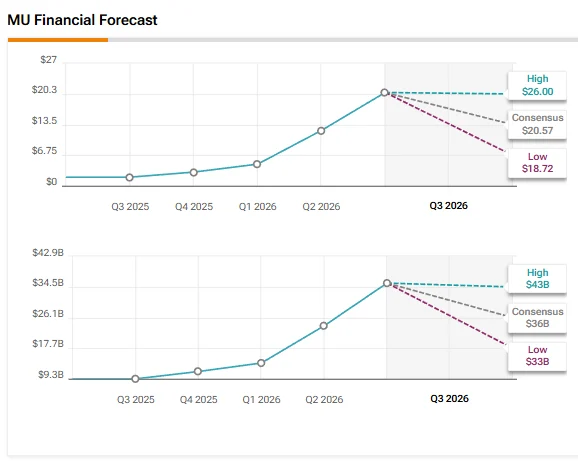

Meanwhile, Wall Street expects Micron to report earnings per share (EPS) of $20.57, implying an impressive surge from $1.91 in the prior-year quarter. Revenue is estimated to rise more than 282% to $35.56 billion, reflecting continued strength in demand for high-bandwidth memory (HBM) and other offerings, as well as elevated pricing amid supply shortage.

Here’s Why Analysts Are Bullish on MU stock Ahead of Q3 Results

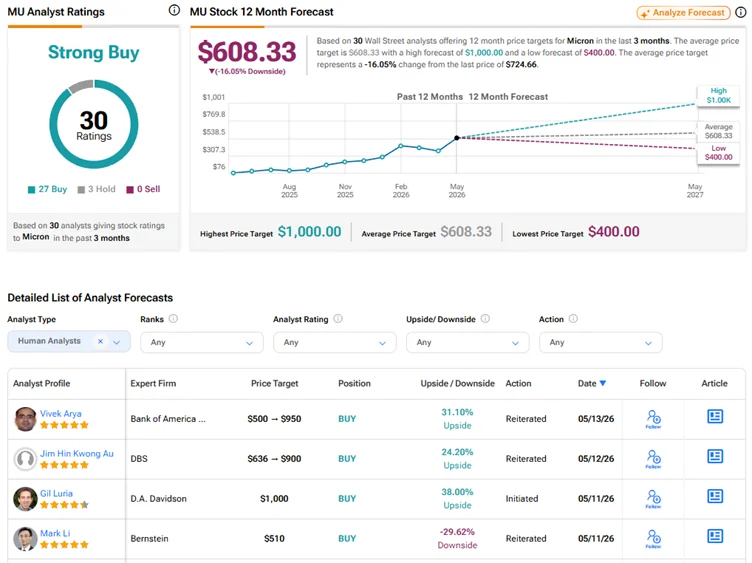

Stifel analyst Brian Chin reiterated a Buy rating on Micron stock and significantly raised his price target to $1,500 from $550. The 5-star analyst boosted his estimates, citing a strong surge in AI-driven memory demand. Chin expects DRAM average selling prices (ASPs) per gigabit (excluding HBM memory) to be about twice as high as Micron’s initial outlook implied for Q3 FY26.

While the increase in conventional DRAM pricing may slow, Chin believes that the main growth driver will be HBM prices. Industry checks indicate that HBM pricing could rise by more than 50% for 2027, with agentic AI-led demand giving suppliers like Micron pricing power.

Likewise, Wedbush analyst Matt Bryson raised his price target to $1,300 from $550 and reaffirmed a Buy rating. The 5-star analyst significantly raised his Q3 FY26 revenue and earnings estimates, as pricing for NAND and DRAM in the second quarter of calendar year 2026 spiked by “high double to even triple digits.”