Memory’s share of hyperscaler capital expenditure is projected to climb from roughly 8% in 2023-2024 to approximately 30% in 2026, according to SemiAnalysis. CLSA takes the projection further, estimating that memory could account for 48% of hyperscaler capex by 2027, up from 35% in 2026.

The numbers behind the shift

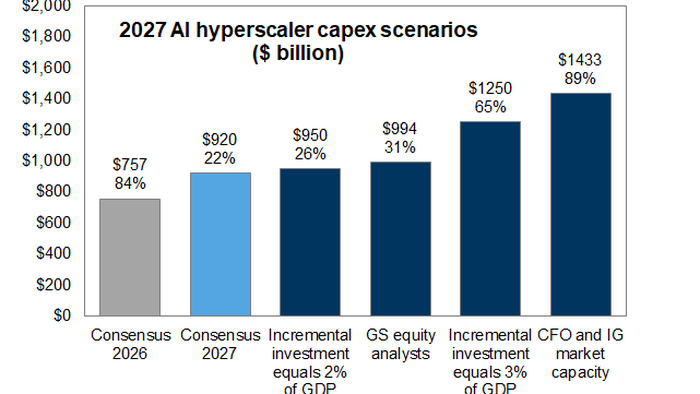

Hyperscaler capex forecasts now exceed $800B for 2026, with consensus estimates approaching or surpassing $1 trillion in 2027. Firms including Goldman Sachs, Morgan Stanley, and Moody’s have all revised their projections upward through mid-2026.

If memory genuinely captures 48% of a trillion-dollar budget, that’s nearly $500B flowing into DRAM, HBM, and related technologies in a single year. For context, the entire global semiconductor industry generated around $527B in revenue in 2023.

LPDDR5 contract prices have increased more than 3x since Q1 2025. DRAM prices more broadly could more than double in 2026, with analysts expecting continued appreciation into 2027. The driver is straightforward: supply cannot keep pace with demand, and the specific type of memory AI workloads require is cannibalizing capacity from everything else.