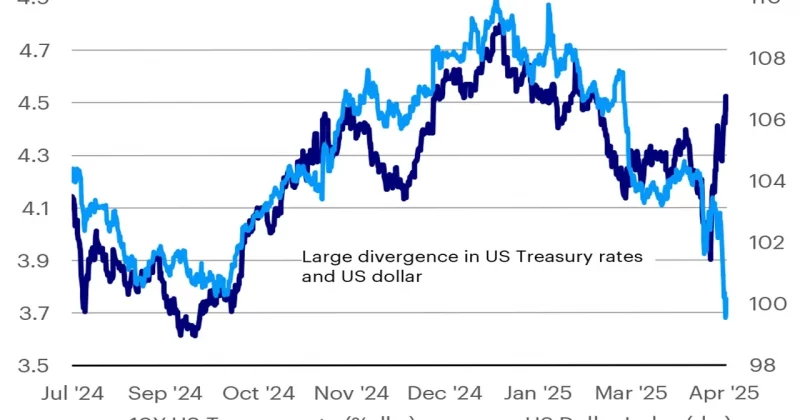

The S&P 500 has stopped playing by the rules. Nelson Armbrust, a Managing Director and lead trader at Goldman Sachs, is flagging something that should make any portfolio manager sit up straighter: the correlation between the S&P 500 and other macroeconomic assets has broken down to levels not seen in a decade.

Armbrust’s observation is that the SPX correlation with rates has dipped to decade lows. This kind of decorrelation tends to show up during periods of concentrated equity performance, where a handful of names or themes drive index-level returns while the broader macro environment sends mixed signals.

The timing matters. In early May 2025, the S&P 500 closed higher for nine consecutive trading days. That’s the first streak of that length since 2004, over two decades ago. Projected daily passive flows during that stretch hit approximately $6.5 billion, driven by aggressive corporate buybacks and systematic trading activity from commodity trading advisors, or CTAs.

What makes Armbrust’s position interesting is that he isn’t bearish. He remains generally optimistic about US equities, pointing to the sheer volume of passive inflows as a supportive force. But Armbrust is recommending that investors consider hedging or de-risking at current levels, given elevated valuations and uncertain macroeconomic indicators. If you’re hedging an equity portfolio using interest rate products or currency positions, and the historical relationship between those assets and the S&P 500 has deteriorated, your hedge might be less effective than your risk models suggest.