For decades, US Treasuries were the boring, reliable anchor of any sensible portfolio. You held stocks for growth, bonds for safety, and the two were supposed to move in opposite directions when things got rough. That relationship is breaking down.

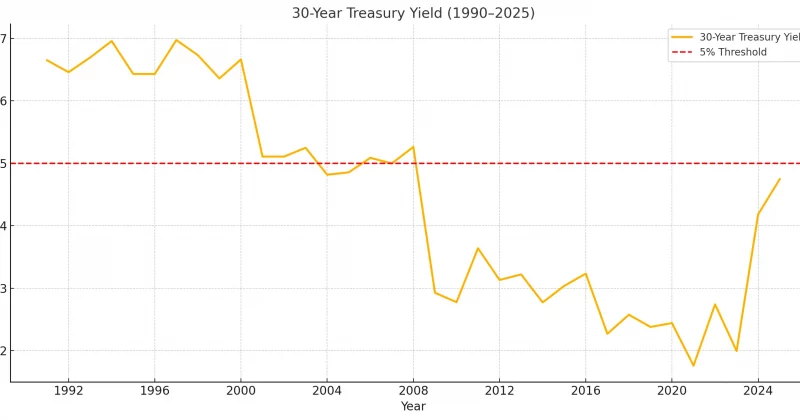

The 10-year Treasury yield climbed to roughly 4.6% in mid-May 2026, its highest level since early 2025. The 30-year yield blew past 5.2%, a mark investors haven’t seen since 2007. These aren’t gentle moves. They represent a fundamental repricing of what “safe” means in fixed income.

The hedge that stopped hedging

In high-inflation environments, that correlation has turned volatile, and at times, outright positive. In plain English: stocks and bonds are falling together, which means your “hedge” is just another source of losses.

The culprits are familiar. Persistent inflation expectations have kept the Federal Reserve locked into a “higher-for-longer” rate stance. Geopolitical friction, including oil market volatility tied to tensions with Iran, has added fuel to the inflationary fire. And mounting fiscal concerns about US government debt levels have made investors demand higher yields just to hold Treasuries at all.