Aggressive revenue recognition is a common tool of manipulation

| Photo Credit:

bluestocking

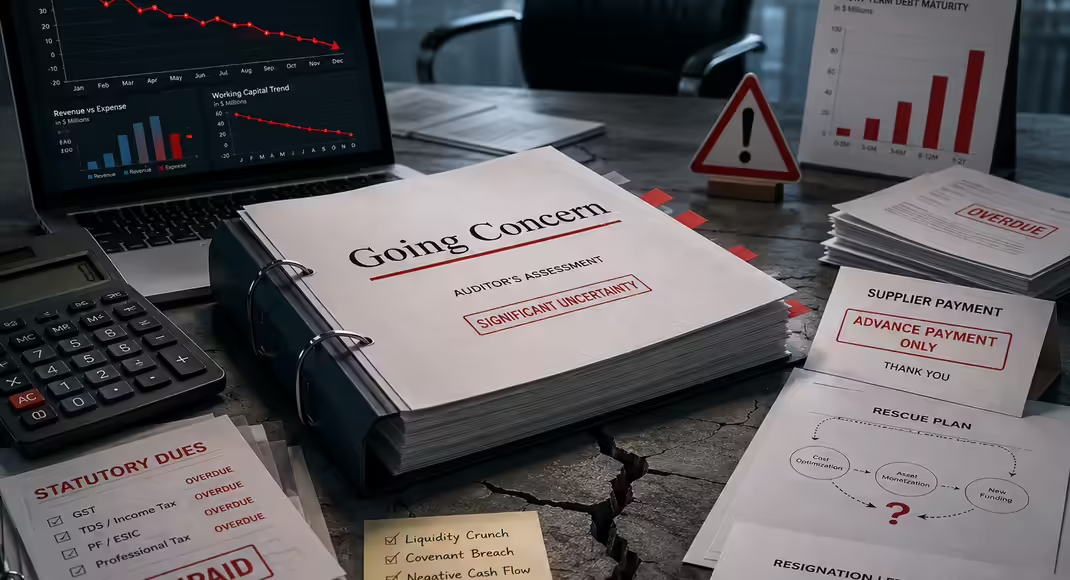

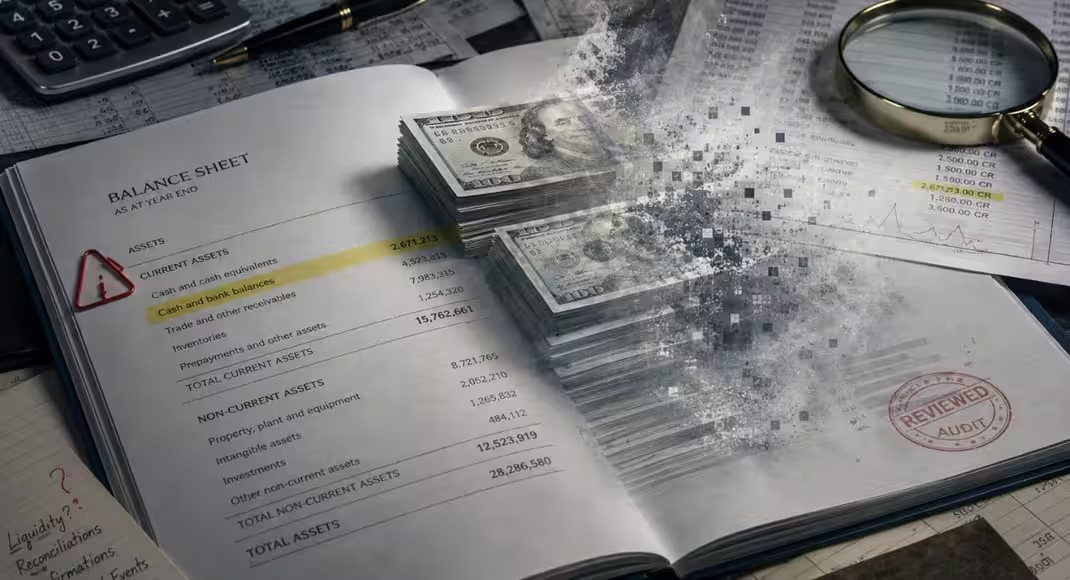

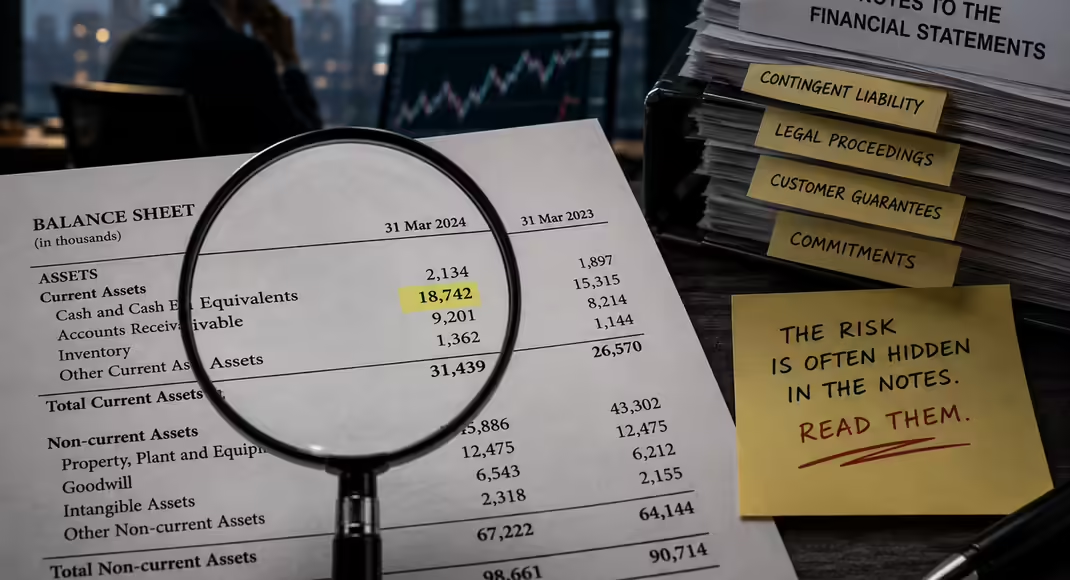

When a listed company releases its annual report, filled with glossy photographs, complex tables and technical disclosures, the average investor can easily feel overwhelmed. Yet beneath the polished surface of financial statements lies a story that may not always be honest. This became evident when the market regulator’s forensic audit of one of India’s largest listed gold companies revealed that up to 99 per cent of its reported consolidated revenues over five years may have been fabricated, amounting to a staggering misrepresentation of over ₹15 lakh crore. A single shareholder complaint, which questioned trade receivables that had remained unpaid for years, was enough to trigger an investigation that exposed what regulators described as “egregious and unheard of” findings.The financial detective at workThis is where forensic accounting becomes vital. It is not merely traditional accounting with more calculations; it is financial detective work. While a regular auditor checks whether the numbers match the records, a forensic accountant examines whether the records themselves are genuine. For investors, especially retail investors, understanding the basics of forensic accounting can act as a shield against corporate deception and wealth destruction. Forensic accounting combines accounting, auditing, legal understanding and investigative skills. If traditional accounting is like a routine medical check-up, forensic accounting is closer to an autopsy that identifies the real cause of financial failure, or a preventive diagnosis that spots danger before collapse. Forensic accountants do not accept numbers at face value. They search for patterns, inconsistencies, unusual transactions and motives behind financial behaviour.The recent case of the Indian jewellery and gold-refining conglomerate offers a powerful lesson. Investigators found that the company allegedly routed a large portion of its revenues through overseas subsidiaries, while withholding key financial statements, customer records, vendor details, and audit working papers from regulators. Such structures make it difficult for ordinary investors to distinguish genuine growth from manufactured revenues. They also show how governance gaps and excessive power concentration in promoter-led companies can endanger public shareholders. One common method used in financial fraud is round-tripping. Here, a company may route funds to a related or shell entity, which then appears to buy goods or services from the same company. On paper, revenues rise sharply. In reality, no genuine economic activity has taken place. Forensic accountants are trained to follow such money trails and identify related-party transactions that lack commercial substance.Red flags for investorsFor retail investors, one of the biggest warning signs is a