Japan’s five-year government bond auction landed with a thud on Tuesday, posting a bid-to-cover ratio of 3.11. That’s the weakest showing since February and below the 12-month average, continuing a trend that has bond market watchers increasingly uncomfortable.

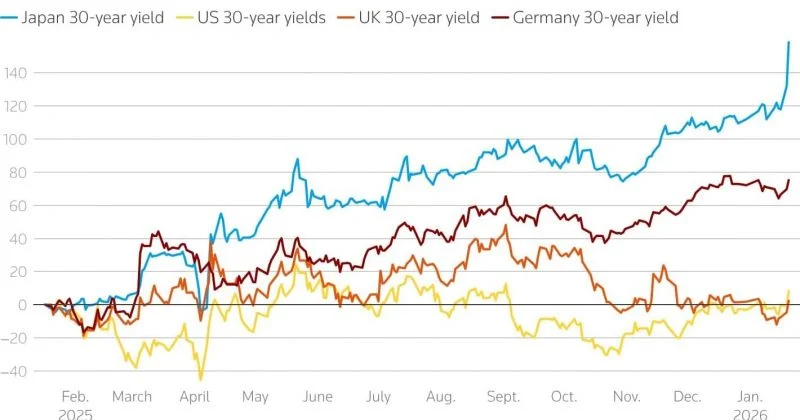

The five-year result follows an equally uninspiring 30-year JGB auction earlier this month, which posted a bid-to-cover ratio of 2.94. For context, the average for 30-year sales sits around 3.4. So demand for Japanese government debt is thinning at both the short and long end of the curve.

The Bank of Japan currently holds its policy rate at 0.75%, a number that would have seemed unthinkable just a couple of years ago when the country was still mired in negative interest rate territory. Markets are pricing in further hikes as the BOJ grapples with persistent inflation, a relatively new phenomenon for an economy that spent decades fighting deflation.

The expectation of additional rate increases is itself part of the problem for bond demand. Why lock in today’s yield on a five-year bond if you believe rates are heading higher? Rational buyers wait, demand weakens, and the cycle reinforces itself.

The yen carry trade connection