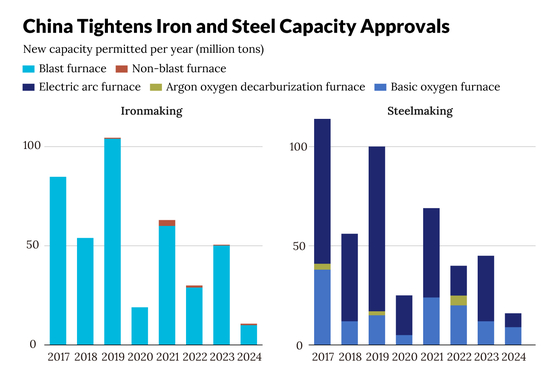

1. China's Ministry of Industry and Information Technology has released new rules on replacing steel production capacity, ending a nearly two-year suspension of new approvals and representing the most significant overhaul of the policy since 2021 [para. 1]. Since 2014, national steel policy has aimed to control overall capacity and encourage upgrades by requiring older capacity to be retired before new facilities can be built [para. 2]. The revised measures, announced on May 18, require even more capacity to be retired before new capacity is added, tighten eligibility requirements, and place new restrictions on the use of dormant capacity [para. 3]. These changes come at a pivotal moment for China's steel industry, which faces slower demand growth, weak profitability, and mounting pressure to reduce emissions—steelmaking remains responsible for about 16% of national carbon emissions [para. 4][para. 5].2. China's capacity replacement policy has evolved over the past decade from a mechanism to manage industrial capacity into a broader tool supporting industrial upgrade, environmental improvement, and decarbonization [para. 7]. The first rules in 2014 required 1.25 tons of existing capacity to be retired for every 1 ton added in key air-pollution control regions, and 1:1 elsewhere [para. 9]. The 2017 revision introduced preferential treatment for electric arc furnace (EAF) steelmaking, which is less polluting and less carbon-intensive than the dominant blast furnace-basic oxygen furnace (BF-BOF) route [para. 10]. Following China's 2020 carbon pledge, the 2021 revision incorporated more explicit climate objectives, tightened replacement requirements, and added stronger support for EAF and emerging low-carbon technologies [para. 11]. The latest 2026 revision generally requires 1.5 tons of existing capacity retired per ton added, excludes long-idled capacity from replacement calculations, restricts cross-regional and cross-company quota trading, and provides more explicit support for EAF and hydrogen-based steelmaking [para. 12].3. Between 2017 and 2024, approved replacement plans included about 400 million tons of new blast furnace capacity, 318 million tons of new BOF capacity, and 128 million tons of new EAF capacity, with BF-BOF projects continuing to dominate despite an increasing share of EAF projects over time [para. 14]. Approval volumes declined significantly after peaking in 2017-2019 due to weaker demand and tighter controls, and the suspension of new approvals in August 2024 further reduced volumes [para. 15]. Following China's carbon pledges, EAF projects accounted for a growing share of approved steelmaking capacity, and a small number of hydrogen-based technologies began to emerge, yet the policy's contribution to decarbonization remained more limited than its role in modernizing production assets [para. 16][para. 17].4. The policy's impact on decarbonization was constrained because most new capacity continued to rely on the coal-based BF-BOF route, even though newer facilities are more energy efficient [para. 18][para. 19]. Additionally, some replacement projects retired underused or idle facilities while newer plants were more productive, meaning nominal capacity reductions did not always lead to lower production or emissions [para. 20]. Competing priorities among stakeholders—the central government focused on pollution control and decarbonization, local governments on investment and employment, and steel companies on competitiveness—meant that capacity replacement proved more effective at modernizing facilities than driving structural decarbonization [para. 21][para. 22].5. The 2026 revision reflects lessons from a decade of policy implementation and the changing realities of China's steel industry, which is entering a period of weakening demand, thin margins, and rising trade frictions [para. 24][para. 25]. One priority was improving the credibility of capacity reduction by raising the standard replacement ratio to 1:1.5 and excluding long-idled facilities [para. 27]. The revised framework also tightens restrictions on buying and selling retirement quotas to prevent them from becoming detached from actual production activity [para. 28]. Additionally, the policy provides more explicit support for hydrogen-based steelmaking, reflecting recent industrial experience with large-scale projects like those led by Baowu and HBIS [para. 29]. However, nearly a month after the revised rules came into effect, no entirely new capacity replacement plans have been announced, and new project activity remains limited [para. 31][para. 32].6. The revised framework could help create more favorable conditions for steel decarbonization by making it harder for high-carbon capacity to remain in the system and sending a clearer signal for future investment in low-carbon technologies [para. 34][para. 35]. However, capacity policy alone is unlikely to drive a rapid transition due to weak demand, low profitability, and the higher cost of low-carbon technologies compared to conventional options [para. 36]. EAF steel's share of crude steel production has remained around 10% in recent years, well below the 15% target set for 2025 [para. 37]. Ultimately, capacity replacement is likely to play a supporting rather than decisive role, with the expansion of China's national carbon market, development of green steel standards, and efforts to green industrial supply chains proving equally important in creating demand for green steel [para. 39][para. 40]. The 2026 reforms are best understood as part of a broader shift, as research estimates that about 350 million tons of blast furnace capacity may need to be retired by 2030 to support the sector's decarbonization pathway [para. 42].AI generated, for reference only

China’s New Steel Rules Test Limits of Industrial Decarbonization

Policy update aims to force older plants out of commission and accelerate low-carbon investment, but weak demand and coal-heavy production continue to constrain progress

832 words~4 min read