persistent gap between profits and cash flows. A company may report strong profits year after year, but if cash from operations remains weak or negative, investors must pause. Accounting assumptions can influence profit, but cash is harder to manipulate over long periods. A business that claims to be highly profitable but consistently struggles to collect money from customers deserves closer scrutiny. Another red flag is a sharp rise in trade receivables. When sales grow rapidly, but customers are not paying, the reported revenue may be of poor quality. Receivables that remain unpaid for long periods can indicate aggressive revenue recognition, weak internal controls or even fictitious sales. Investors should ask a simple question: if the company is selling so much, why is the cash not coming in?Aggressive revenue recognition is another common tool of manipulation. Companies under pressure to meet market expectations may record future or doubtful sales as current revenue. Frequent changes in auditors, sudden resignations of key finance personnel, qualified audit opinions, complex subsidiary structures and excessive dealings with unknown entities are also warning signs. Ratio analysis is another useful tool. If a company reports unusually high margins, very low expenses or exceptional growth compared with peers, investors should look for a convincing business explanation. Superior performance is possible, but it must be supported by technology, brand strength, cost advantages or operational efficiency. When extraordinary results come without extraordinary reasons, scepticism is healthy.Exercise due diligenceInstitutional investors often conduct forensic due diligence before committing large sums of money. Retail investors may not have the same resources, but they can still develop basic discipline. Reading cash flow statements, tracking receivables, examining related-party transactions, reviewing auditor remarks, and following credible independent research can significantly reduce risk. Investors need not become forensic experts, but they must learn to ask uncomfortable questions.Ultimately, forensic accounting is about democratizing financial truth. In the past, only large institutions had the resources to look behind the corporate curtain. Today, with greater access to information, digital records and regulatory disclosures, ordinary investors too can become more alert. By looking for cash, questioning related-party deals and being sceptical of “too good to be true” growth, they can avoid major traps. In the stock market, success is not only about finding winners; it is also about avoiding big losers. Corporate fraud can destroy wealth suddenly and brutally. Forensic accounting reminds us that integrity is the most valuable asset a company can possess. The truth is often hidden in the numbers, but investors must know where and how to look.Saravanan is a professor of finance and accounting at IIM Tiruchirappalli, and Williams is the Head of India at Sernova FinancialPublished on June 18, 2026