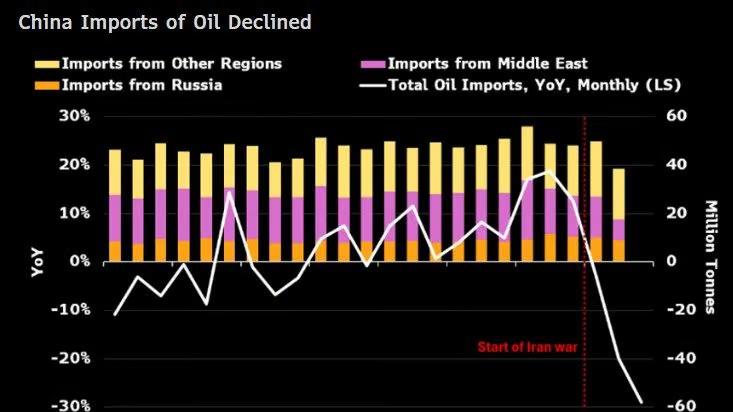

There is an obvious “if” underlying any analysis of the economic impact of the agreement between the US and Iran – everything hangs on whether it will now be signed and can become a longer-term deal. If that happens, then the risk of a further surge in energy prices, a spike in wider inflation and a big hit to growth, will be removed from the economic outlook, which was Longer-term questions about energy flows will, however, remain. The war has shown clearly how quickly supplies can be disrupted.For now, there is relief the progress has been made. The market reaction on Monday was predictable – oil prices fell, Government bond prices went up – due to hopes of lower inflation -and share prices rose. Among the stocks to gain most internationally were the big players reliant on consumer demand, which was exposed to risks of higher inflation and lower growth.Things will not return to the pre-war situation immediately. Global oil flows have been disrupted and even if shipping can now flow freely there will be a considerable period of “catching up”. The extent of damage to the Gulf’s oil infrastructure and what impact this will have on oil and liquefied natural gas (LNG) shipments is also not entirely clear. In turn this will affect wholesale prices and costs to consumers. Encouragingly, energy markets have adapted to the problems in recent months perhaps better than could have been hoped. Still, if the deal holds, then the risk of a further escalation of energy prices and even potential supply shortages in some areas will be taken off the table. In turn this would limit the risks of inflation surging higher. An important context, however, is that we do not know the longer-term implications for energy flows through the Strait of Hormuz, weaponised in the recent conflict. Just how quickly supplies can be disrupted is now all too clear. In the shorter term, there will be arguments about the likely impact on inflation and interest rates – and what central banks now need to do on interest rates. The outlook for borrowers has now clearly improved though central banks will remain vigilant. The impact on inflation will linger as higher energy costs have already fed into the supply chain – for example in areas like fertilisers. We will just have to see how this plays out. For the Irish economy, a permanent agreement and a free flow of energy supplies would obviously be good news. As the Government and interest groups discuss the budget at the National Economic Dialogue on Monday, the prospect of energy costs easing in time would take some pressure off households. That will in turn take pressure of the Government to bring in measures to compensate those hit.Remember, though, that as we saw after the 2022 energy shock, the hedging practices of big energy companies slow the increase in prices when wholesale markets are heading higher, but also delay the decreases feeding through to consumers when wholesale prices come down.The high cost of living and the prospect of a slow normalisation of energy markets mean pressure to “do something” in the budget to help households will remain.For now, the Government is likely to argue that it needs to wait and see now how energy prices pan out. Importantly, however, the prospect of having to deal with some kind of energy emergency in the budget will now recede, if the deal holds. And so will the risk of a global period of high inflation and slow growth – so-called stagflation – which would have had a big impact in Ireland.If – there is that word again – this all holds, a big economic risk has been removed even if the war has introduced a new longer-term uncertainty about the security of energy supplies.

The Iran deal removes a big economic risk for Ireland, if it holds

The deal will ease some pressure on households and the Government but problems will remain

633 words~3 min read