Story audio is generated using AI

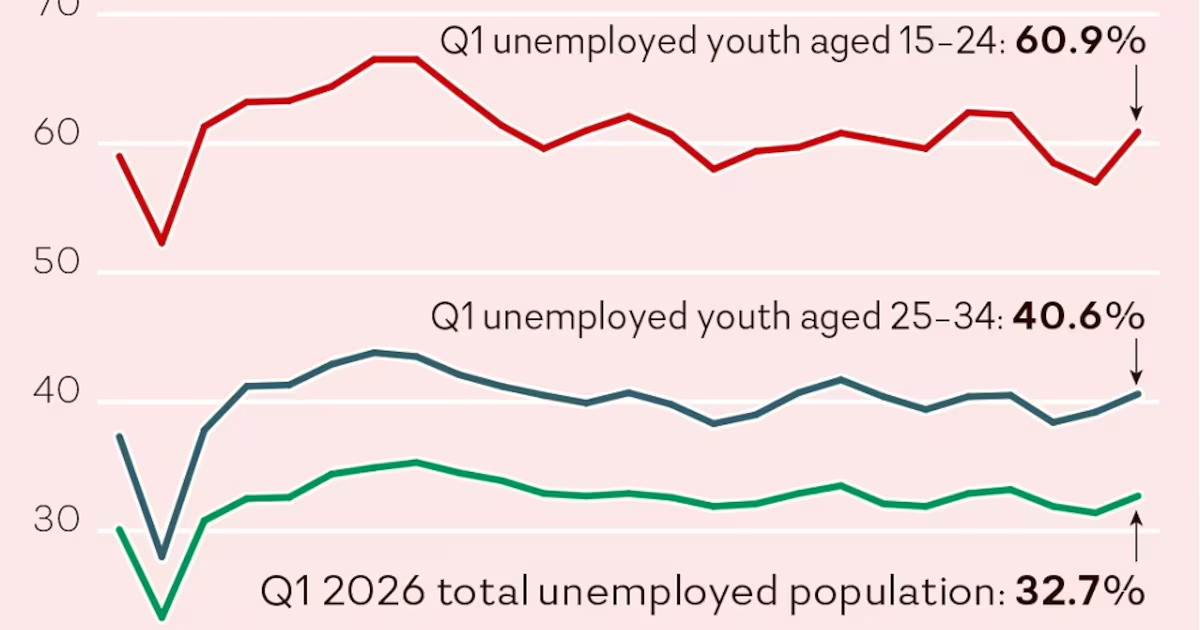

South Africans have become accustomed to a peculiar contradiction. Every year we hear announcements about new investment commitments, expanding factories, modernised production lines and billions flowing into the economy. But every year unemployment remains stubbornly among the world’s highest. The standard response is that South Africa simply needs more investment. More investment will produce more growth. More growth will produce more jobs. More jobs will reduce unemployment. It is a neat theory. The problem is that reality increasingly refuses to co-operate. Recent projections of South Africa’s demographic and labour market future suggest that even under more optimistic growth scenarios unemployment is likely to remain above 30% well into the future. Employment grows, but so does the labour force. More jobs are created, but the number of unemployed people remains extraordinarily high. The implication is difficult to avoid: South Africa’s challenge is not simply a shortage of growth; it is a shortage of labour-absorbing growth. This distinction matters because it forces us to ask whether we have become fixated on the wrong economic indicators. (Karen Moolman) Consider how foreign direct investment is usually discussed. When a multinational company acquires a South African business the transaction is recorded as foreign direct investment. Politicians celebrate it. Analysts welcome the vote of confidence. Newspapers report the value of the deal. The larger the number, the greater the celebration. But from the perspective of unemployment, what exactly has changed? The acquisition of Massmart by Walmart is a useful illustration. The transaction undoubtedly represented a substantial inflow of foreign capital. Yet the deal did not create a new retail industry. It did not suddenly generate tens of thousands of new jobs. What changed was ownership; an existing South African asset acquired a foreign owner. This is not an argument that the transaction was harmful. Nor is it an argument against foreign ownership. It is simply an observation that ownership transfer and job creation are not the same thing. From a national income perspective an awkward question arises. When a profitable South African company is acquired by a foreign owner a larger share of future dividend flows leaves the country. The initial capital inflow may be substantial, but the long-term income stream becomes more internationally distributed. The transaction may make perfect commercial sense, but it does not necessarily solve the country’s unemployment challenge. There is also a balance-of-payments question that South Africa has not sufficiently confronted. When foreign investment builds new productive capacity, expands exports or replaces imports, it can strengthen the country’s external position. But when foreign capital mainly acquires existing assets, the equation is different. The country receives a once-off inflow, while future profits, dividends and other income streams may flow outward year after year. From a national income perspective an awkward question arises. When a profitable South African company is acquired by a foreign owner a larger share of future dividend flows leaves the country.If the investment does not create new jobs, expand domestic value addition or generate additional foreign exchange, South Africa risks exchanging a short-term capital inflow for a long-term external drain. That is not investment-led development. It is a future balance-of-payments trap. The same issue emerges in discussions about industrial investment. When a vehicle manufacturer announces a multibillion-rand investment programme the headline figure dominates public discussion. But much of the investment may be directed towards automation, retooling, equipment replacement, productivity improvements and workforce retraining. Such investments are often essential for competitiveness and may preserve existing jobs. But they seldom create jobs. Again, there is nothing wrong with this. Modern firms must remain competitive. The problem arises when policymakers, commentators and the public treat capital expenditure and employment creation as interchangeable