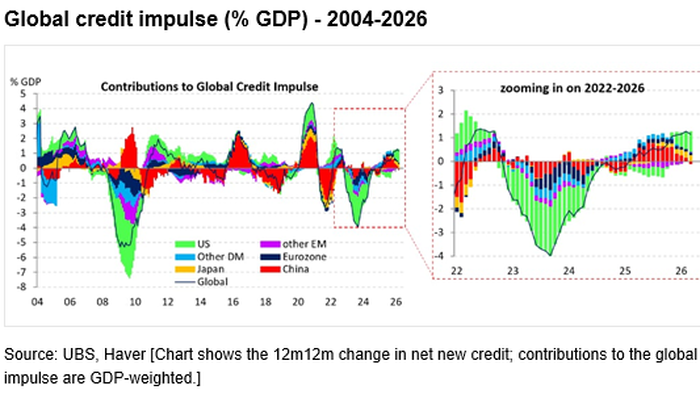

PremiumDuring the global financial crisis and in the aftermath of the European sovereign debt crisis, and again following the global covid crash, China was the global credit dynamo that pushed the world out of a recessionary rut with its massive, seemingly relentless, firehose of debt which lead to three surges in the global credit impulse. Then things changed, and as a result of the giant Chinese housing crash of 2020 which lasts to this day (not to mention China's cumulative 350% debt/GDP), Beijing has taken a secondary role with the US now accounting for over half of the global credit impulse (largely thanks to the relentless credit expansion fueled by AI capex - as explained overight, hyperscalers alone will lead to $600 billion in 2026 debt issuance), but as UBS notes, the strongest acceleration in credit right now is in Japan.

Massive AI Debt Issuance Main Driver Behind Jump In Global Credit Impulse

Step aside China: the global impulse is now overwhelmingly a US story, or rather AI story, accounting for +2.6% of GDP, or roughly $800bn of additional credit over the past year.

TL;DRAI

US hyperscalers' AI capex drove $600B debt in 2026, displacing China as dominant global credit engine. AI infrastructure debt reshapes financing costs; CIOs must reassess capex strategy and debt service impacts as credit conditions tighten.

141 words~1 min read