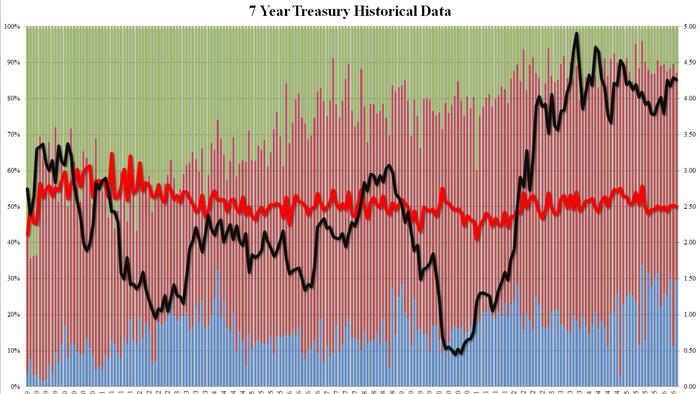

The US Treasury just auctioned off its latest batch of 7-year notes, and the results tell a story about who still wants to lend money to Uncle Sam. The high yield came in at 4.290%, with a bid-to-cover ratio of 2.5 that suggests adequate but hardly enthusiastic demand.

Direct bidders, which include domestic institutions and primary dealers, increased their share of the auction. Meanwhile, indirect bidders, a category that typically captures foreign central banks and international investment funds, pulled back.

What the numbers actually mean

A 4.290% high yield on a 7-year note means the US government is paying investors roughly $4.29 per year for every $100 they lend, over a seven-year horizon. That’s a meaningful cost of borrowing for intermediate-term debt, and it serves as a benchmark that ripples through everything from mortgage rates to corporate bond pricing.

The bid-to-cover ratio of 2.5 means that for every dollar of notes the Treasury was selling, investors collectively offered to buy $2.50 worth. A bid-to-cover ratio below 2.0 would start raising eyebrows about weak demand. Anything above 2.5 to 3.0 typically signals strong appetite. This one lands squarely in the “fine, nothing to see here” zone.