Get the latest news and updates from Dawn

If ever voice mattered, it was now. The budget unveiled today shows the government heard everything that was being said about it and has moved to rectify, albeit the moves are small.

Salaried people have been extended some relief, but mostly for upper slabs. The infamous “deemed income” on capital assets (immoveable property) has been scrapped. The other bug bear of the elites, the so-called “Super Tax” has been abolished for firms with income up to Rs500 million and for those earning above this threshold the rate has been reduced from 10 per cent to 8pc, excluding banks, E&P and fertiliser sector.

Advance taxes on real estate transactions have been reduced from 2.75pc to 1.5pc, supposedly to encourage documentation of these transactions. The Capital Value Tax (CVT) on foreign movable and immovable assets of resident Pakistanis has also been abolished.

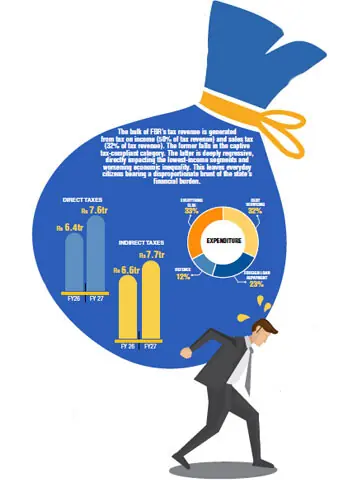

These measures were lightning rods throughout the tenure of this government and the fact that they have moved on them shows they are responsive, even if much ground remains to be covered. What is puzzling though is trying to figure out how they intend to squeeze and additional Rs 2.281 trillion FBR tax revenue for FY27.