concepts. They are not. None of this suggests productivity is unimportant. On the contrary, productivity growth is essential for competitiveness, profitability, rising incomes and long-term economic sustainability. South Africa does not face a choice between productivity and employment; it requires both. The real question is whether sufficient attention is being given to the type of investment capable of improving productivity while simultaneously expanding employment opportunities. For too long policymakers have assumed investment, productivity and job creation are interchangeable concepts. They are not. An investment may improve productivity without creating new jobs. An acquisition may bring capital into the country without expanding productive capacity. A country confronting unemployment on South Africa’s scale cannot afford to measure success solely by the volume of capital invested or the productivity gains achieved. It must also ask a more fundamental question: how many sustainable employment opportunities are being created? South Africa’s defining economic challenge is not a shortage of capital. It is a shortage of opportunities for work. That reality should influence the way we evaluate investment decisions and economic policy. Instead of asking how much investment has been attracted, perhaps we should spend more time asking what the investment actually does. Does it create new productive capacity? Does it expand supply chains? Does it create downstream industries? Does it increase domestic value addition? Does it create sustainable employment? Or does it simply change ownership, improve productivity or preserve existing operations? These are not the same outcomes, yet they are frequently bundled together under the single heading of “investment”. South Africa does not face a choice between productivity and employment; it requires both. The real question is whether sufficient attention is being given to the type of investment capable of improving productivity while simultaneously expanding employment opportunities. This matters particularly in a country blessed with extraordinary mineral wealth. South Africa possesses resources the world requires for advanced manufacturing, renewable energy technologies and industrial production. But much of this wealth continues to leave the country in raw or semiprocessed form. The familiar pattern persists: export the mineral, import the finished product. The consequence is that we capture only a fraction of the potential employment embedded within the value chain. For years beneficiation has appeared in policy documents and political speeches. Yet progress has often been tentative and uneven. Meanwhile, countries across the developing world are increasingly seeking ways to retain more value from their natural resources through processing, manufacturing and industrial development. The question is not whether South Africa should attract foreign investment. Of course it should. The question is whether South Africa should be more selective about the type of investment it prioritises and celebrates. If unemployment is the country’s foremost economic challenge, investment that creates jobs should carry greater weight than investment that merely changes ownership. Investment that expands domestic value addition should be more highly prized than investment that reinforces dependence on raw commodity exports. Investment that builds labour-intensive industries should arguably receive greater policy attention than investment that simply improves productivity in sectors that already employ relatively few people. None of this requires hostility towards foreign capital. It requires clarity about national priorities. Perhaps the time has come to ask a question South African economic policy has avoided for too long: are we measuring the wrong thing? If unemployment is the country’s greatest challenge, the ultimate test of economic success cannot simply be how much capital enters the country. It must be whether that capital creates opportunities for South Africans to work. • Swanepoel is CEO of the Inclusive Society Institute. This article draws on the institute’s recent research on South Africa’s population dynamics, economic growth and employment prospects.