Discover high-conviction stock picks and new investing opportunities with the TipRanks Smart Investor Newsletter

In a recent report, DBS analyst Amanda Tan said that the market may be overlooking a key reality of the memory industry. According to Tan, memory capacity cannot be added overnight, meaning supply is likely to remain constrained even as demand from AI data centers continues to grow. She also highlighted Micron’s ongoing manufacturing expansion, including its advanced memory facility in Singapore, as a long-term driver that could help the company meet rising demand through 2027 and 2028.

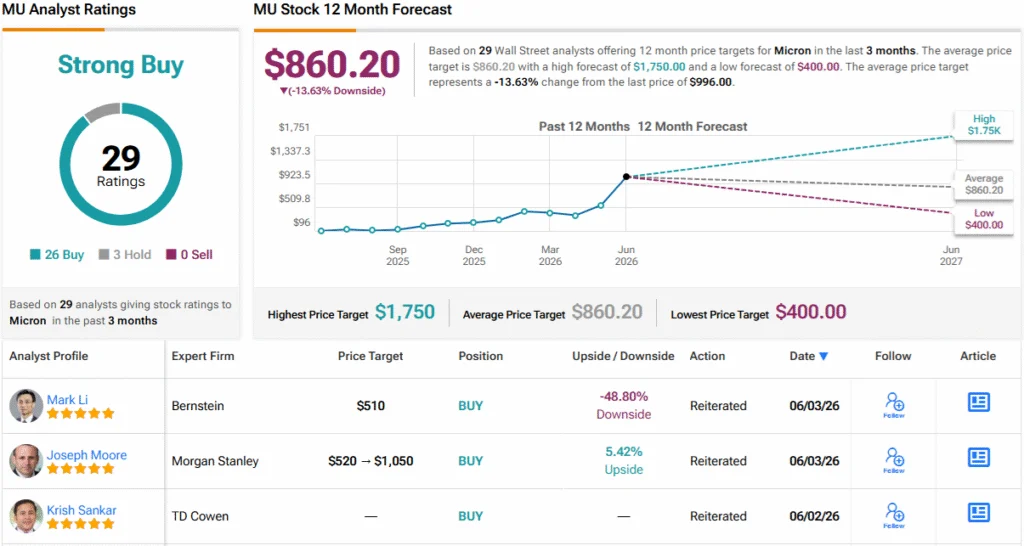

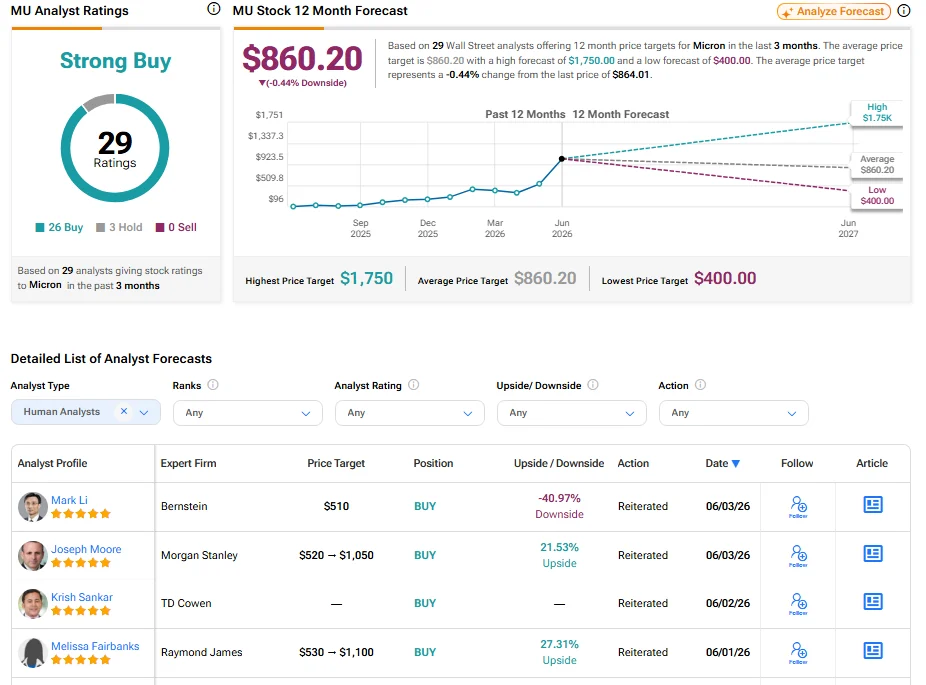

Meanwhile, Bernstein analyst Mark Li maintained his upbeat outlook on Micron. He highlighted a sharp rise in memory prices and said demand for server DRAM and enterprise SSDs continues to exceed supply as companies ramp up AI spending. While he expects price gains to slow later this year, Li believes memory prices should remain strong through 2027 due to tight supply and healthy data center demand.

June 24 Could Settle the Debate

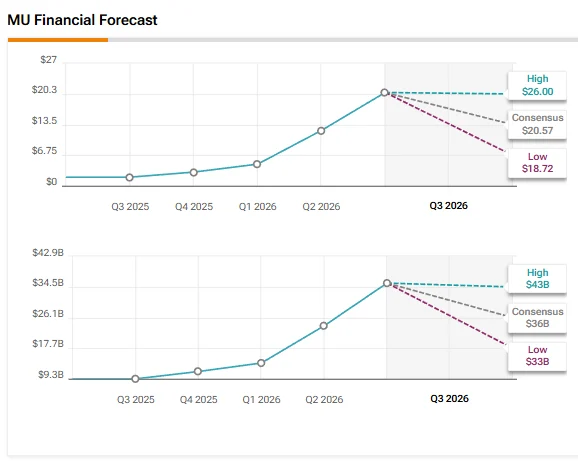

Micron’s upcoming earnings report may determine whether the recent selloff was justified. Wall Street expects fiscal third-quarter earnings of $19.63 per share, up roughly 927% from a year ago, while revenue is projected to rise 268% to $34.27 billion.