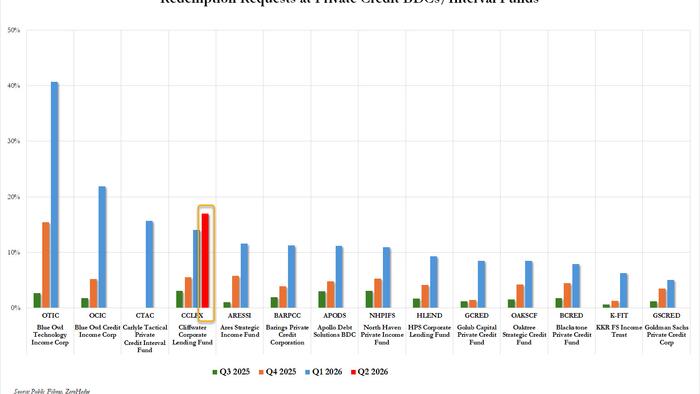

When investors in a $31 billion fund want out and the fund says “not so fast,” it tends to get people’s attention. Cliffwater Corporate Lending Fund, one of the largest private credit interval funds in existence, has capped its quarterly share repurchases at 5% of net asset value despite receiving redemption requests totaling roughly 17%.

That means for every dollar investors wanted back, the fund is returning less than 30 cents. The rest stays locked up.

A liquidity squeeze months in the making

This isn’t the first sign of stress. Back in the first quarter of 2026, approximately 14% of the fund’s shares were tendered for repurchase. Cliffwater responded by executing the maximum allowable buyback of 7%, distributed on a pro-rata basis. In plain English: everyone who wanted out got a partial exit, proportional to what they requested, but nobody got the full amount.

Now redemption demand has climbed even higher, to 17%. And the fund has tightened the gate further, setting repurchases at exactly 5% of its $31.53 billion NAV, roughly $1.58 billion. Payments for this round are scheduled for June 5, 2026.