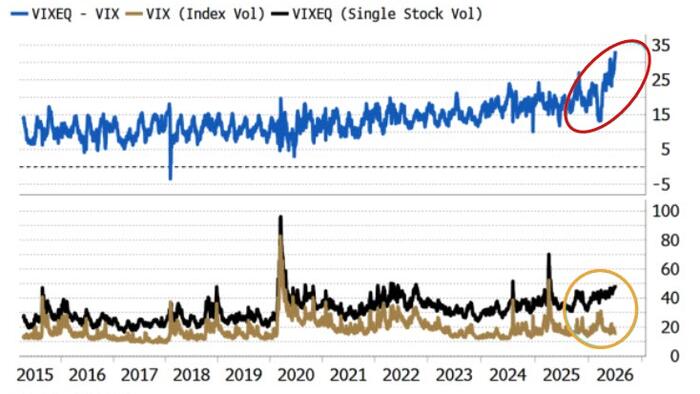

The S&P 500 is doing its best impression of a serene lake. Flat surface, gentle ripples, nothing to worry about. But underneath, individual stocks are thrashing around like they’re being chased by something with teeth.

Average three-month implied volatility for individual S&P 500 stocks has climbed to roughly 40%, the highest reading since the tariff-driven sell-off in March and April 2025. Meanwhile, the VIX, which measures expected volatility for the broader index, is sitting at around 15.8% for the year. That’s a 29-point spread between single-stock volatility and index volatility, a record that was set in early June.

The great divergence

The Cboe single-stock volatility index, known as VIXEQSM, recently surged to nearly 45%. Options markets are pricing in that individual equities could move dramatically over the coming months, even as the overall market appears to be sleepwalking.

The driver behind this isn’t some macro catastrophe or geopolitical shock. It’s idiosyncratic risk, which is a fancy way of saying company-specific stuff. Earnings reports are generating outsized moves. Sector-specific news, particularly in technology and semiconductors, is creating pockets of intense volatility that don’t ripple across the broader index.