (MJO), more of a short-term phenomenon lasting for about 60 days, unlike an IOD or El Nino, which last for several months.What is the current status of El Nino, IOD and MJO, and what are the implications for our South-West monsoon season?As per SST data published by the IMD, the SST value was -0.1 for the March-May period, which is an increase from -0.9 in the December-February period. However, as per the latest data released by Columbia Climate school, the SST anomaly measured using Nino 3.4 Index, which was at 0.48 degree Celsius in March-May period, has increased swiftly to 0.94 degree Celsius by May and further increased to 1.7 by June 17. This indicates a strong possibility of a moderate-to-severe El Nino event this season. Multiple agencies, including National Oceanic and Atmospheric Administration, have confirmed the El Nino event.The IOD, which was positive to neutral at the start of the year, is now showing a swing towards negative zone — with the May IOD at -0.39 in the IMD website. MJO is possibly not presenting clear indications yet.However, the IMD has indicated widespread rainfall this week, supported by formation of a ‘low’. While the rainfall progress in July remains extremely crucial, the Indian government has launched an emergency plan to protect crops in 315 districts with irrigation infrastructure gaps and significant deficiency in rainfall and the farming community is preparing itself for the worst. The government is helping the farming community to navigate this phase by shifting to crops, such as millets and pulses, which can thrive on less water, use of climate-resistant and short-duration crops, etc.Efforts such as these can help minimise the impact of weak rainfall on farm incomes, as foodgrain production bears the biggest brunt of a weak-rainfall season. Directionally, the impact is visible, either through flattish output or a marginal decline in output during the years when the monsoon has been below normal. For instance, in 2009-10, which followed the 2009 drought year, foodgrain production slipped 7 per cent. In the following years — 2014 and 2015 — production was lower by 4.9 per cent and 0.2 per cent, respectively. Similarly, in 2019, when the rainfall was a tad lower, the growth in foodgrain production was flat. As foodgrain production is highly sensitive to monsoon rainfall, this needs to be closely monitored. Meaningful improvement in rainfall will be crucial to keeping food inflation under check.Levels of farm income and food inflation are two important variables that have a bearing on economy and interest rates and thereby on the markets.However, India has, over the last three decades, managed to increase the area under irrigation — from 33.6 per cent in 1990-91 to 39 per cent by 2001 and 59 per cent by 2023, is worth noting. States such as Punjab and Tamil Nadu have seen significant improvement in the irrigation penetration, while Maharashtra continues to be significantly dependent on the monsoon, making it more vulnerable, given that the State is a key producer of sugarcane and cotton.Sectors that need to be watchedWhile conventional wisdom suggests that agri and allied sectors may be the first casualty of a weak monsoon, what does historical data point to?Contrary to our conventional wisdom that monsoon weakness may have a direct and significant impact on the sales of agri-inputs, historical data show resilience. For instance, when we study the trend in fertilizer sales, it has remained strong even during weak monsoon years. For instance, during the drought year of 2009, fertilizer consumption grew 6.4 per cent year-on-year. Similarly, in 2014 and 2015, when the rainfall was lower than the LPA by 12 per cent and 14 per cent, respectively, fertilizer sales grew 4.5 per cent and 4.3 per cent, respectively. This is largely because of two reasons. First, the purchases typically happen ahead of the season and hence remain unaffected by the rainfall. Second, the high government subsidy on urea and complex fertilizers has also supported consumption. Stocks such as Chambal Fertilisers and Chemicals, and Coromandel International have delivered healthy gains irrespective of the monsoon concerns and stocks are up 9-10x in the last 12 years.Interestingly, the sector has seen significant improvement in profitability over the last decade, thanks to the initiatives to bring in operational efficiencies. This aside, government efforts such as direct benefit transfer for subsidy and timely payment of subsidies, have helped improve the sector’s balance sheet.Chambal Fertilisers, a leading producer of urea, for which the subsidy continues to account for a significant portion of the total realisation, has seen its debtor-days reduce from 100+ levels in FY15 to less than a week in FY24 and FY25, although it has increased to about a month in 2026. For Coromandel International, among the country’s largest complex fertilizer players, debtor-days halved from over 40 days in FY15 to about 20 days by FY24. However, FY26 has seen an increase in the debtor-days.Even as the broader demand is expected to remain steady in 2026-27, the significant jump in input costs for the sector due to the US-Iran war could result in an increase in the working capital needs for companies and impact profitability. The reason: Even though the government continues to shoulder the burden of higher input costs through subsidy, payment can be back-ended as the subsidy for complex fertilizers were announced ahead of the crude rally.Sulphur, a crude derivative used to make phosphoric acid, which in turn is used in complex fertilizers, has risen from $350 per tonne in 2025 to almost $850 per tonne in 2026. The cost of anhydrous ammonia has also increased from $500 a tonne last year to over $750 this year. Gas prices globally witnessed sharp rise in 2026 due to the war.Agrochemicals has traditionally seen some correlation to monsoon rainfall. This is because, unlike fertilizers, only the purchase of preventive sprays happen ahead of the monsoon. For instance, in 2014 and 2015, when the country saw two consecutive years of deficient rainfall, the overall industry witnessed