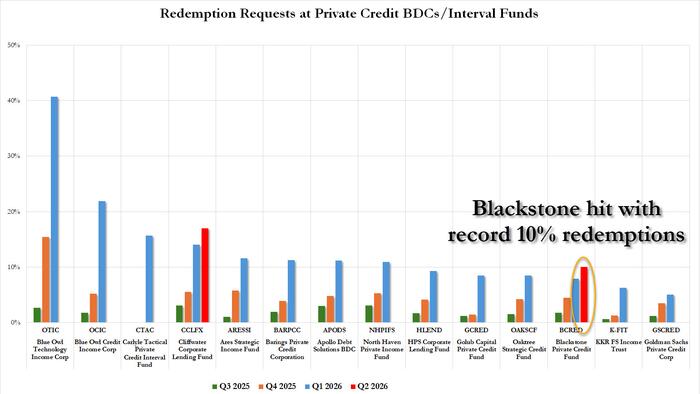

When roughly one in ten investors wants out of your fund at the same time, you have a problem. When you can only let half of them leave, you have a headline.

Morgan Stanley Investment Management capped redemptions in its North Haven Private Income Fund at 5% of outstanding units during Q1 2026, even though investors submitted requests totaling approximately 10.9% of shares. The math is unforgiving: the firm honored only about 45.8% of the exit requests, paying out roughly $169 million while leaving hundreds of millions in withdrawal demand unfulfilled.

A semi-liquid fund meets fully real panic

The North Haven Private Income Fund manages somewhere between $7.6 billion and $8 billion in assets, making it one of the larger specialty finance vehicles focused on middle-market lending. It has generated an annualized yield in the range of 8.5% to 9.25% as of May 2026. The problem is that yield means nothing if you can’t access your capital when you want it.

The 5% quarterly cap on tender offers isn’t something Morgan Stanley invented on the fly. It’s a pre-established structural feature that complies with SEC rules governing semi-liquid private credit funds.