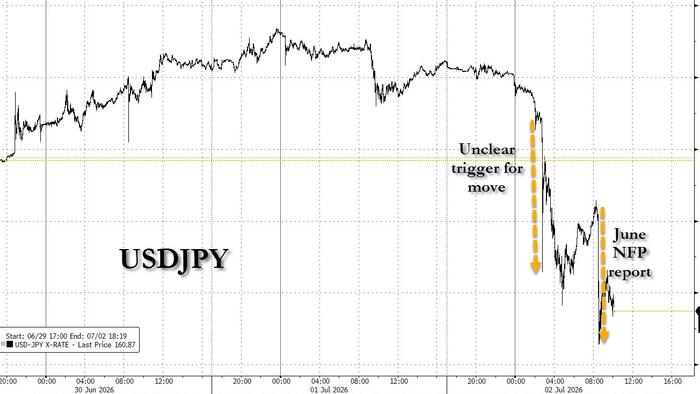

The Japanese yen is having a rough year, and options traders are bracing for it to get rougher. With USD/JPY trading near 162.38, the yen’s weakest level against the dollar since 1986, demand for volatility hedges is spiking as the July 4 US holiday approaches and trading desks empty out.

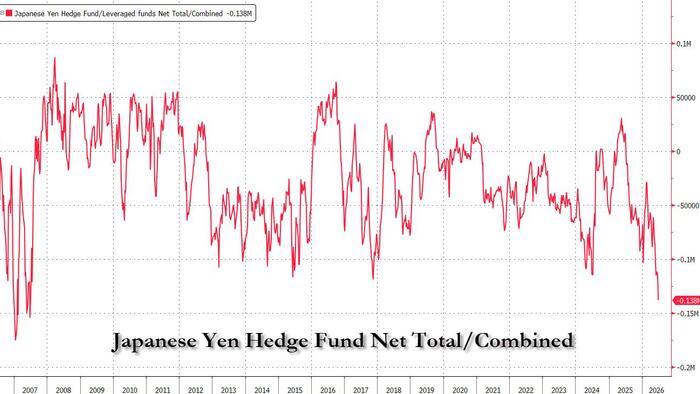

The yen’s slide has been driven by interest rate differentials. The Federal Reserve’s hawkish posture has kept the dollar attractive relative to the yen, which remains anchored by Japan’s comparatively accommodative monetary policy. The result is a one-way trade that has pushed yen short positions in futures markets to record highs.

Japanese authorities spent roughly ¥11.7 trillion, approximately $73.6 billion, on currency interventions from April to May 2026. Past interventions from the Bank of Japan and MOF have tended to act as temporary stabilizers rather than trend reversals. Traders know this, which is why the yen keeps weakening even after massive intervention campaigns. But the interventions still cause violent short-term moves, and if you’re positioned wrong when one hits, the damage is real.

Options markets are reflecting this anxiety. Traders are paying elevated premiums for contracts that protect against sharp yen moves in either direction, with particular focus on the period around July 4 when US markets close early and liquidity drops.