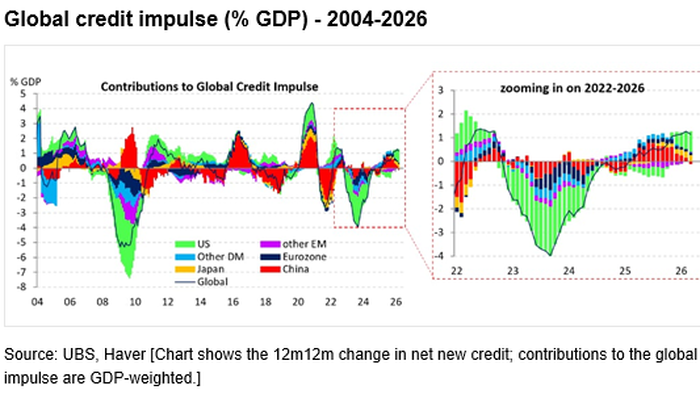

PremiumA little over a week ago we pointed out something remarkable: after China consistently led the growth of the global credit impulse - defined as the 12-month change in net new credit as a share of GDP, and a useful proxy for real domestic demand growth - in recent years there has been a dramatic shift in the balance of credit creation, and according to UBS calculations, the global credit impulse has become overwhelmingly a US story: +2.6% of GDP, or roughly $800bn of additional credit over the past year, much of it the result of funding for various AI projects. Meanwhile, Beijing has taken a secondary role in global credit creation, with the US now accounting for over half of the global credit impulse, largely thanks to the relentless credit expansion fueled by AI capex - recall, as we showed separately, hyperscalers alone will lead to $600 billion in 2026 debt issuance. The obvious implication here is that should the AI-linked credit firehose slam shut, the biggest driver of the global credit impulse will go into reverse, and ostensibly push the world into a recession.

Albert Edwards: Something Big Just Changed In The US Economy

"Both consumption and investment are dependent on the AI ‘bubble’ not bursting." - Albert Edwards

TL;DRAI

US leads global credit impulse at +2.6% GDP (~$800bn), driven by AI capex including $600bn hyperscaler debt expected in 2026. If AI credit tightens, global recession risk rises—forcing tech leaders to recalibrate capex and rethink enterprise AI investment.

186 words~1 min read