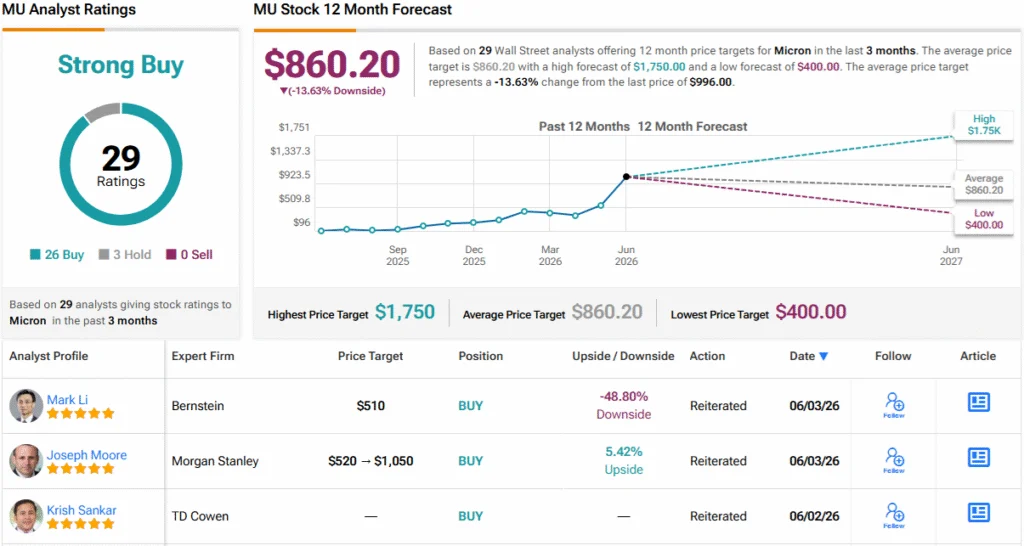

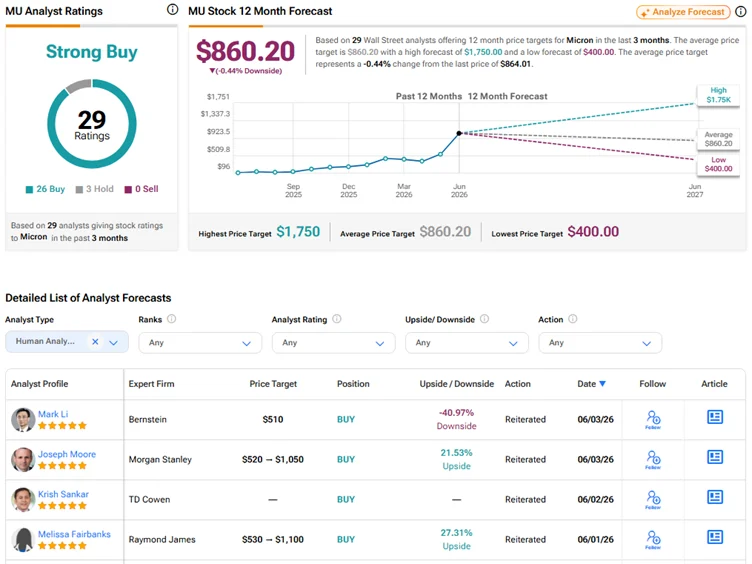

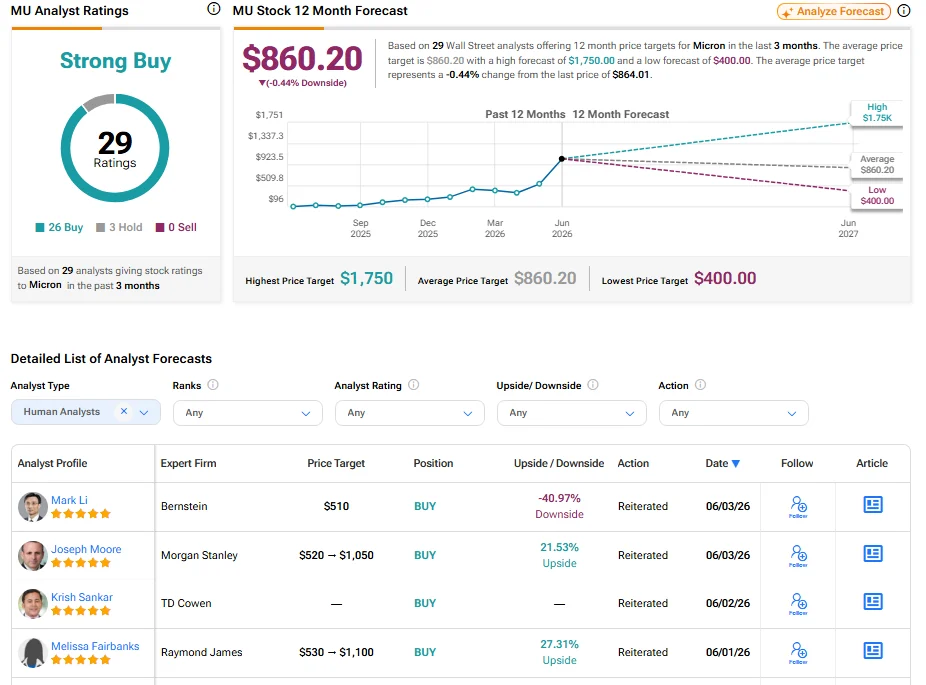

Although Broadcom delivered strong quarterly results, investors were underwhelmed by its AI outlook. The company maintained its long-term forecast for AI semiconductor revenue above $100 billion by fiscal 2027 rather than raising it, and projected fiscal third-quarter AI revenue that largely matched lofty expectations.With valuations across the AI trade reflecting aggressive growth assumptions, the absence of a meaningful guidance increase triggered profit-taking and weighed on semiconductor stocks, including Micron.Earnings And Analyst OutlookMicron’s next major catalyst is its earnings report, scheduled for June 24, 2026.Wall Street expects earnings of $19.29 per share, up from $1.91 per share a year earlier. Revenue is projected to reach $33.88 billion, compared with $9.30 billion in the prior-year period.The stock trades at a price-to-earnings ratio of 50.9, reflecting a premium valuation compared with many semiconductor peers.Analysts maintain a Buy consensus rating on the stock, with an average price forecast of $827.61. Recent analyst actions include:

Morgan Stanley maintained an Overweight rating and raised its price forecast to $1,050 on June 3.

Raymond James maintained an Outperform rating and raised its price forecast to $1,100 on June 1.