Nvidia’s stock is sitting flat heading into its next earnings report, but the options market is telling a different story. Implied volatility is pricing in a roughly 5.3% move in either direction once results drop, a number that sounds modest until you remember we’re talking about a company with a market cap measured in the trillions.

A 5.3% swing on a stock this size translates to hundreds of billions of dollars in value creation or destruction, depending on which way the wind blows. For context, that’s roughly the entire market cap of many S&P 500 components, shifting in a single after-hours session.

What the options market is actually saying

Here’s the thing about implied moves: they’re not predictions. They’re the market’s best guess at the size of the price swing, not the direction. Think of it as a weather forecast saying “expect strong winds” without telling you which way they’ll blow.

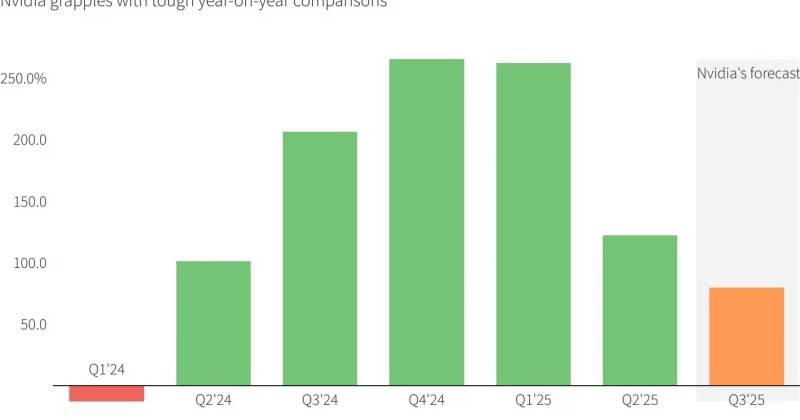

The 5.3% implied move is actually interesting when stacked against Nvidia’s recent track record. Historical realized moves have averaged around 4% to 4.5% over the last eight earnings announcements. That means options are pricing in a slightly larger swing than what has actually materialized recently.