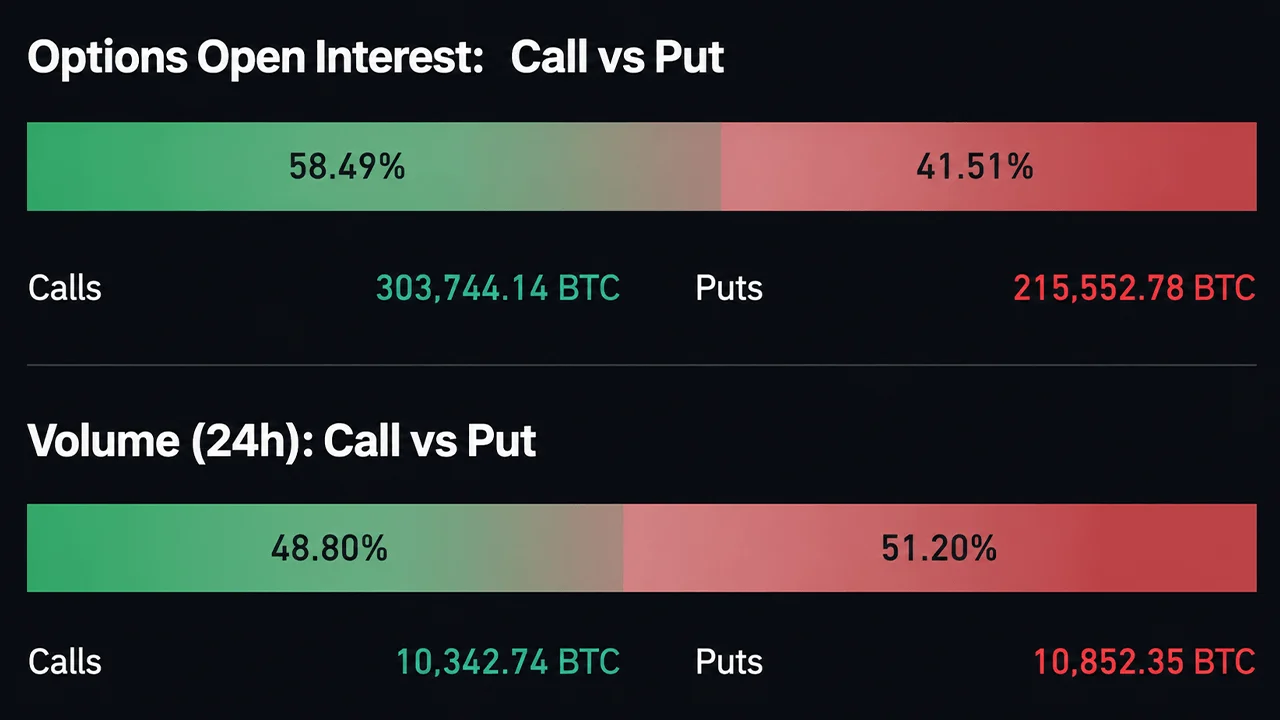

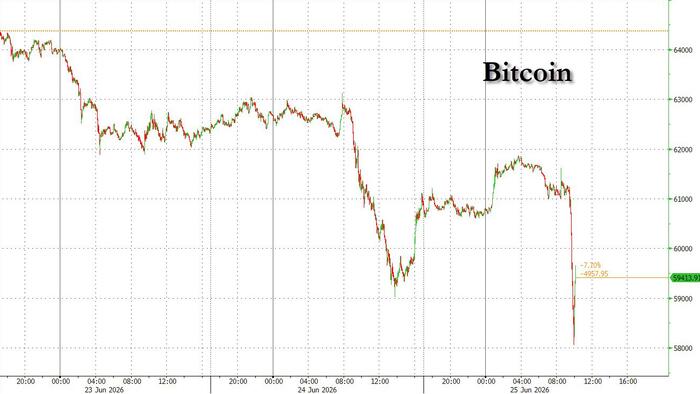

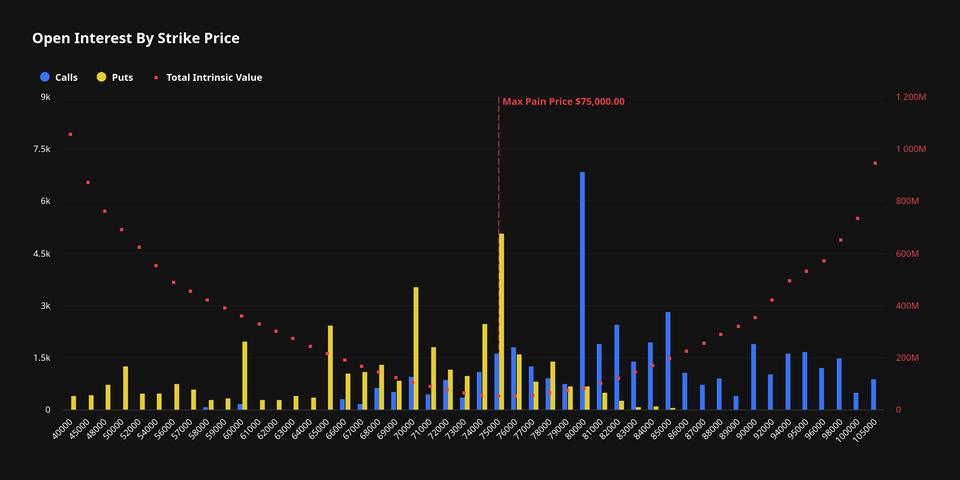

Bitcoin’s options market is staring down one of its largest single-day settlements ever, and the pricing suggests traders aren’t particularly worried about it. Deribit’s DVOL index, the go-to gauge for Bitcoin implied volatility, sits at roughly 42%, a level that seasoned options traders would describe as, well, boring.

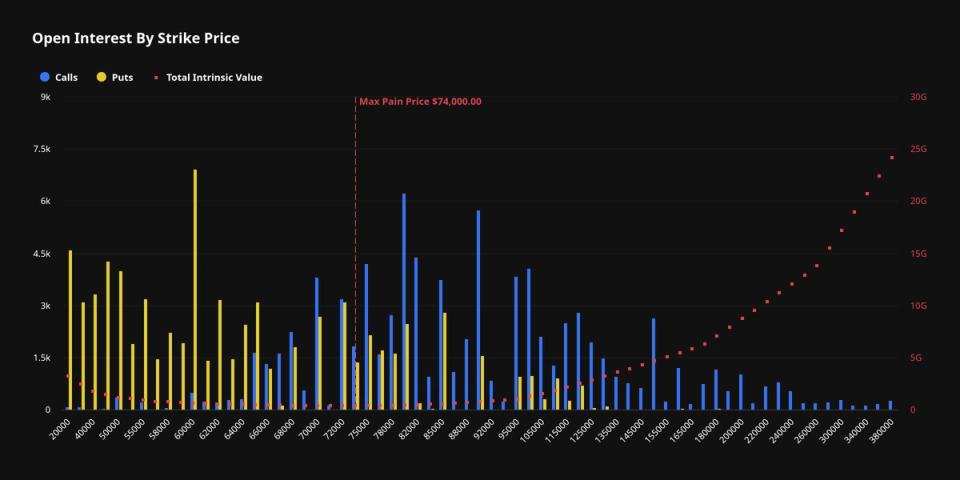

The June 26 monthly options expiry carries a notional open interest of approximately $10.6B. For context, Deribit’s total Bitcoin options open interest across all expiry dates currently hovers around $28B, meaning this single event accounts for a massive concentration of the platform’s outstanding contracts.

Why 42% volatility matters more than it sounds

Think of implied volatility as the market’s best guess at how wild price swings will get. A DVOL reading of 42% means options traders are pricing in moderate, not extreme, movement heading into the expiry.

That number has been trapped in the low-to-mid 40% range recently, which tells us something important. Despite the sheer size of the upcoming settlement, the market isn’t bracing for a shock. At-the-money options, the contracts most sensitive to directional price moves, reflect this same calm pricing.