growth stagnation at about ₹20,000 crore. However, they staged strong recovery post 2015. For an industry that was reeling under pressure due to global de-stocking and price-cuts driven by China since 2023, the de-stocking completion came as a hope. However, the input price hike due to the US-Iran war may play spoilsport in the short term.Besides impact on the sectors that are directly connected with agriculture, a weak monsoon may have a cascading effect on other sectors, too, like FMCG companies.BeneficiariesHowever, there are some sectors that cheer a weak monsoon. Construction and building materials sectors, for instance, always share an inverse relationship with the South-West monsoon. A poor monsoon rainfall means uninterrupted construction activity and consequently, there is stronger demand for materials such as cement, steel, paints, etc. Cement dispatch, for instance, grew at a healthy 8 per cent plus in 2009, even as the country was grappling with drought. While the sector’s prospects are more closely aligned with the overall economic activity, uninterrupted construction during monsoon can boost sales.Mining is another industry which benefits from a weak monsoon season. Traditionally, mining activity remains lull during monsoon and in the absence of rainfall, mining continues to remain steady, thereby helping companies in this space achieve higher revenue and earnings.Power generation – coal and also solar – which could be disrupted during the monsoon season, may see higher output, should rainfall not pan out as expected.Farm incomeSectors riding the rural consumption wave may see an indirect impact from weak monsoon rainfall. Two-wheeler producers and farm equipment makers have traditionally seen tepid sales in years of lower agricultural output. For instance, M&M saw its revenue and operating profit decline 3 per cent and 13 per cent, respectively in FY15.Another sector that has had a reversal of fortunes over the past decade is FMCG. Within the FMCG universe, the fortunes of the companies that get a significant share of revenues from the rural market, share a strong correlation with the monsoon rainfalls, with a lag effect though. Sample this: Hindustan Unilever’s revenue and operating profit declined 13 per cent and 4 per cent respectively, in FY10, following the drought in 2009. In 2014-15, after two consecutive weak monsoons, the company reported flat revenues and a 4 per cent operating profit decline in FY16.P&G Hygiene and Healthcare saw the weakness continue until 2017 at the revenue level, even as its operating profit margin witnessed improvement during this period. Dabur and Marico also saw their revenue growth stagnate in the FY15-17 period. The stagnation in revenue and profit happened with a two-year lag in FY17-18 after weak monsoons for five consecutive years. The FMCG sector, measured by the Nifty FMCG Index, also mirrored the weak growth of the companies in this space, declining 13 per cent and 5 per cent in 2002 and 2004, and a flat performance in 2015.Initiatives such as crop rotation and planting of crops that can be managed with limited water can only help partially mitigate the impact of weak monsoon on rural income.Monsoon and inflationThe effect of a weak monsoon on the food and beverage (F&B) consumer price inflation (CPI) is evident, though with a one-year lag. For instance, after two consecutive weak monsoon phases in 2014 and 2015, monthly CPI on F&B remained elevated at over 5 per cent during 2015-16.Likewise, after the weak 2023 monsoon, the F&B monthly CPI shot up to a new high of over 10 per cent in 2024 and remained high until 2025.Another important agricultural product to be monitored is sugar. A sharp spike in sugar can have a cascading effect on packaged foods, FMCG, beverages, etc and can also have a rub-off impact on inflation. The implications are significant with India contemplating curbs on sugar exports in order to meet the country’s energy needs, given the focus on ethanol blending programme (EBP), especially due to the spurt in crude oil prices. With sugarcane diversion to ethanol expected to increase, any reduction in cane acreage or yield can risk not only the country’s domestic sugar availability, but its ambitious EBP too. Cane acreage and yield are important variables to track.Monsoon and marketIndia’s equity indices have historically remained unaffected by the monsoon vagaries. Key benchmark Nifty 50 Index’s performance over the weak monsoon phases such as 2004, 2009 and 2023 has remained strong and resilient. Except for calendar year 2015, when the Nifty 50 index corrected about 4 per cent, the benchmark index had actually delivered positive returns during the earlier periods of weak monsoon such as 2002 (3.6 per cent), 2004 (9 per cent), 2009 (71 per cent) and 2023 (30 per cent). Index composition, with significant weightage for banks, financial services, IT services, oil & gas, and metals, is also possibly the key reason behind the resilience. However, the stellar rally in 2009 was after the mayhem in 2008, following the global financial crisis.Overall, history indicates the impact of El Nino weak monsoon on markets is not broad-based and only affects few sectors. At the same time, there are a few risks now which are different from the past. The impact of inflation arising from reduction in agri produce and the risk to consumption due to fall in rural incomes, can add to the pressure on an already volatile market grappling for positive news.Even though historical data do not point to any serious risks from a weak monsoon as a standalone factor, the current geopolitical situation and crude price volatility and the weakening of Indian rupee against the US dollar need to be tracked by investors from here. One cannot rule out the possibility of a knee-jerk reaction in the market should the rainfall situation continue to remain weak without any significant meaningful improvement in July and August.Published on July 4, 2026

Clouded under El Nino skies

Explore the implications of the El Nino event on India's agriculture, markets, and economy amid a weak monsoon season.

2,346 words~11 min read