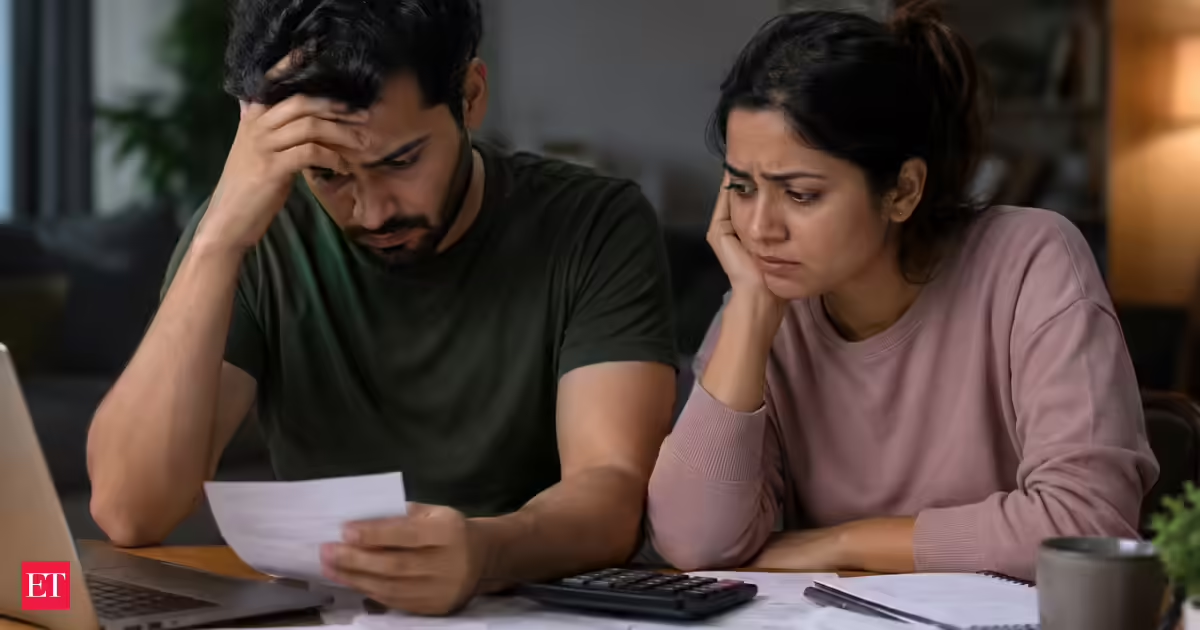

If you look closely at India’s macroeconomic indicators — such as the growth rate, inflation numbers, etc., — they project a story of robust financial discipline and economic growth. However, the average household budget portrays a far more fragile reality. Over the last 12 years, the vital link between the wealth created by the economy and individual purchasing power — the goods and services one can buy with one’s income — has broken.Given wages (after inflationary erosion is accounted for) have not grown across livelihoods, households have been forced to meet consumption expenses through borrowings. (Photo for representation) (Pexel)Given wages (after inflationary erosion is accounted for) have not grown across livelihoods, households have been forced to meet consumption expenses through borrowings. Families are now increasingly relying on credit card debt, personal loans, and loans raised against gold to fill the gap between growing expenses and stagnant incomes. This underlines a wage-debt squeeze — and borrowings must be repaid from the same, constrained incomes — that is forcing the working class to walk a precarious financial tightrope.The growing financial strain on the Indian working class cannot be dismissed merely as a temporary external price shock — resulting from, say, the energy supply disruptions because of the war in West Asia. Rather, it is a realignment in how national wealth is generated and distributed. While the economy has seen a sustained phase of growth and stock-market indices have risen alongside, the mechanism through which the national wealth generated is transmitted to households has broken down.Also read: Terms of Trade | A fine imbalanceWhen such a structural wage gap is sustained over a long period, it inevitably shifts the macroeconomy. This lack of income growth and the consequent pressure on households directly explains the fall in India’s net household financial savings, to a historical low of 5.2% of gross national disposable income (GNDI) in FY23, from its long-standing average of 7-8%. Loans raised against collaterals or secured loans, on the other hand, have doubled from 3% of GDP in FY14 to 5.7% by FY23, resulting in the combined household debt — outstanding secured and unsecured loans — breaching 40% of the GDP by end of 2023. Long-term economic data reveals a “K-shaped divergence”, evidence that India’s economic recovery post the Covid-19 pandemic has been driven by corporate profits rather than proportional growth in wages.Also read: Who is ‘Honourable’ in the Indian republic? High Court order sparks a questionAcross organised sectors, non-managerial corporate compensations — as a share of total company expenditure — have seen a gradual decline. Additionally, year-on-year wage growth in heavy infrastructure and manufacturing has languished below the real rate of inflation in the last five years. This squeeze is not an isolated urban phenomenon. While the minimum support prices (MSPs) have been regularly increased, the gains have flowed in a skewed manner.Asset-owning landholders have cornered the largest share of these increases, completely ignoring the landless casual labourers who rely on daily cash wages, which have not grown in keeping with MSP increases.Also read: Climate action needs cash. Where is it?Real wages for casual labourers have languished at an annualised growth rate of under 1.5% between 2014 and 2025. The impact of this wage suppression has been worsened by the lack of stable employment opportunities in formal, urban settings. Since 2018-19, there has been a massive reverse migration, with millions of workers returning to agriculture from precarious