US bank loan delinquencies ticked upward across multiple categories throughout 2025, according to Federal Reserve data. The total bank loan and lease delinquency rate fluctuated between 1.48% and 1.55% across the quarters of 2025. That’s still below the 10-year average of roughly 1.7%.

The numbers behind the uptick

The New York Fed’s Q4 2025 Household Debt and Credit Report, published in February 2026, put aggregate household debt delinquencies at 4.8% of outstanding balances. That’s a 0.3 percentage point jump from Q3 2025, when the figure sat at 4.5%.

Early delinquencies on mortgages and student loans drove much of the increase. Student loan delinquencies were particularly stark: 9.6% of balances were 90 or more days past due in Q4 2025, a figure that reflects the expiration of pandemic-era forbearance measures that had effectively frozen millions of borrowers’ obligations.

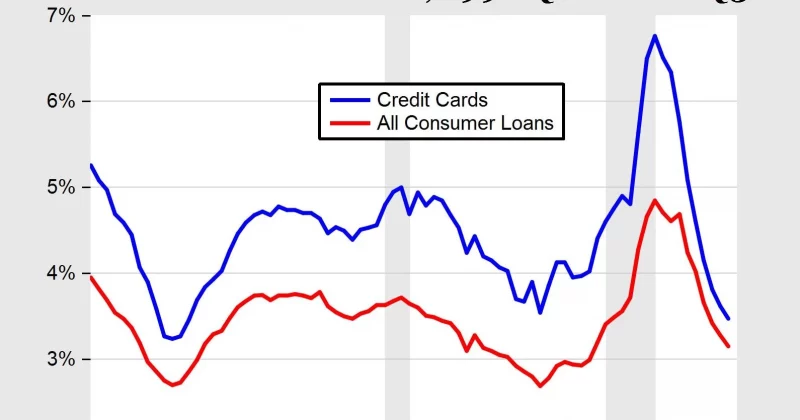

Residential real estate, consumer loans, and credit cards all showed minor quarterly increases throughout the year. Commercial real estate delinquencies actually declined to approximately 1.5% by Q2 2025. During the first half of 2025, total bank loan delinquency rates held near 1.5%, remaining under the 10-year average of approximately 1.7%.