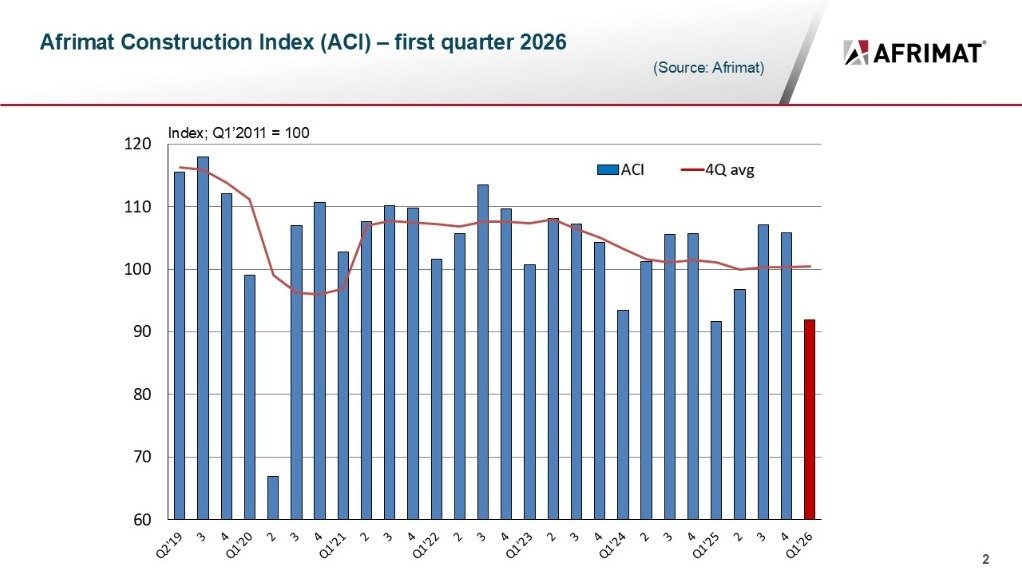

Afrimat’s annual earnings rose by a third as the group focused on costs and as it stemmed losses in its cement business. The multicommodity mid-tier mining company’s group revenue increased 20.3% to R10bn for the year ended February, while operating profit increased 9.6% to R523.7m, it said on Thursday. HEPS were up 32.5% to 95.8c and the group paid a total dividend of 33c per share, up 32% year on year.The group said that during the first half of the year, Afrimat delivered 101.9c per share, which turned to negative 6.1c in the second half. This was caused by the Glencor-Merafe ferrochrome smelter shutdown and lower profitability in the iron ore business, which was both volume- and price-driven.“These results reflect the strength of Afrimat’s strategic positioning and our ability to deliver on our investment commitments. Our renewed focus on aggregate quarrying has proved to be well-timed, and the Lafarge integration is complete and performing exceptionally well, said CEO Andries van Heerden.“The aggregates business has been significantly strengthened, and the numbers demonstrate this clearly.”The cost of sales increased, primarily due to higher-than-normal repairs and maintenance in the cement business to improve the performance of the plant. Cash generated from operations amounted to R831.4m and though this is below its customary levels, Afrimat said the work done during the financial year puts cash generation on a firmer footing for the future. “This, together with cash from the sale of non-core assets and properties, expected in the new financial year, will be used to pay down debt.”Afrimat’s product range is wide and diversified. The construction materials segment’s revenue increased by 20.7% to R5.5bn, with aggregates delivering an increase of 11.2% and cement 54.3%. Improved service levels and product availability at the former Lafarge quarries enabled the business to regain previously lost market share, driving stronger sales performance. The group added that significant progress was made in the aggregates business during the second half of the financial year, with 80% of the projects required to position it as a stronger, more competitive player completed. Year-on-year revenue growth was driven by a wider presence across the country, supported by continued orders from road, construction, rail projects and provincial infrastructure maintenance.Noncore brick and block, ready-mix businesses, as well as noncore properties, were sold, with cash proceeds expected to flow through in the new financial year. The cement business contributed revenue and an operating loss of R1.56bn and R185m, respectively. Cement sales volumes increased, delivering 36.2% sales growth, while resolving inherited operational challenges and improving revenue by 54.3%.“With substantial remedial work and maintenance properly undertaken to repair previous neglect (a total of R271.6m was spent in financial year 2026 on repairs and maintenance), losses in the cement business have been stemmed with strategic alternatives under consideration,” Afrimat said.Bulk commodities revenue increased by 15.7% from the previous year. The first half of the year delivered strong volume performance from local iron ore sales, which was partially offset by a softer trading environment in the second half, it said.International iron ore sales were affected by lower dollar prices, and exports continue to be affected by the challenges on the rail line. “Despite Transnet not being able to provide capacity to fill the group’s rail allocation of 870,000 tons per annum, with export volumes remaining 17% below this allocation, the work being done by the new Transnet management team to fix a broken and ailing iron ore export line is to be commended,” it said.The temporary shutdown of all South African ferrochrome smelters in August 2025 had a significant impact on Nkomati’s revenue, which had no sales for six months, and profitability, and operations were suspended as part of cost-containment measures. This shutdown, together with an impairment of the underground operation amounting to R118.2m, resulted in an operating loss of R160.5m.Afrimat embarked on a strategy to gain exposure to critical minerals by acquiring Glenover a few years ago. This resource contains a unique combination of minerals, including phosphate, iron and a high concentration of valuable rare earth minerals. Comprehensive research and development work has proven that the Glenover material is a unique and highly valuable feedstock for modern batteries as well as a source of rare earth minerals, Afrimat said. “Discussions to find suitable technical partners to advance the project to implementation are progressing well. Afrimat has chosen project strength over speed and has invested the time needed to position a globally competitive project.“As the world prepares for AI and hyperscale data centres, demand for rare earth elements is rising, and Afrimat recognises Glenover’s significance in this scenario. While the group is experienced in mining this type of asset, it has started discussions with reputable international and local players to partner with it on this project, both technically and financially, to develop processing technology for extracting battery minerals and rare earths,” it said.The group said the position of the aggregates and iron ore business is strong, with sufficient capacity to increase production in both should market demand call for greater supplies.It said a reduced electricity tariff for the ferrochrome industry could dramatically improve Nkomati’s prospects. The outcome of the National Energy Regulator of South Africa’s decision on tariffs is expected in June. Afrimat has submitted an application for an increased allocation on the iron ore export line and expects a final decision from Transnet towards the end of 2027.It is also evaluating opportunities in neighbouring countries that align with Afrimat’s mining expertise and will add value to its current diversified portfolio.For the coming year, the focus will be on reducing debt.

Afrimat earnings rise by a third as cement losses ease

The group has capacity to lift production in aggregates and iron ore if demand rises

921 words~4 min read