non-farm employment. This glut of labour has eroded bargaining power in negotiating a fair baseline compensation.When an economy systematically substitutes wage growth with credit access, the fundamental nature of consumer debt also changes. The big worry for India is not merely household debt, but also its survivalist composition — that people have become dependent on it to meet even essential expenditures. Domestic borrowing has pivoted away from secured lending such as housing mortgages toward short-term, unsecured liabilities. The Reserve Bank of India (RBI)’s Financial Stability Reports note that unsecured personal loans and consumer retail credit have registered compounding annualised growth rates of 22-25% in recent years. Outstanding credit card debt and loans against gold jewellery — traditionally, borrowers’ last resort — have surged; gold loans alone have reached ₹3.38 lakh crore, registering a massive 128.5% year-on-year growth. This localised credit explosion is concentrated specifically within the lower-income brackets facing the sharpest real-wage stagnation.TransUnion CIBIL report reveals that small-ticket loans (under ₹50,000) have seen the most explosive growth, driven by digital lending apps and microfinance institutions targeting distress-borrowers.By utilising short-term but expensive debt to fund immediate survival, the working class effectively borrows from its future financial security to keep current domestic consumption afloat. Debt-led consumption provides a temporary illusion of stable demand, but it does so by compromising long-term solvency of the Indian household.The stabilisation of the macro-indicators has occurred at the cost of financial strength of working-class households. Unsecured retail debt growth cannot permanently replace income growth, nor can small-ticket micro-loans act as a lasting surrogate for a stable social safety net. When household financial liabilities double as real agricultural wages grow at less than 1% per annum, it means that the economy is running on borrowed time.To transition from a fragmented, highly unequal growth trajectory to an inclusive and sustainable model, India’s policy should pivot away from pure supply-side incentives. While measures like corporate tax cuts and manufacturing incentives have boosted industrial capacity, they have failed to trigger higher wages for the workforce. The government must rationalise GST slabs on non-discretionary consumer goods and essential services to immediate lower bands. The fiscal framework must additionally rely more on progressive direct taxation rather than burdening the working class. Revitalisation of the labour-intensive MSME ecosystem can further this initiative so that informal workers can be transitioned through formal contracts, raising the national wage floor. Finally, there needs to be a robust scaling up of public budgetary allocations for health care and education. When the Union government absorbs the financial risk of heath and education experienced differentially by states at the moment, it immediately frees up a higher proportion of household disposable income for discretionary consumption, breaking the cycle of survivalist borrowing.Deepanshu Mohan is dean and professor of economics at OP Jindal Global University (JGU) and a visiting professor at LSE and University of Oxford. Srisoniya Subramoniam is a researcher with Centre for New Economics Studies, JGU. The views expressed are personal

Borrowing to survive, as wages fail to rise; India's working class walks a financial tightrope

The growing financial strain on the Indian working class cannot be dismissed merely as a temporary external price shock.

1,056 words~5 min read